Market Lab Report

by Dr. Chris Kacher

The Web3 Evolution Will Not Be Centralized™

Big Tech Juggernauts buoyed by liquidity

MMANGA big tech stocks (Meta, Microsoft, Amazon, Nvidia, Google (Alphabet), Apple) have well outperformed because they are in a virtuous circle where fund managers must hold some of each or risk underperforming. Further, it is a bet that these companies are in a great position to capitalize on AI which will increase profits, in part from direct AI use within the organization and also from the need for fewer employees.

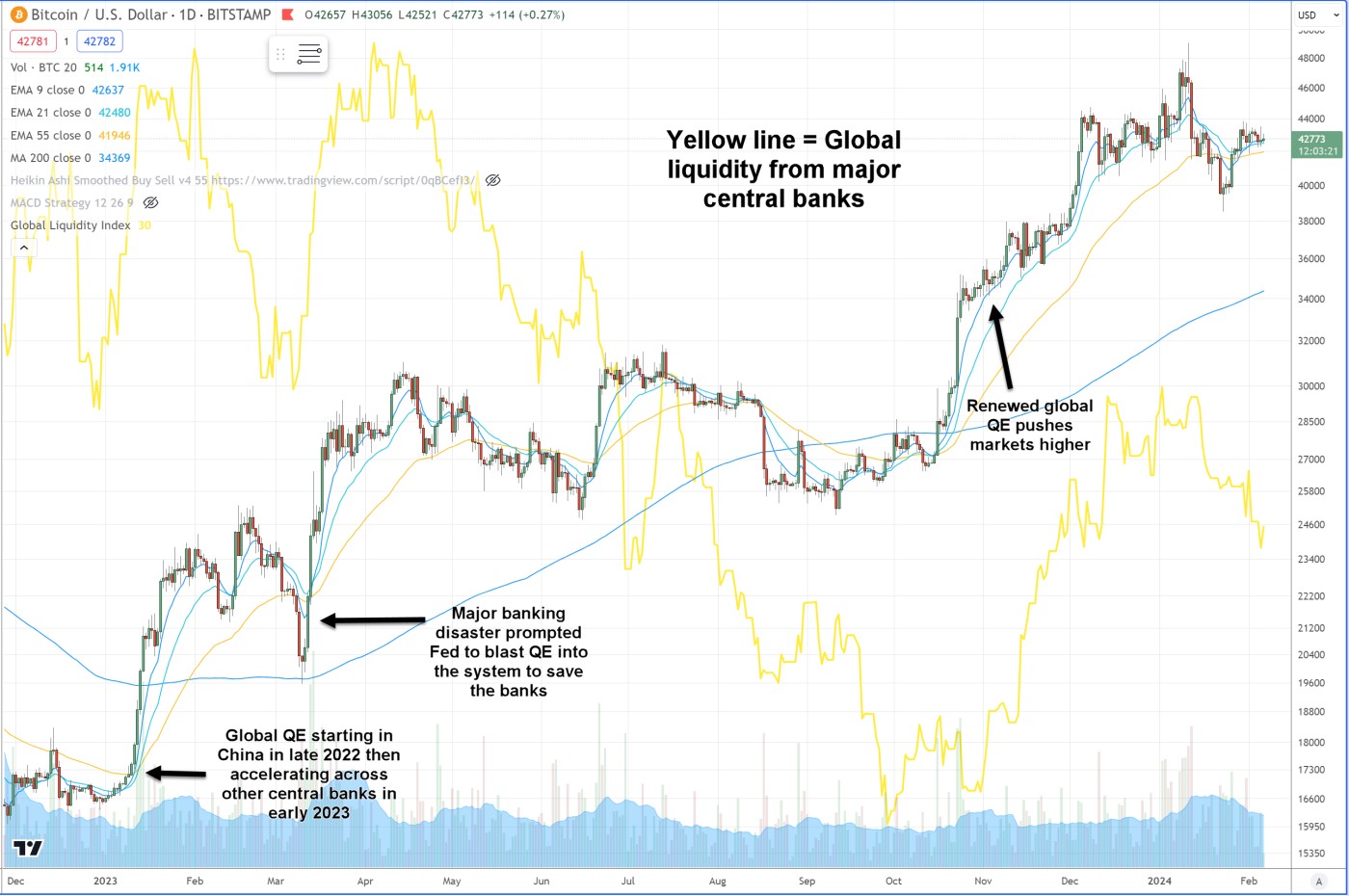

Increasing global liquidity will find its way into major assets such as these MMANGA stocks, though since the start of the year, liquidity has been in a mild downtrend. Predictions about recession have been pushed back to sometime in the second half of this year. If you take the difference in yield between the 10Y and 2Y bonds, when the yield curve inverts as it did in 2000 and 2007, a deep recession came the following year.

