Market Lab Report

by Dr. Chris Kacher

The Metaversal Evolution Will Not Be Centralized™

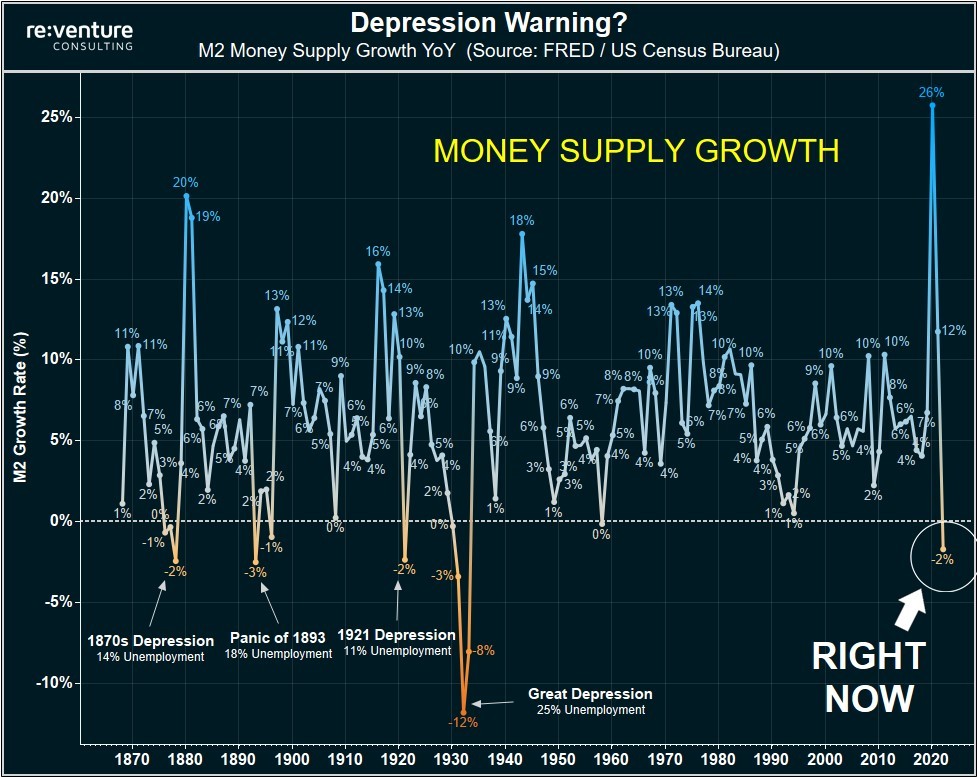

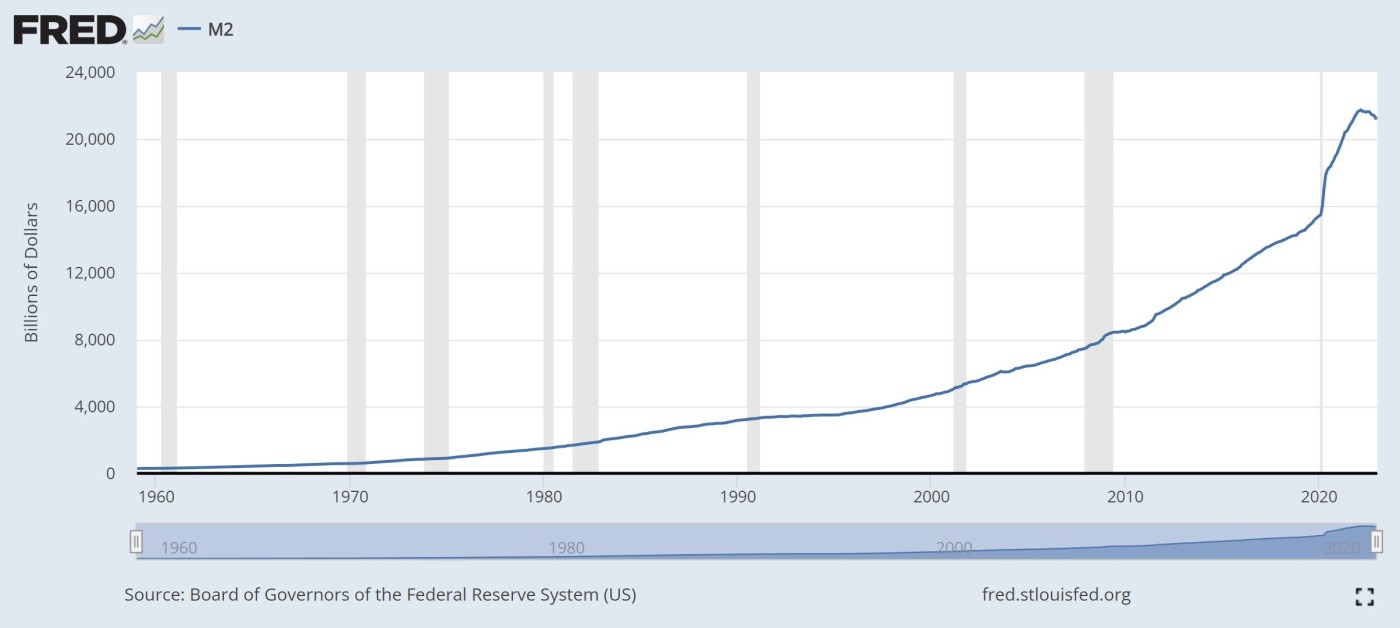

M2 contracting YoY

This is the first time since the Great Depression that YoY M2 money supply growth has become negative. This is due to the record pace of rate hikes from record lows since 2022. This has only happened 4 previous times in the last 150 years. Each time a depression with double-digit unemployment rates followed.

Contracting money supply + inflation means fewer dollars chasing rising prices. As one example, 1921 came after WW I and the Spanish Flu which brought on a 2% contraction in M2 resulting in deflation and soaring unemployment.

Ray Dalio thinks today resembles the 1930s of any decade. This is not the 1970s since M2 kept growing which caused a decade of high inflation.

A major war involving the US such as WW I and II or a black swan would push the Fed to print huge sums once again. This would likely start a new bull market. History shows something vital breaks in the economy when M2 contracts 2% or more resulting in a deflationary crash. That said, China and Japan are printing huge sums so global M2 is on the rise since late 2022. Global inflation could therefore persist as it did in the 1970s. Indeed, this time is different because in prior M2 contractions in the US, the rest of the world also contracted. Today, we have China then India as prime contenders to displace the US as the world's leading economy, thus money printing in China as well as in Japan more than offsets M2 contractions in the US, UK, and EU.

