by Dr. Chris Kacher

AI utility exponential

Since the introduction of OpenAI's generative AI ChatGPT in late 2022, the practical applications of AI in the real world have begun to expand rapidly. Take Klarna as an example: the company has revolutionized online shopping by integrating OpenAI's technology into its customer support operations. By replacing human agents with AI, Klarna has slashed the average time it takes to resolve customer issues from 11 minutes to just 2 minutes. Not only has this led to increased customer satisfaction—with AI proving more efficient than human staffers—it has also significantly boosted the company's profitability.

The emergence of generative AI is creating a profound impact across industries, delivering substantial economic benefits and reshaping the business landscape. Although there are concerns about job displacement in customer support roles as more companies adopt similar AI solutions, the flip side is that the extra profits generated could be reinvested into creating more advanced, higher-level jobs, propelling the workforce toward more sophisticated tasks.

Historically, technological advancements have consistently transformed the nature of work. From the advent of the plow to the rise of the automobile, humans have transitioned from manual labor to knowledge-based roles, and now to creative and innovative work, spawning new job categories. With generative AI, a small startup can outmaneuver larger, established companies, achieving revenues of $100 million with just a handful of employees. Operating costs for technology companies are poised to halve as generative AI takes over coding and other functions. We're looking at a future where companies are streamlined, with a single leader orchestrating a suite of software and AI tools.