Yield curve to uninvert?

The uninversion of the yield curve may get postponed should the current rise in yields and strength in the dollar prove temporary. While the Fed has taken a more hawkish position as of late as they continue to maintain their mandate is to reduce inflation back to 2% while keeping employment healthy, they will continue to boost liquidity though only "just enough" so they keep inflation at bay. However, any black swan such as future major bank failures should the BTFP not be extended may force the Fed's hand as it did in March 2023. Regional banks are not out of the woods as NYCB and COLB both gapped lower recently.

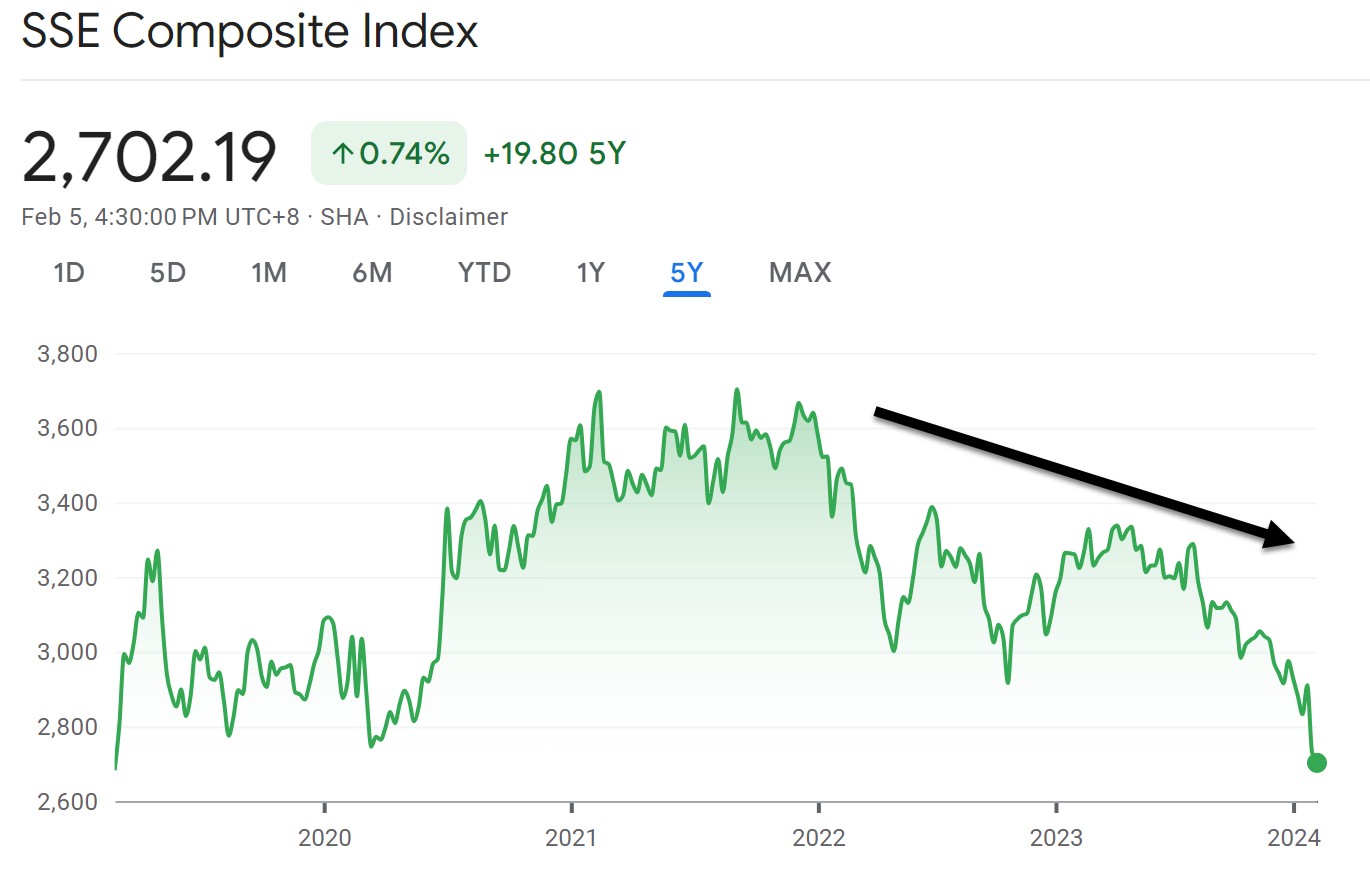

Former predictions of recession made in 2023 had to be pushed forward by a few quarters. The Conference Board is forecasting "GDP growth to turn negative in Q2 and Q3 of 2024," up from prior calls for a recession to start sometime in 2023. The huge gains in utility could postpone recession. Such comes from cutting edge technologies such as AI as well as liquidity from central banks such as in China to prop up their stock market with the equivalent of about $280 billion in yuan which has been in a nasty downtrend despite the exchanges of other major countries heading higher since late 2022. The Shanghai Composite index recently fell to five-year lows but analysts say propping up the market with cash can't be sustained due to an ailing property market which affects consumer and investor confidence. As rates were hiked aggressively in 2022, China's bloated real estate market was particularly impacted. Escalating tensions with Washington on trade and record numbers of labor strikes in China add to revolutionary pressures. The task is also giant: mainland stocks are worth nearly $9 trillion.