Bank failures the black swan?

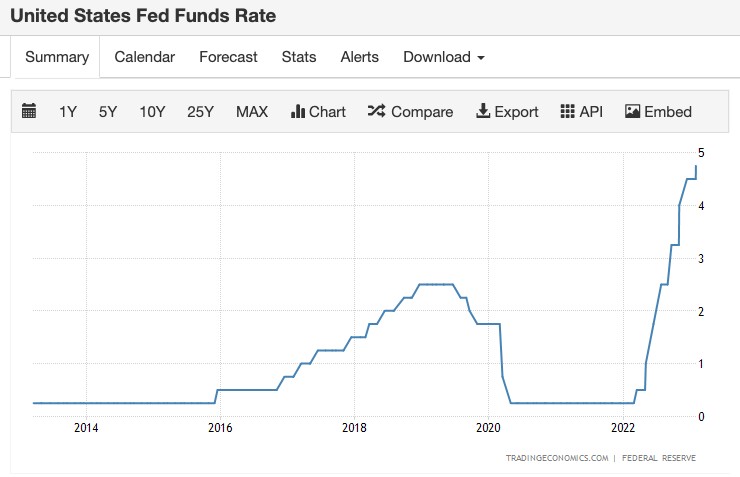

Nevertheless, we may have our black swan. The Fed hiked rates at unprecedented speed from near 0% to almost 5% over the last year.

This caused Silicon Valley Bank to fail. At $209 billion, it was the second largest bank failure ever. The bank also funds many tech companies.

Balaji Srinivasan nicely summarizes why SVB happened: 1) First, the state set up fake accounting rules. Those rules allowed banks to tell customers they had money when they did not have money. 2) Next, the Fed suddenly sent interest rates to the sky after years of keeping them near zero, denying inflation was a problem, and/or telling the world inflation was transitory. 3) Finally, banks that bought bonds under the Fed's misleading guidance got rug-pulled. Skyrocketing interest rates meant the government bonds they bought just a few months ago were suddenly far less valuable. So that's why people don't have the money in their SVB accounts. All their capital was used to buy bonds from the government, and the government allows banks to legally lie about this in their accounting. Uncle Sam is the new Sam Bankman-Fried. We cant trust the banks. That's why we need Bitcoin.