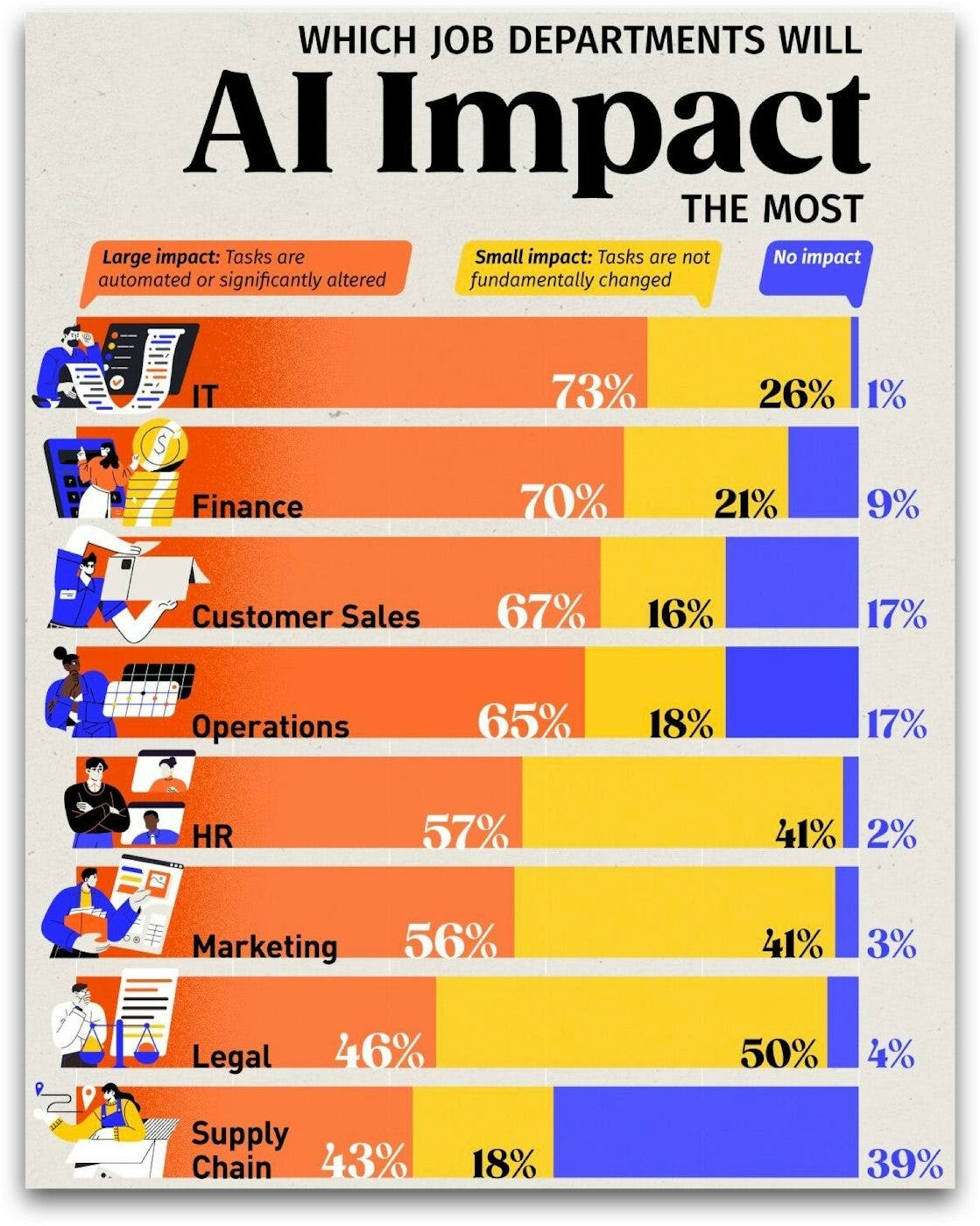

Generative AI automates 73% of IT departments, 70% of finance departments, 67% of customer sales departments, and 56% of marketing departments just to name a few.

All that said, current market trends among AI-centric stocks indicate some are correcting, influenced by higher-than-anticipated inflation rates that may keep rates higher for longer. The recent selloff in cryptocurrencies was triggered by the fear of inflation which could not only postpone rate cuts. But should leading AI tech juggernauts establish sound price floors or continue to trade sideways such as in the case of META, MSFT, AMZN, NVDA, and GOOGL, this could create undercut & rally, pocket pivot, or volume dry-up entry points.

