Market Lab Report

by Dr. Chris Kacher

NVDA earningsNVIDIA's latest earnings for Q4 FY2026 landed solid, with revenue hitting $68.1 billion, up 73% year-over-year and beating estimates. Data Center revenue exploded to $62.3 billion, driven by relentless demand for Blackwell GPUs and AI accelerators. Guidance for the next quarter points to $76-80 billion, well above what the Street expected. Adjusted EPS came in at $1.62, topping consensus. Jensen Huang highlighted skyrocketing adoption of AI agents, with commitments soaring to $95.2 billion. This is no flash in the pan; it's sustained momentum.

The stock popped modestly in after-hours trading, a relief rally after some recent chop. NVDA has been holding up better than many in a jittery market, but the real takeaway is validation: AI infrastructure demand isn't slowing. Hyperscalers and enterprises are still pouring money into compute power, and NVIDIA owns the lion's share of that market.

For AI stocks overall, this report acts as a stabilizer. The sector has been under pressure from fears of overbuilding and diminishing returns on massive capex. NVDA's beat and strong forward look ease those worries short-term. Semis peers, cloud giants, and AI enablers should catch a bid as sentiment improves. We could see a rebound in names that got oversold on bubble talk.

But here's the counterbalance: OpenAI just slashed its long-term capex target dramatically, from $1.4 trillion to $600 billion by 2030. That's a 57% cut from earlier projections. The company is now tying spends more tightly to actual revenue growth, which hit $13.1 billion in 2025 but still burned heavy cash. This isn't panic; it's realism. It signals the AI arms race is maturing: less infinite spending, more disciplined scaling.

That shift could cool the wildest enthusiasm. If more players follow suit and prioritize ROI over endless buildouts, capex forecasts across the board might moderate. For NVIDIA, it's mixed: near-term demand stays robust, but a slower ramp in total infrastructure dollars could cap upside later. The focus moves from sheer scale to profitable, efficient AI deployment.

Bottom line: NVDA's results prove the core AI engine is firing on all cylinders. The sector gets breathing room to climb. Yet OpenAI's capex reset reminds us reality is setting in; fortune favors those who align with real momentum, not hype. In markets, as in life, coherence with what's actually unfolding beats forcing outcomes. Stay sharp, stack the odds, and let the right side of the trend do the heavy lifting.

Stagflation risk?

US Q4 2025 GDP grew 1.4% annualized, missing 3.0% forecast, but 1% of the miss was due to shutdown drag, bringing it to 2.4% annualized. Meanwhile core PCE hit 3.0% YoY above 2.9% estimate. This is classic stagflation signals of weak growth + hot inflation though analysts say this is temporary.

AI is boosting productivity (0.1-0.6% annual labor gains), potentially lifting GDP while compressing costs/labor share, creating disinflation (0.5-0.7% CPI drag). This could offset stagflation long-term via supply surge, but short-term labor displacement may weaken demand.

The AI Revolution: Supply-Side Abundance vs. Demand-Side Danger

Elon Musk predicts AI and robotics will drive massive productivity in tradeable goods, creating **supply-side deflation** where output surges faster than money supply, prices plummet, living standards rise, and massive debt becomes easier to service. He calls it “good deflation” and sees it as the path to abundance within a few years.

But there is a critical distinction: **demand-side deflation**—prices falling because people stop spending due to job losses, wage stagnation, or contraction—is far more dangerous. Consumers delay purchases expecting lower prices, businesses cut jobs and output, debt burdens grow in real terms, and central banks lose tools to stimulate. The Great Depression and Japan’s lost decades show how vicious this cycle can become.

AI’s white-collar impact (potentially 50%+ of routine knowledge jobs in 3–5 years) could trigger this sooner than later. Early signs are already here: AI-linked layoffs, hiring freezes, and softening consumer spending in exposed sectors. Robotics in factories, warehouses, and retail will follow, with a longer but similar timeline.

Markets are pricing the **supply-side boom**—productivity miracles, earnings growth, higher multiples—but have not fully factored in the **demand-side risks**. Tech stocks remain euphoric, while consumer and defensive sectors lag. Volatility could spike when mass layoffs hit or consumer data weakens.

In a 70% consumption-driven economy, widespread job destruction risks a deflationary trap unless offset by policy: UBI, wealth redistribution, or new income mechanisms tied to AI gains. Without adaptation, the transition could be painful—recessions, social strain—before abundance arrives.

Musk’s long-term vision of near-zero prices and optional work is plausible, but the path forward hinges on navigating the demand shock. The next 3–10 years will decide whether AI delivers prosperity or a destructive deflationary spiral. Markets are still betting heavily on the upside. History suggests caution until the job reality unfolds.

