Market Lab Report

by Dr. Chris Kacher

The Web3 Evolution Will Not Be Centralized™

Drunken sailors

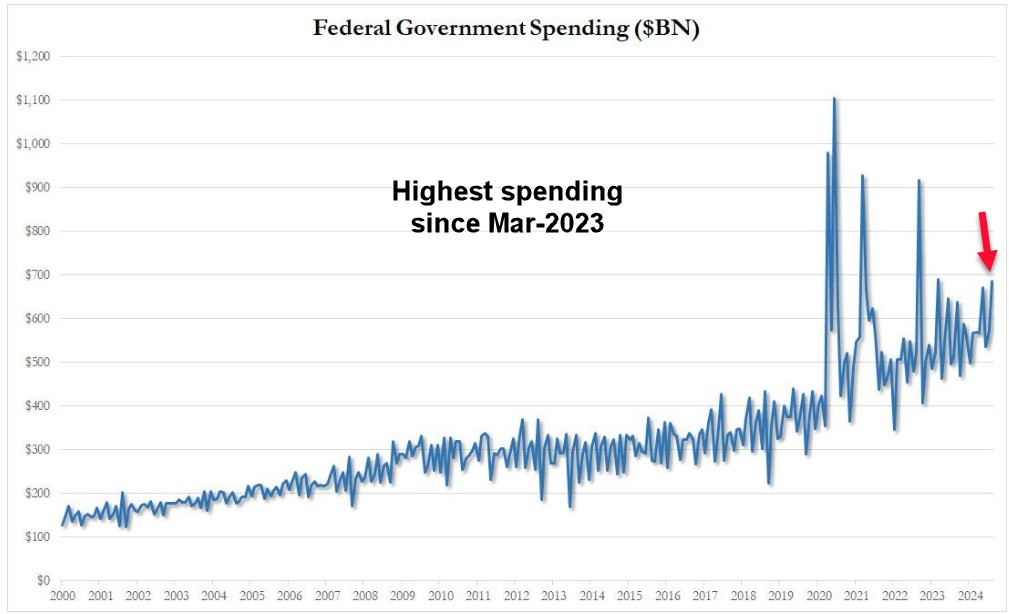

The August budget deficit hit a staggering $380 billion.

The Biden administration intentionally spent big to reboot the economy so we don't get a recession just in time for the elections. Outlays hit $686 billion, the highest since March 2023, and only a handful of crisis months during the covid crash saw greater government spending in any given month.

Keep in mind this does not include stealth QE where spending has been greater since Jan-2023 than during the first two years of COVID.

So of course the Biden admin will spend what it takes to paint the political tape.