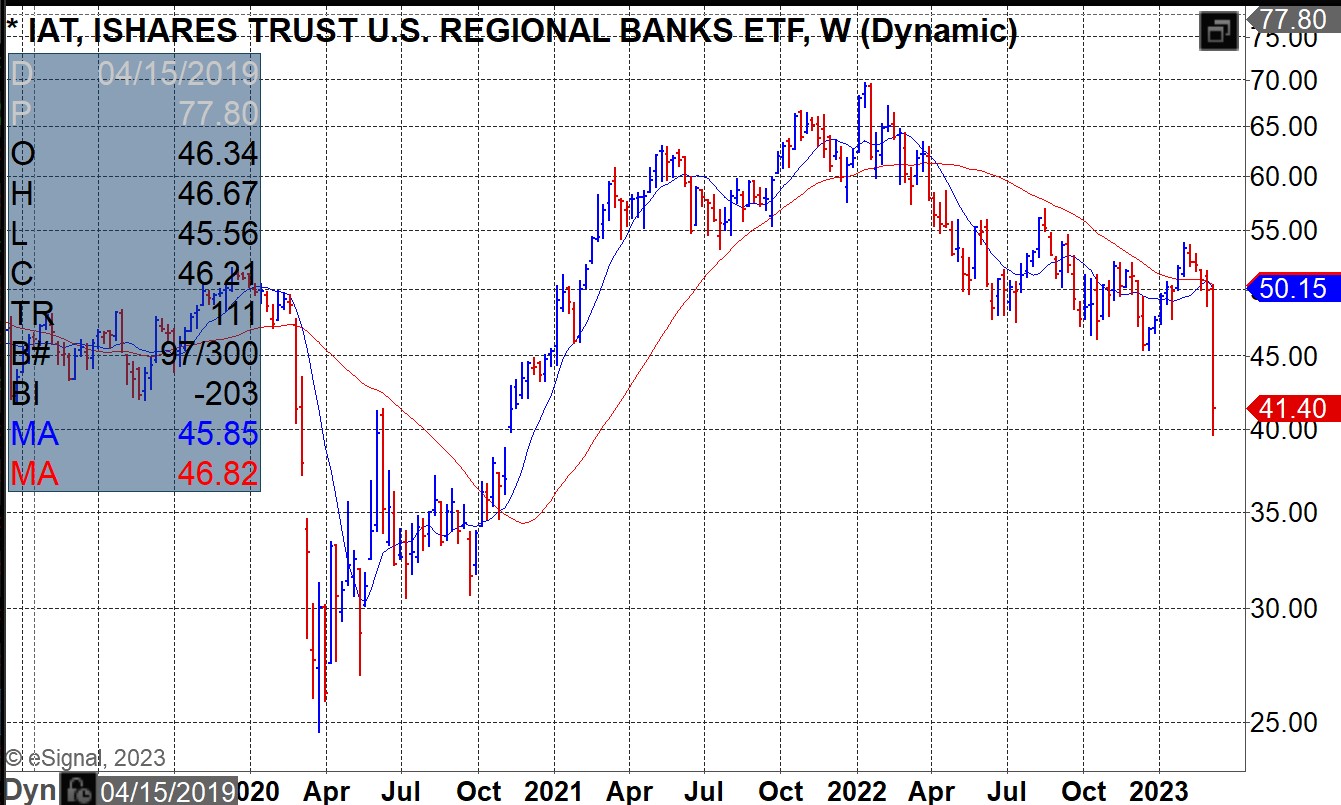

Silicon Valley Bank is likely one of many banks that would have failed if not for the Fed stepping in to guarantee depositors. This is not just a Silicon Valley problem but a regional bank problem as regionals are more vulnerable to having bond losses on their books than large banks as can be seen in the ETF.