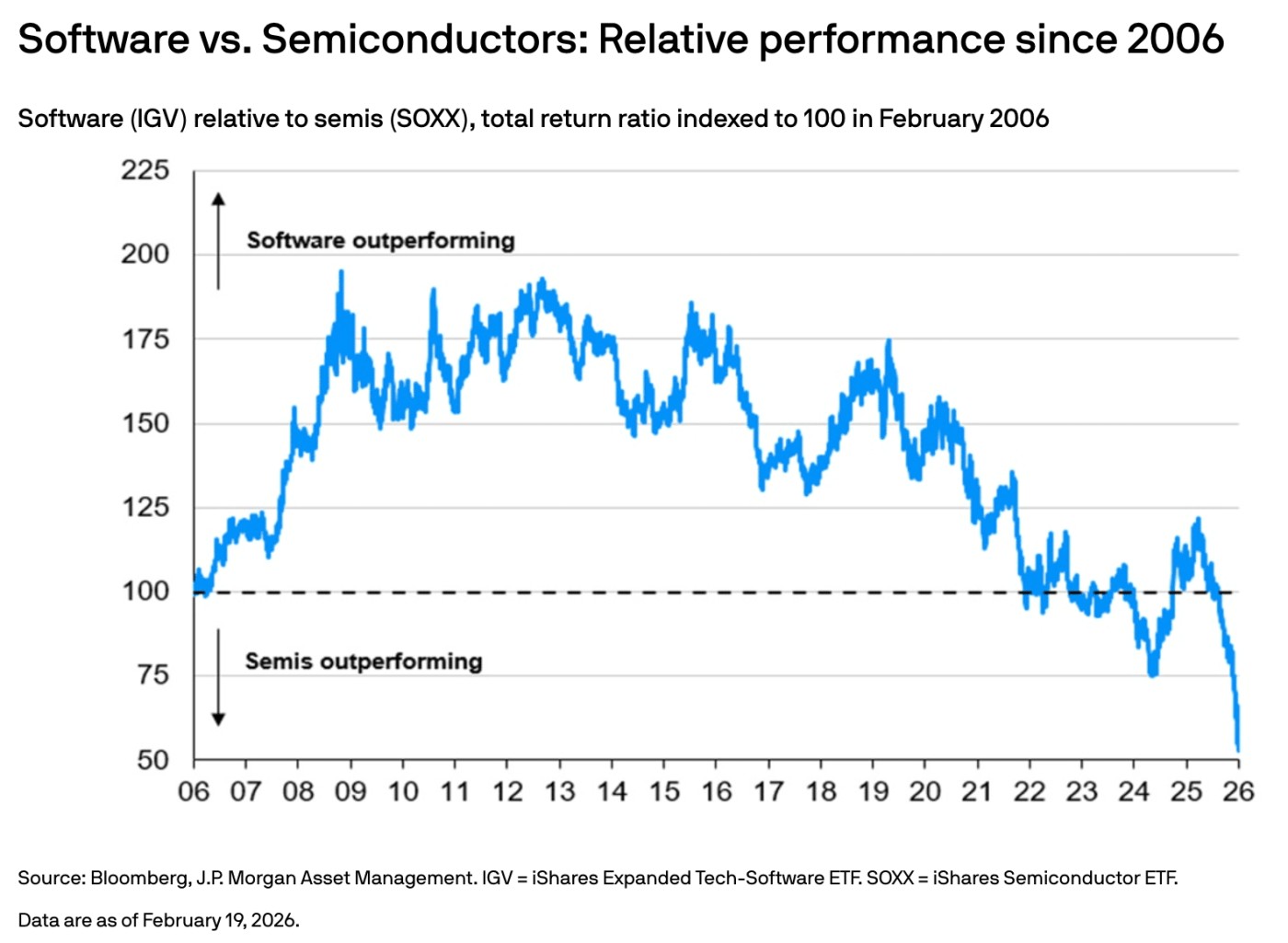

The Great Flip: From Software to Silicon

Underscoring the breakneck speed of change, since 2006, software stocks have crushed chipmakers. Investors rode asset-light, high-margin SaaS models to massive gains—scalable code, recurring revenue, minimal capital.

That era just ended.

The relative price performance of software versus semiconductors has plunged to multi-decade lows. The AI trade is pivoting hard—from code to hardware.

Why? AI agents.

These autonomous systems are no longer assistants; they are executors. They reason, plan, act—handling complex workflows without human teams. If agents can replace entire departments, why pay for dozens of per-seat SaaS licenses? The subscription model that fueled Salesforce, ServiceNow, Adobe, and others is now under existential pressure.

Wall Street sees it. Software valuations are losing their premium. Meanwhile, the real money is flowing to the AI supply chain: energy (power), materials (chips, rare earths), industrials (cooling, racks, data centers). Hardware is the bottleneck; code is becoming commoditized.

This is not the end of software—it is the beginning of its deflationary chapter. Agents collapse complexity into efficiency. The same force driving supply-side deflation in goods will hit SaaS margins.

The market’s intention is clear—hardware wins the next leg. Software survives, but the easy money in that space is over.

FAQ

Q: How do you see the impact from AI sooner than later replacing up to -or maybe more- than 50% of white collar jobs, on the economy and even more so on stock market. Is this already factored in price action? Same question with longer timeline from robots in factories, distribution centers, and retail space. In our consumption driven economy who/how will buy stuff when they no longer have jobs.

A: AI's short-term effect on white-collar jobs could be a "tsunami," with mass displacement leading to structural unemployment, reduced consumer spending, and potential recessionary pressures as high-earning workers (40-60% of the workforce) lose income. For robots in blue-collar work, the economy faces similar but delayed shocks: IMF projects 40% global job exposure, with manufacturing/logistics hit hardest (50%+ vulnerable), potentially spiking unemployment in industrial regions without reskilling.

Longer-term, AI and robotics are expected to create net job gains through productivity booms (e.g., WEF: 170M new jobs by 2030 vs. 92M displaced; Goldman Sachs: 6-7% U.S. workforce shift but offsets via new roles).

Emerging jobs in AI oversight, ethics, data curation, and human-AI integration could outpace losses, with AI-exposed sectors growing wages 2x faster and revenue/employee 3x quicker.

For robots, net +2M U.S. manufacturing jobs by 2030 despite 9M displaced, as repatriation and efficiency create demand in adjacent fields.

As for the stock market, this isn't fully factored into current price action. Markets are optimistic about AI productivity, but broader displacement risks are underpriced. Short-term volatility could rise if layoffs accelerate (e.g., SaaS stocks already falling as AI reduces seats/licenses), leading to consumer spending drops and earnings misses. Longer-term, markets could boom from productivity (e.g., $13T global GDP boost by 2030), but the initial "tsunami" could trigger recessions or selloffs before QE/liquidity rallies assets.