Fed meeting

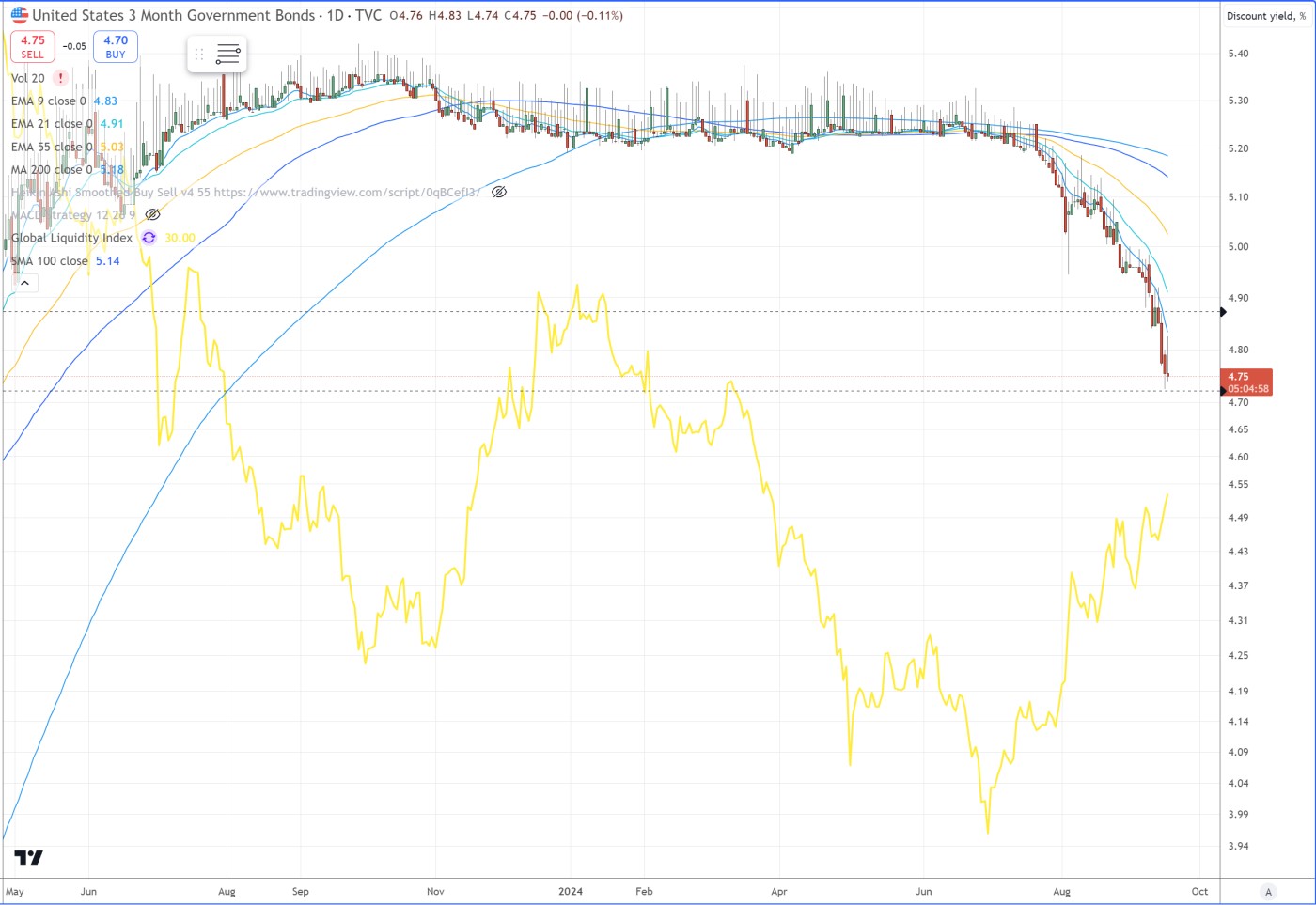

The central bank reduced rates for the first time since 2020. I strongly suggested a 50 bps rate cut based on 3-mo T-bills which were heavily projecting such a rate cut.

It is the last meeting before elections on November 5. CME FedWatch is now placing odds of a 25 then 50 bps rate cut when it meets again in November then December.

