by Dr. Chris Kacher

Technology's vanguard

META and MSFT both had strong earnings reports suggesting cutting edge tech continues to lead. When it comes to AI, the companies with the biggest wallets get the best data, the fastest chips, and the most entrenched customer base. More users means more data to train AI models which implies the most robust tools. Such becomes self-reinforcing. The other Magnificent Seven companies are also participating to keep their lead. Nvidia’s GPUs are the backbone of nearly all advanced AI training and inference worldwide. Its chips power the data centers and cloud platforms of the world’s largest tech companies, making Nvidia central to the AI boom. The lifting of Biden's AI chip export restrictions are a major tailwind for NVDA. Alphabet (GOOGL) invests billions in AI, from search and advertising to cloud and autonomous vehicles. AMZN Web Services (AWS) is a top provider of AI and machine learning tools for businesses worldwide. AAPL integrates AI into its hardware and software ecosystem, powering features like Siri, personalized recommendations, and device security. TSLA's AI is at the heart of its Full Self-Driving (FSD) software, using vast amounts of real-world driving data. Tesla is developing Optimus, a humanoid robot, and expanding AI applications in manufacturing and energy management.

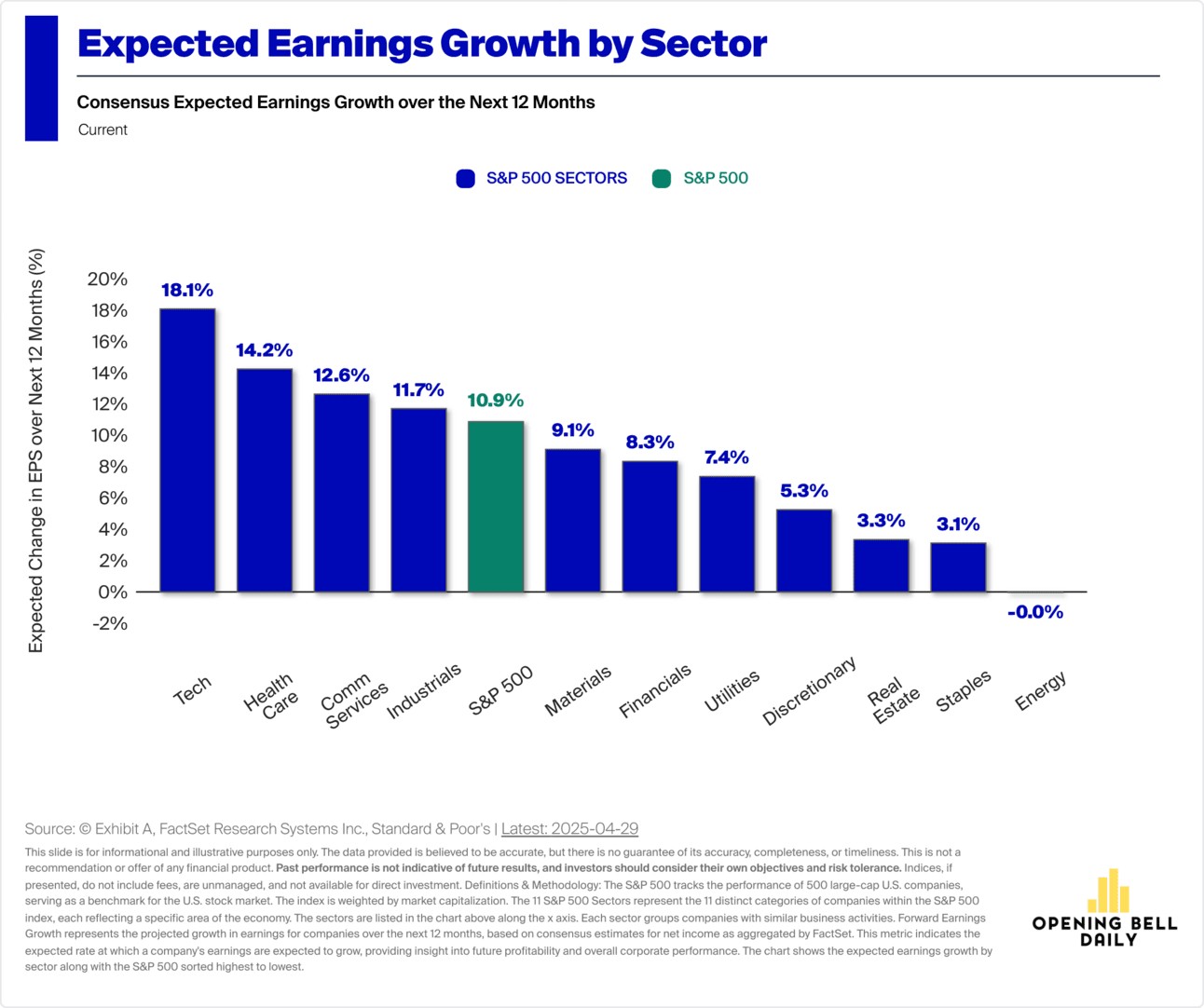

Indeed, the S&P 500’s technology sector continues to lead in expected earnings growth over the next 12 months at 18.1% compared to the S&P 500 overall at 12.8%. Overall, S&P 500 earnings so far this quarter are outperforming prior quarters. With about 72% of companies reporting, the index is showing a year-over-year earnings growth rate of 12.8% for Q1 2025. This marks the second consecutive quarter of double-digit earnings growth and the seventh straight quarter of year-over-year earnings gains. Additionally, 76% of companies have reported positive earnings surprises, and 62% have reported positive revenue surprises-both strong figures compared to historical averages. These results are notably stronger than in previous quarters, reflecting robust performance, particularly in sectors like technology, health care, and consumer discretionary.

Gold vs Bitcoin

Gold tends to lead bitcoin by 90 to 180 days.

This holds true going back many years. Gold is the risk-off harbinger of inflation or crisis. Bitcoin which is risk-on then follows typically after 90 to 180 days after fear has subsided, giving investors more reason to become risk-on.

Global liquidity

