Another reminder that sell stops of 6% on NASDAQ Composite and 18% on TECL have been suggested starting in the year 2010. Members often set stops based on their risk tolerance levels and position size accordingly whether it is a stock or an ETF. In this Era of QE, since 2009 when QE was launched, the steeper the drop, the greater the upside since tech-driven major averages such as TECL always hit new highs often within a few months of the typical 'V' bottom. As some have been doing with success over the last decade, one buys more the further major indices fall then starts to slowly take profits as they make new highs.

As some have been doing with success over the last decade, one starts buying the further major indices fall then as they make new highs, one starts to slowly take profits. It's an entirely different dynamic but suits some investors' risk tolerance preferences. There's many ways to skin a cat. Some use the Market Direction Model in this manner so if its losses exceed a certain amount during a buy signal, they first sell their position then start to slowly buy if the market continues to fall even if the model goes to a cash signal. Likewise, they start to take partial profits as the market continues to make new highs on a buy signal. Since markets inevitably bounce or top, this is a way to increase profits on selloffs since during macro-favorable times, the model is far more likely to go from buy to cash back to buy as it did through most of 2020 and 2021.

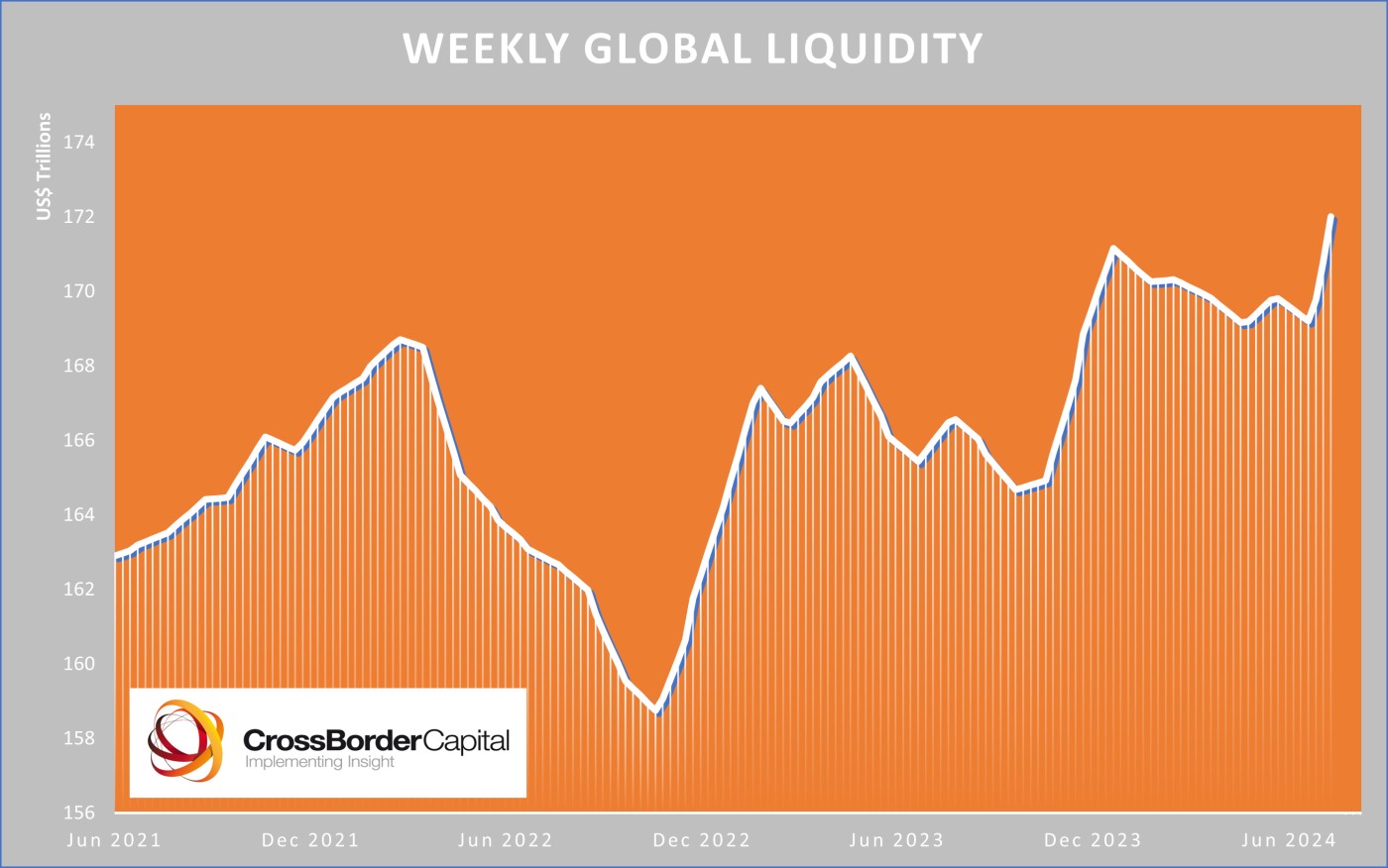

The recent plunge in markets will go down in history. While Japan's stock market posted its biggest 2-day drop in its history, South Korea halted all sell orders on their stock market. Triggering the collapse of world markets and spurring the recent sharp rise in global liquidity (QE/GMI) is the yen carry trade which is in the many trillions wherein an investor borrows in a currency with low interest rates, such as the yen, and reinvests the proceeds in a currency with a higher rate of return. Since Jul 11 when the selloff began, there has been a strong correlation between major stock markets and the USD/JPY chart.

The Japanese government had been telling Japanese banks who hold US Treasuries to sell them to buy Japanese bonds to keep interest rates at bay or the interest on their massive levels of debt will jump. At the same time, the US needs to prevent their interest rates from rising, so using the FIMA repo facility which was created by the Fed, Japanese banks were given cash via stealth QE courtesy of the US Fed without having to sell their US Treasuries. That's a lot of QE. But in the meantime, USD/JPY may unwind further dragging down markets with it. With a stronger yen, borrowers have a higher loan outstanding and their interest rate is higher. The result caused some traders to sell their assets and repurchase yen in order to pay back their loans. But that buy pressure against the yen sends it up further which forces more buying--resulting in a liquidation cascade.