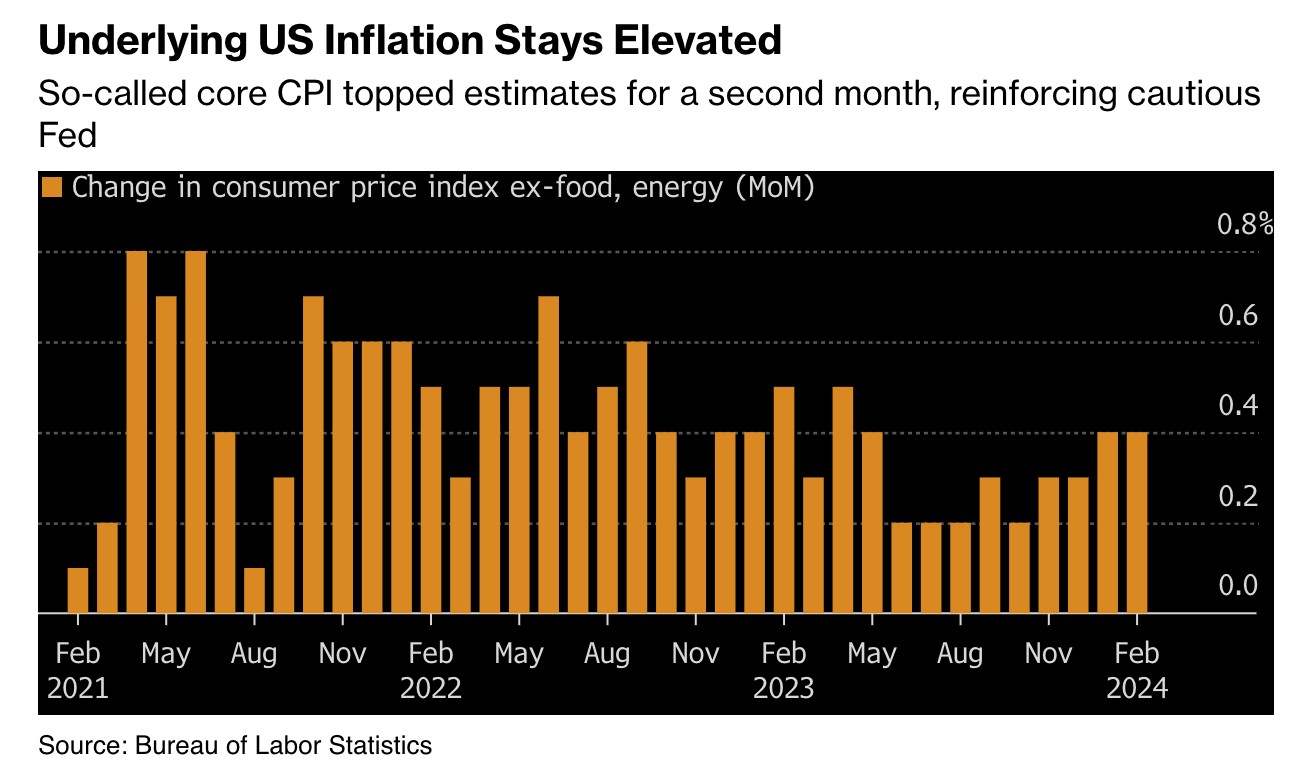

The Fed wants to avoid this at all costsThat said, the Fed will not be able to cut rates with inflation across CPI, PPI, and PCE staying stubbornly high despite moderating off peak levels. The core CPI has been rebounding since Aug-2023 from 0.2% to 0.4%, topping estimates.

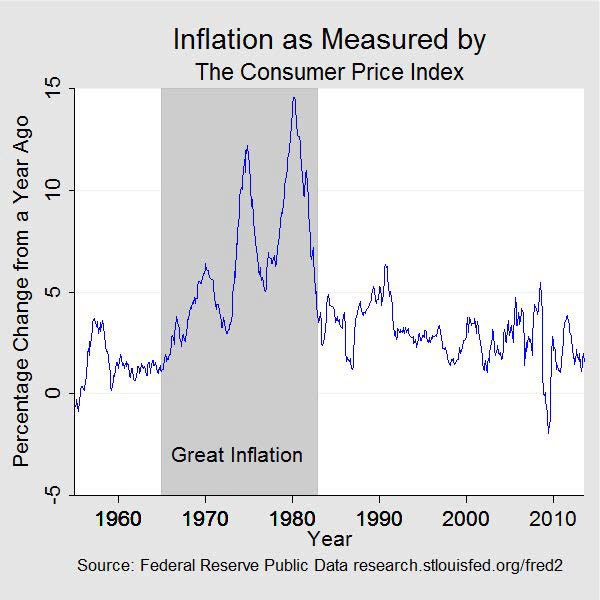

In the 1970s, we had what became known as The Great Inflation. Since late 2008, we have had quantitative easing which the Fed amply uses. This was a tool not used prior to 2008. It creates a substantial sum of money which degrades fiat. In other words, it creates inflation. The Fed wants to avoid a repeat of the 1970s.

Michael Bryan of the Federal Reserve Bank of Atlanta describes that time period where he writes:

“The Great Inflation was the defining macroeconomic event of the second half of the twentieth century. Over the nearly two decades it lasted, the global monetary system established during World War II was abandoned, there were four economic recessions, two severe energy shortages, and the unprecedented peacetime implementation of wage and price controls. It was, according to one prominent economist, “the greatest failure of American macroeconomic policy in the postwar period” (Siegel 1994).

Ken Griffin, the founder of Citadel, sees this rise in inflation as a key reason why the Federal Reserve should not rush to cut interest rates. Griffin said at a recent conference:

The Atlanta Fed's gauge of sticky inflation has risen to about 5% on a 3-month annualized basis. As inflation is starting to rise again, CME FedWatch now sees just three rate cuts by Dec-2024, down from the estimated seven rate cuts just a few months ago.“If I’m them, I don’t want to cut too quickly. The worst thing they could end up doing is cutting, pausing and then changing direction back towards higher rates quickly. That would, in my opinion, be the most devastating course of action that they could pursue. So I think they are going to be a bit slower than what people were expecting two months ago in cutting rates. I think we are seeing that play out.”