The People's Bank of China cut lenders' reserve requirement ratio by 50 basis points allowing them to loan more money out, while its seven-day reverse repo rate was reduced to 1.4% making loans more accessible for its citizens. Global liquidity is just ramping up. China's central bank injected 1 trillion yuan ($140 billion) 3 hours after agreeing to trade talks to prop up its economy and give the communist party ammo for negotiations. The 145% tariffs are forcing China's hand. The same could be said for other central banks as tariff negotiations unfold. This might be why markets have clawed their way back since their mini crashes.

The Fed held rates steady so will likely be behind the curve once again. They need to see more evidence in the data for a rate cut because at present, they claim the economy and the jobs market are holding up though did express concern that if these tariffs are sustained, they are likely to raise inflation, slow economic growth, and increase unemployment. We are seeing an economic slowdown because of the potential tariffs, which can be seen by the slowing rate of inflation, so the stimulus from a rate cut would help spur economic growth. Nevertheless, the Fed is adopting a cautious “wait and see” approach, monitoring how tariffs and other policy changes affect the economy before making further moves. Powell declined to commit to any rate cuts this year, stressing the need for more data as the situation evolves.

But whether now or later, the direction of global interest rates remains lower. As QE continues, bitcoin should push higher especially as investors have so far invested more capital into Blackrock’s bitcoin ETF than the largest gold ETF. As of early May, BlackRock’s IBIT has attracted $6.96 billion in net inflows for the year, slightly surpassing GLD’s $6.5 billion over the same period. But bitcoin remains more risk-on while gold is more risk-off thus bitcoin has been met with more selling thus gold has outperformed for now.

That said, as we get clarity on tariffs, we should expect asset prices to continue to recover. So far, the recovery has happened without a single trade deal announced or the Fed cutting interest rates. And trade deals and rate cuts are coming. In fact, Trump just revealed a comprehensive trade deal with the UK and a rare earth deal with Ukraine. Although it is only the first deal, announced deals brings certainty and certainty brings higher asset prices. Contrast this with early April when markets had mini-crashes due to maximum uncertainty regarding the tariffs. This caused sentiment to reach near all-time lows across retail and institutions. Even Bank of America told clients to short the market on April 11.