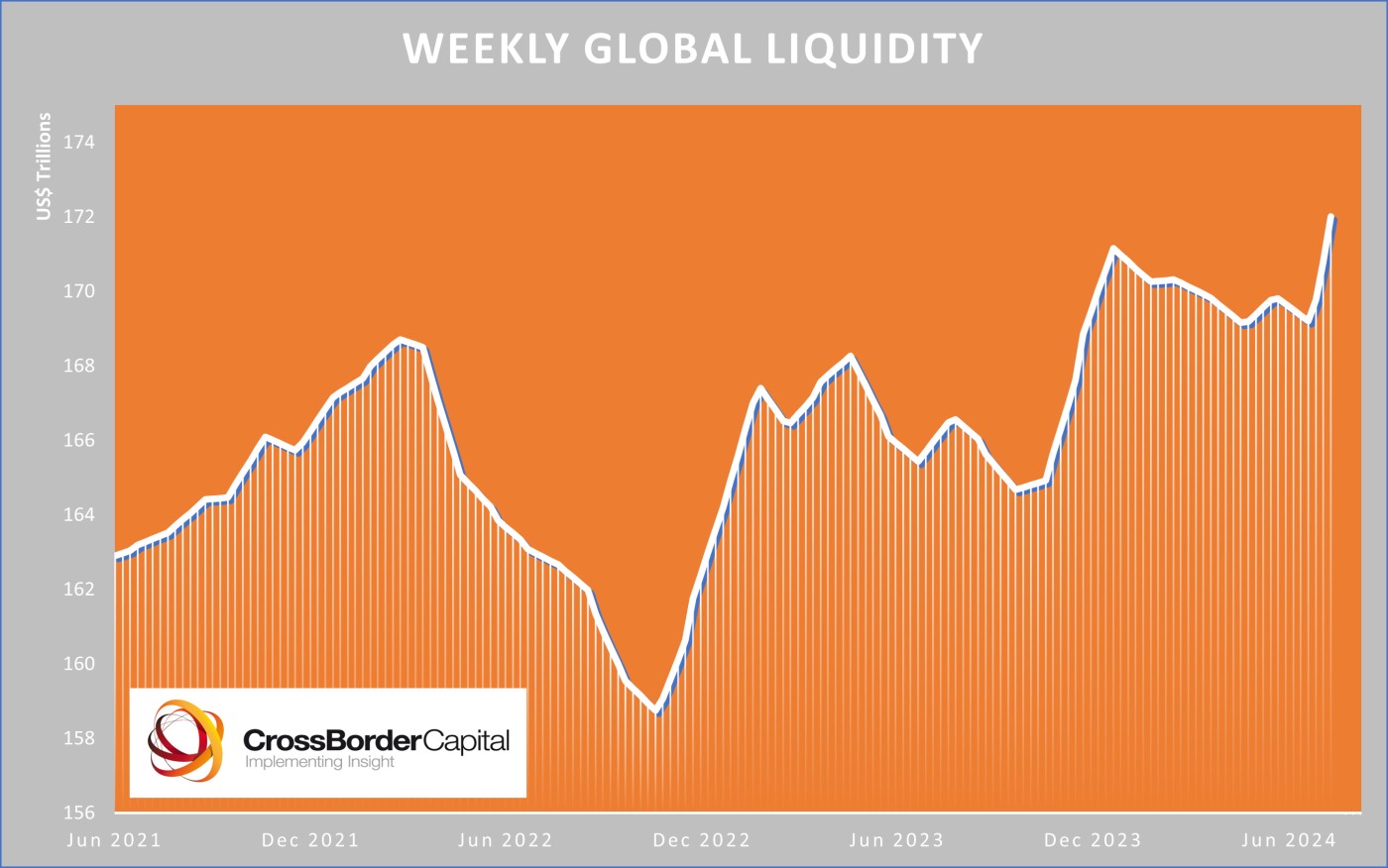

Powell's testimony went as expected. He was mostly the bearer of good news and positive expectations for the future. He emphasized how the economy is doing decently, inflation will continue to fall, and unemployment will be tempered. Markets reacted somewhat positively though were volatile. Overnight, at the time of this writing, futures are projecting a 2% gap higher in the NASDAQ-100. The stocks we suggested in our weekend's Focus List Review are looking to continue higher. Liquidity at home and abroad continues to break to new highs when accounting for central banks as well as private sector liquidity which includes all flows of cash and credit.