Keep in mind that in this Era of QE, the steeper the drop in an ETF, the greater the upside. ETFs that reflect tech-centric major averages always hit new highs since technology stocks lead bull markets. 'V' bottoms are often formed then new highs are eventually achieved, often within a few months, especially since QE was launched in late 2008.

Observations:

1) Note how a reduction in QE led to the first Christmas crash on record on Dec 24, 2018 but fresh QE days later pushed TECL straight back to new highs within a few months.

2) Note how COVID in Mar-2020 led to massive QE where markets hit new highs within a few months.

3) Even after the first prolonged bear market in 2022, the first since 2008, TECL shot straight back up.

Markets are now pricing in a 60% chance of an emergency Fed rate cut before their meeting in September and two 50 bps rate cuts at their next two meetings. It would not be surprising to see a big wave of emergency QE from major central banks in the coming days.

Even before the crash, renewed global liquidity was already on a sharp rise especially when accounting for private sector liquidity which includes all flows of cash and credit as well as major central banks.

Liquidity (QE, GMI) guides markets. The NASDAQ-100 pulled back in 2022 and from July to October 2023 when global liquidity fell.

But until we get a green light from the Fed on an emergency rate cut, markets will be highly volatile with the likelihood of a possible retest of recent lows given how it may take some time to completely unwind the yen carry trade. Further, if the Fed lowers rates, this will weaken the dollar thus strengthen the yen which will further exacerbate the yen carry trade.

List of Potential ETFs for investors:

1-times inverse

PSQ - NASDAQ 100 1x bear.

2-times inverse

QID - NASDAQ 100 2x bear.

3-times inverse

SQQQ - NASDAQ 100 3x bear.

NOTE: This is a suggested list. Investors may wish to become acquainted with the full range of available ETFs, and should make an effort to understand how these ETFs are created and what their components are, as well as being aware of the downside risks involved, especially with leveraged ETFs. Certain ETFs may be more appropriate depending on one's risk tolerance levels. Typing in keyword 'ETF' into the FAQ keyword search bar or going here https://www.virtueofselfishinvesting.com/faqs/search?p=1&q=etf and visiting this site https://etfdb.com/ can be instructive.