Major averages rose yesterday on lower volume. The averages gapped up about half a percent at the open, then crawled higher for the remainder of the trading day. The NASDAQ Composite is at multi-year highs and S&P 500 is now above its 50dma.

Since late 2008 when QE began, fund managers would have loved to have held a core position in a stock ETF or a volatility ETF such as XIV or SVXY as they would have met their bogeys each year, matching the performance of the indices, or outperforming had they gone on margin or bought a leveraged ETF. Instead, the reality is that equity fund managers of all stripes, including the trend following wizards, have well underperformed the major averages since 2009. But of course, hindsight is 20/20.

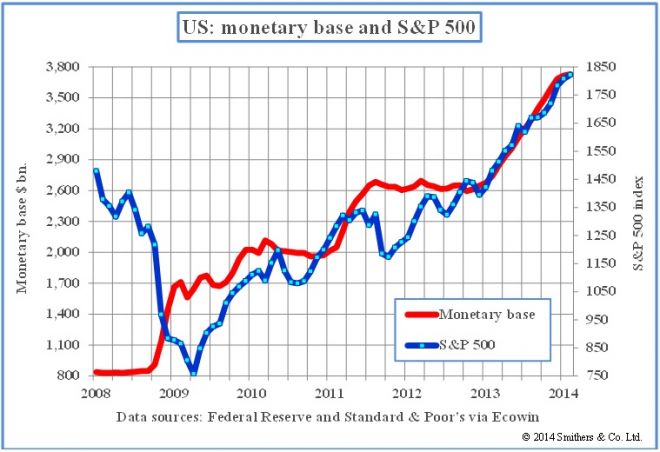

This chart shows the correlation between QE and the stock market since late 2008 when QE began:

So despite the lack of any real economic recovery in the US, the UK, and in Europe, the QE printing press rolls on, defying weak price/volume action in the major indices, continuing to push them higher.

The burning question on everyone's mind due to a number of factors which show a myriad of weak market internals, divergences, and sour global economic health is when will we get an appreciable correction? This nervousness underscores the saying that the market takes the escalator up and the elevator down, though the saying since January 2013 should be adjusted to say that the market takes the stairs up and the trapdoor down. Indeed, whenever the market drops just a few percent, investors run for cover, pushing leading stocks down far greater than the small fall in the averages.

So the MDM will continue to incorporate "selling insurance" by moving to cash (or sell) as the market can fall quickly at times, then also be quick to jump back on board the QE-train uptrend. Keep in mind that there are other ways to skin a cat. PPR and BGU reports continue to work well even in this environment as well as short selling strategies which we discuss at length in our webinars.