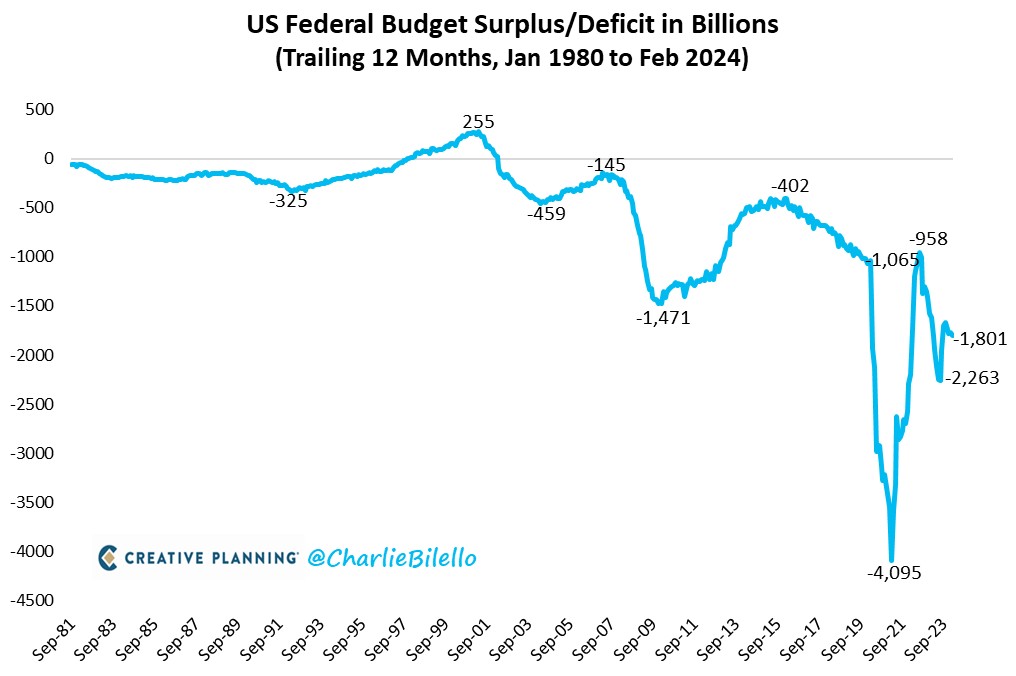

If the Fed were to start lowering rates prematurely while stealth QE remains in place and debt continues to climb to record levels, inflation could return with a vengeance. The US government continues to spend money in accelerated fashion as the budget deficit stands at $1.8 trillion. By contrast, between 1980 and 2019 or nearly 4 decades, the deficit typically ranged between a surplus of $255 billion and a deficit of $1.4 trillion. COVID created a deficit of more than $4 trillion, but since then, despite tightening, spending has never returned to baseline. And all of this spending is occurring when the economy is still in an expansion and home and stock prices are at record highs. Overspending seems to be the new norm while the federal deficit continues to reach new highs as interest payments alone now represent more than the total outlay for annual defense spending in the US.

Powell's testimony

Powell's favorable testimony emphasized how the economy remains strong by upgrading the growth outlook while unemployment is likely to remain stable. I would add that part of this strength is due to the utility created by AI. Its pace of development remains at breakneck speeds. He suggested that the recent inflation data that exceeded estimates was due to potential seasonal influences so it does not change the fact that prices are cooling, thus offering the possibility of rate cuts. He also mentioned quantitative tightening (QT) may soon slow.

Depending on the strength of the economy, we could get a situation where interest rates remain in place for over a year as they did from June 29, 2006 to Sep 18, 2007 when the Fed finally lowered rates. During this time, major stock market indices trended higher climbing a wall of worry due to rates being kept at "higher for longer" levels. Only after the first rate cut on Sep 18, 2007 did market troubles begin with the market putting in a major top about 6 weeks later. The first rate cut sometimes signals trouble ahead. Since the Fed tends to be behind the curve due to the way the system is structured, it is often too late for the Fed to rescue an economy that has started to falter.

That said, in today's market, the Fed has QE at the ready to save the day. Regardless, should such a "higher for longer" rate situation arise where rates are kept at current levels, as long as the economy continues to print strong numbers, expect this to favor the major indices and leading technology stocks.