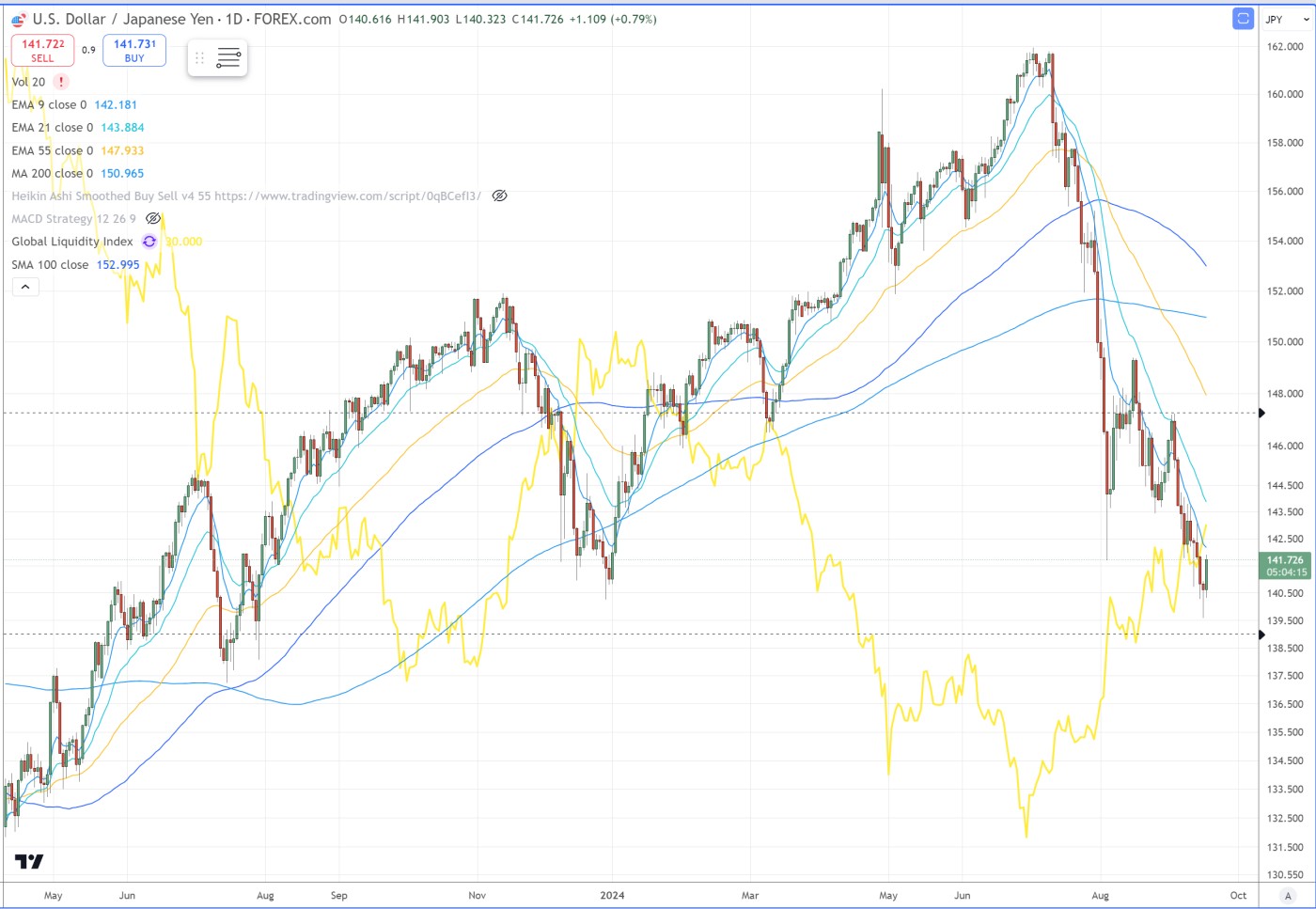

Strengthening yen

While concerns remain about the strengthening yen, the Bank of Japan has said they will not be raising rates. In addition, some ‘deal’ was potentially agreed between the US, Japanese and Chinese authorities to weaken the US dollar slightly which allows global liquidity to expand further while giving China the window to add vital liquidity to their markets.