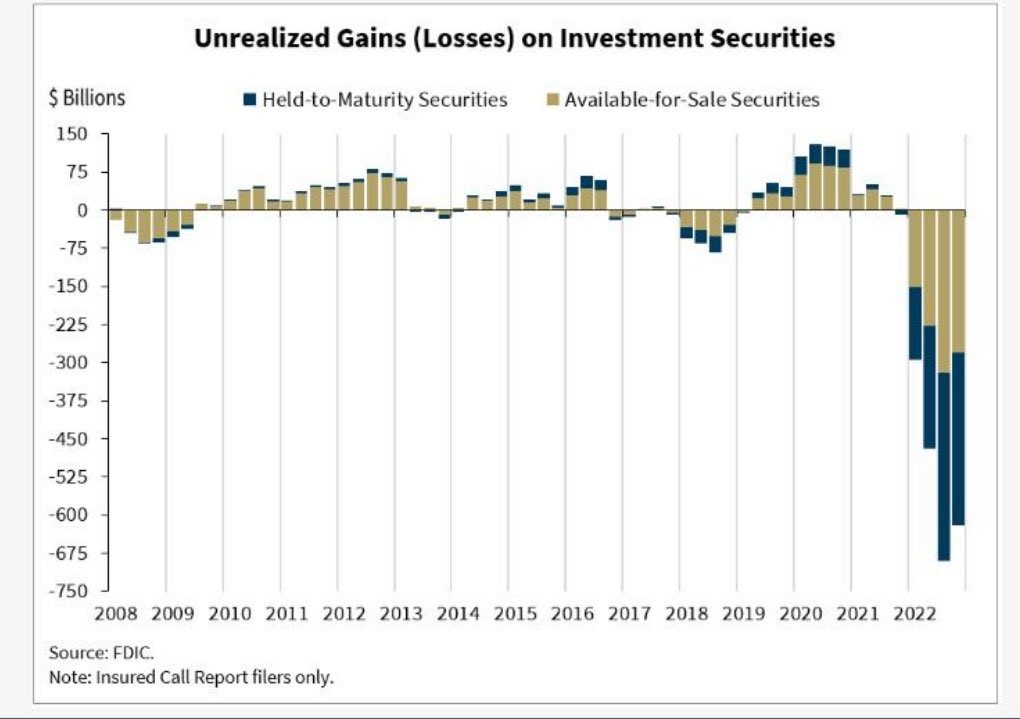

In addition, payroll processors would have been unable to provide for their thousands of tech company clients. The radical change in interest rates has put banks at risk who bought longer duration bonds when rates were much lower. Powell said that he wouldn't raise rates in April, June, July, and Oct 2021. Banks trusted him and bought bonds with billions in customer deposits because of those assurances. Now some are wrecked, and that's how the Fed caused the crisis. The unprecedented COVID-induced money printing followed by massive rate hikes have created $620B in unrealized bank losses, up from $8B a year prior.

When SVB was acquiring treasuries (mid-2021) at ultra low interest rates, 72% of the Fed presidents said rates would be under 1% in 2023, and 100% said under 1.75%. We are one quarter into 2023 at fed funds rate of 4.75%. With soaring rates, bond values plummet.

This is a perfect example of a completely inept and unaccountable institution which has been given a monopoly on money printing in America. This fiscal and monetary mismanagement is why central banks and fractional banking must eventually come to an end.

Replacements could be found within DeFi which could eventually co-exist with a highly evolved AI. Money prices, like any price, should be determined by a decentralized free market. This would spur self custody, privacy, and permissionless software which are essential. Blockchain is key here. Real-time, automated, on-chain balance sheet monitoring will outperform a system where financial regulators in the country did not know 36 hours before it closed that its 18th largest bank became insolvent. That said, this could usher in a US CBDC which could be created at will with nothing backing it, but then there would be no default nor bank run. This could also result in the replacement of stablecoins with a US CBDC.

The Fed announced they will protect all depositors which is helping to restore confidence through their newly created Bank Term Funding Program. They've pledged $25 billion but may have to do far more due to the $620 B in bank bond losses. According to JP Morgan, the Fed's emergency loan program may inject as much as $2 trillion of funds into the US banking system which will ease the liquidity crunch. Depending on the severity of the domino effect that may topple more banks, this is sounding a lot like QE, much as they did after the 2008 financial collapse or after COVID hit. Both times were the start of major multi-year bull markets. This could be the end of rate hikes and the start of the big print. Higher inflation would become the standard as the Fed would be forced to accept a higher inflation target well above 2% which Ray Dalio had predicted in one of his published pieces.

Some are finally understanding the anger that led to the creation of Bitcoin. Why would you trust a “government insured” bank that’s not actually insured, exchanges that go bust, stablecoins that depeg, or fiat currencies that make you poorer every year?