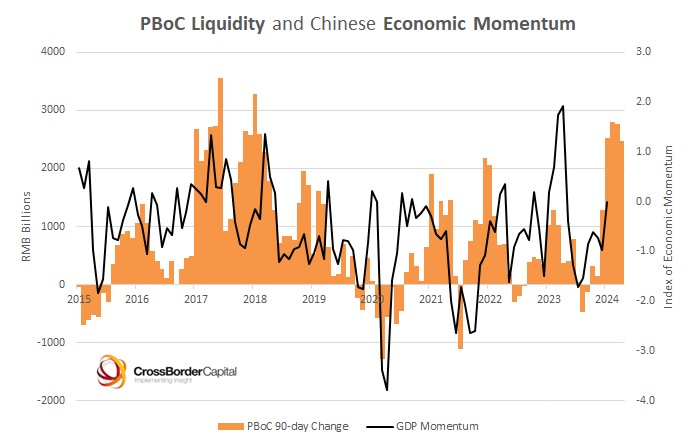

Legendary investor Jim Rogers has said he fades central banks that try to prop up their stock markets or fiat currencies if the fundamentals remain problematic. Things in China are likely to get worse before finding a floor despite government intervention. When the GDP growth of China was outpacing most of the world, this growth was largely due to overleveraging in real estate. In fact, they had three and a half more times banking leverage than the US. The two largest property developers in the country which have blown apart, Evergrande and Country Garden, have more than $500 billion in debt combined. After an unregulated and unabated climb in real estate, we are now seeing a real estate collapse which is affecting China's stock markets. The likely solution seems to be more QE from the PBoC (People's bank of China). PBoC liquidity helps China's economic momentum. Rising QE will help global markets as everything is more interconnected than ever. QE capital finds its way within the digital landscape.

Rates higher for longer?

Concerns that rates may remain higher for longer can pressure real estate prices, stocks, bonds, and cryptocurrencies. Yields on the 10-year and the dollar have both been trending higher. CME FedWatch predicts the next rate cut will be in May with a terminal rate of 400-425 bps by the end of the year for a total of 5 cuts. Global liquidity also remains in a downtrend since the start of the year. Liquidity is the force that props markets higher. We can see how it correlates well with the price of Bitcoin which is a measure of value against falling fiat currencies since Bitcoin is regulated by unalterable code, not politicized central bankers who are under constant pressure by their respective governments.