That said, MDM always has a point at which it will switch out of its signal to mitigate risk. QE is a formidable force so despite bearish conditions, the market can baby step higher as it has been known to do. We discuss various aspects of the model here: https://www.

In terms of market headwinds, the trade issues between the US and China remain. Trump has been known to change on a dime. This morning, the major averages gapped lower on news the Trump Administration will impose $200 in additional trade tariffs against China.

In addition to the trade issues, the interest rate environment remains tenuous with the Federal Reserve attempting to hike a few more times. As we have discussed in prior pieces, the global economic environment remains stuck in a quagmire, thus global QE remains near all-time highs. The Fed will therefore be unable to hike as aggressively as it wishes. QE explains much of the current weak-volume bounce.

So despite the bearish technicals, QE can still keep the bull alive. Volumes remain bearish for the major indices as bounces come on lower or below average volume while down days come on increasing volume. The cluster of distribution days has been pronounced.

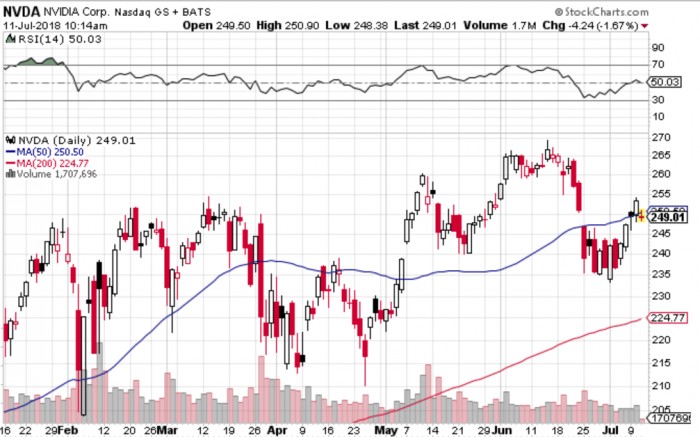

Meanwhile, names that used to lead such as NVDA struggle to find direction. NVDA's recent bounce has also been on lower volume.

The handful of stocks that have bucked the current correction are trading around their 10- or 20-day moving averages or near their old highs, but those are few and far between. That said, NFLX, AMZN, and FB are showing strength as QE tends to find its way into the tallest standing midgets. These stocks need to be owned by the institutions to keep pace with their benchmarks.

Chinese names remain damaged with many trading around their 50 such as MOMO and BZUN, or 200 day lines such as BABA, then continuing to struggle for even a meager bounce as the trade situation worsens. Others have been pummelled well below their 200-day lines such as VIPS, WB, and WUBA.

The market this year is in stark contrast to the trending environment that began mid-2016.

Asset allocation is key when it comes to investing. The tug-o-war between QE and higher interest rates accounts for the choppy first half of the year. This tug-o-war remains. Now add in the trade issues. Both are attempting to counter the bullish effects of the near-record levels of global QE.

The market may therefore remain choppy and trendless. Such an environment is difficult for any trend following model. One may wish to apply profit taking rules in such an environment instead of following the model blindly. Alternatively, one may wish to allocate a smaller percentage of their portfolio to the model. The risk of course is that the market finds an uptrend which can be difficult to join late.

Michael Covel's book Trend Following is an excellent work that shows the challenges even the top trend followers face. In choppy, sideways environments, they know they will lose. But they also know that in trending markets, they will more than make back the losses. Tom Basso is one of the top trend followers that have managed to make money overall despite many others getting thrown in this QE-manipulated environment. Indeed, the MDM managed to do well during the prior trending environment that began in mid-2016. But 2018 has been more or less trendless with volume clues that would normally dictate lower markets ahead, but instead, QE manages to create floors then pushes the market higher on a string. The current environment will continue to pose a challenge should it remain choppy and sideways. MDM will move to cash or buy as conditions dictate.