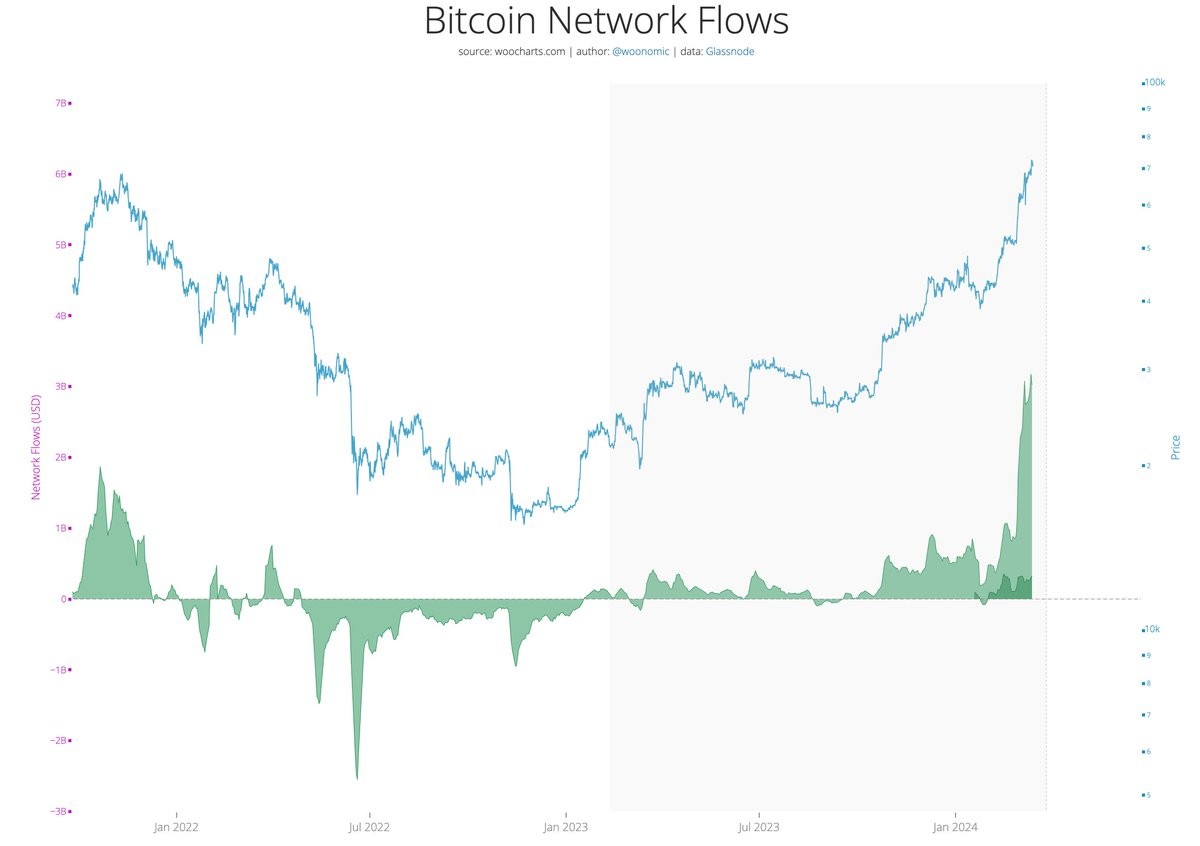

Bitcoin spot ETF inflows

Daily flows into Bitcoin visualised (rolling 7d average). The dark green patch starting in Jan-2024 is the influx from Bitcoin spot ETFs showing the ETFs are just getting started. Institutions and wealth management platforms will take a couple of months to complete due diligence before allocation begins, so this would contribute to daily flows into spot ETFs in the coming months.

That said, the selloff in Bitcoin which reversed to the upside today on the Fed's dovish testimony has increased outflows of GBTC while slowing Bitcoin spot ETF inflows. In consequence, Monday's and Tuesday's net inflows were negative. Nevertheless, stealth QE remains in place along with institutional buying of Bitcoin from spot ETFs plus the halving on April 19. Bitcoin had corrections weeks before the prior two halvings due to external news events. In 2016, it was the crash of a major exchange, then in Mar-2020, it was COVID. Without such events, Bitcoin would likely not have corrected.