by Dr. Chris Kacher

Bond market omen

The country that controls the bond market controls the future. Adam Smith once wrote that the Navigation Act of 1651 was protectionist legislation targeted by Britain on Holland designed to cripple Dutch trade. Smith said the act was “..the wisest of all the commercial regulations of England” because Holland is “… the only naval power which could endanger the security of England.”

Similar could be said today in the US vs China trade war. Indeed, Trump's tariffs against China which currently stand at 145% are “..the wisest of all the commercial regulations of the US” because China is “… the only power which could endanger the security of the US.”

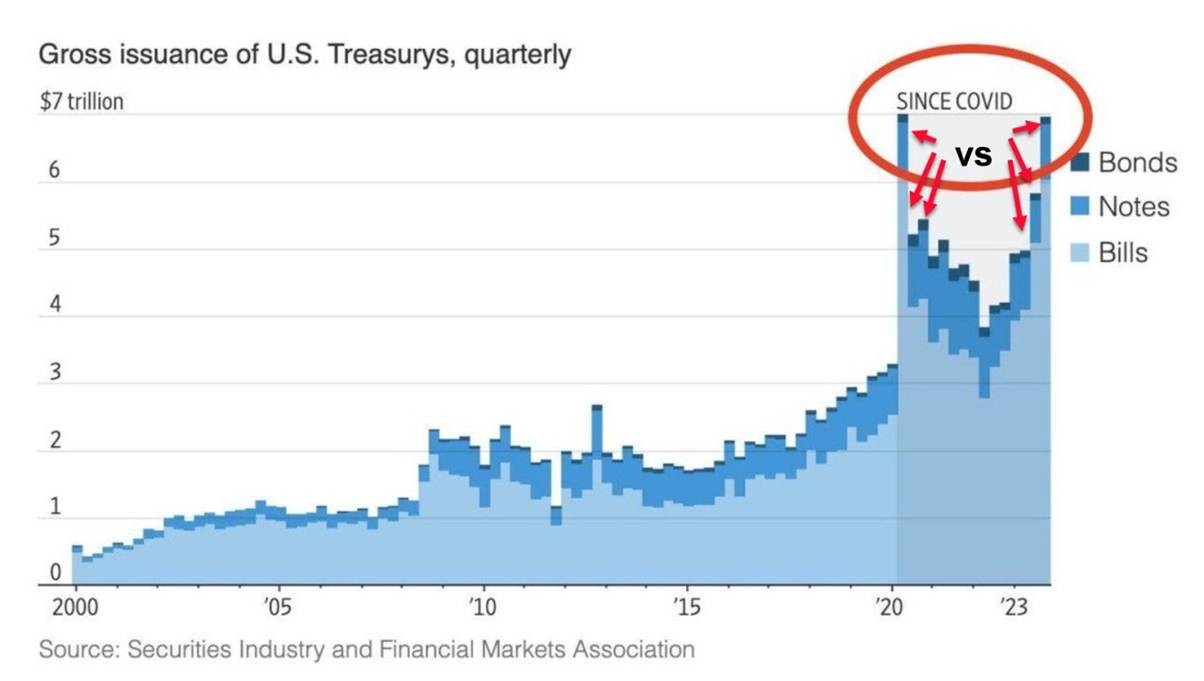

China’s economy will be hurt badly especially given China’s credit plight. However, the Achilles Heel of the US is their bond market which will refinance US$9-10 trillion of debt this year at the lowest interest rates possible. If China sells part of its US$720 billion inventory of US Treasuries, yields will rise to cause maximum yield pain to the US. But China's $3 trillion in total dollar assets (including agency bonds) equals ~15% of its GDP. A fire sale would destabilize its own financial system and trigger yuan appreciation, harming exports. With 23% of Chinese corporate debt in distress and property sector crisis ongoing, Beijing prioritizes financial stability over geopolitical brinksmanship. A Treasury dump could spark capital flight, worsening its credit crunch. Analysts estimate China could sell $200–300B (~1.5% of Treasury market) before losses outweigh geopolitical gains. This would spike 10-year yields by 30–60 bps temporarily. The US retains greater capacity to absorb shocks through Fed tools and deep markets, making Treasury weaponization a high-cost, low-reward tactic for China.

Nevertheless, there is also the issue of Global Term Premia where interest rates are globally on the rise.

For example, Germany plans to issue €1 trillion+ in new debt over the next decade to fund infrastructure, defense, and climate initiatives. German 10-year yields spiked 43 basis points in one week, the largest jump since 1990, narrowing the gap with US Treasuries. This makes German bonds increasingly attractive over US Treasuries.

There is also the unexpected rise of Japanese inflation which has contributed to upward pressure on US Treasury yields. Higher Japanese bond yields reduce the attractiveness of US Treasuries. Japan alone holds ~$1.1 trillion in US debt.

As you can see, the yield on the 10-year shot higher at one of the fastest rises in history.

So despite CME FedWatch anticipating 3 to 4 more rate cuts this year, other factors could push US Treasury yields higher. If such occurs, the Fed could restart QE, as in 2020, to cap or lower yields. They could also force domestic buyers such as pension funds, insurance companies, and banks to absorb any selling by other countries.

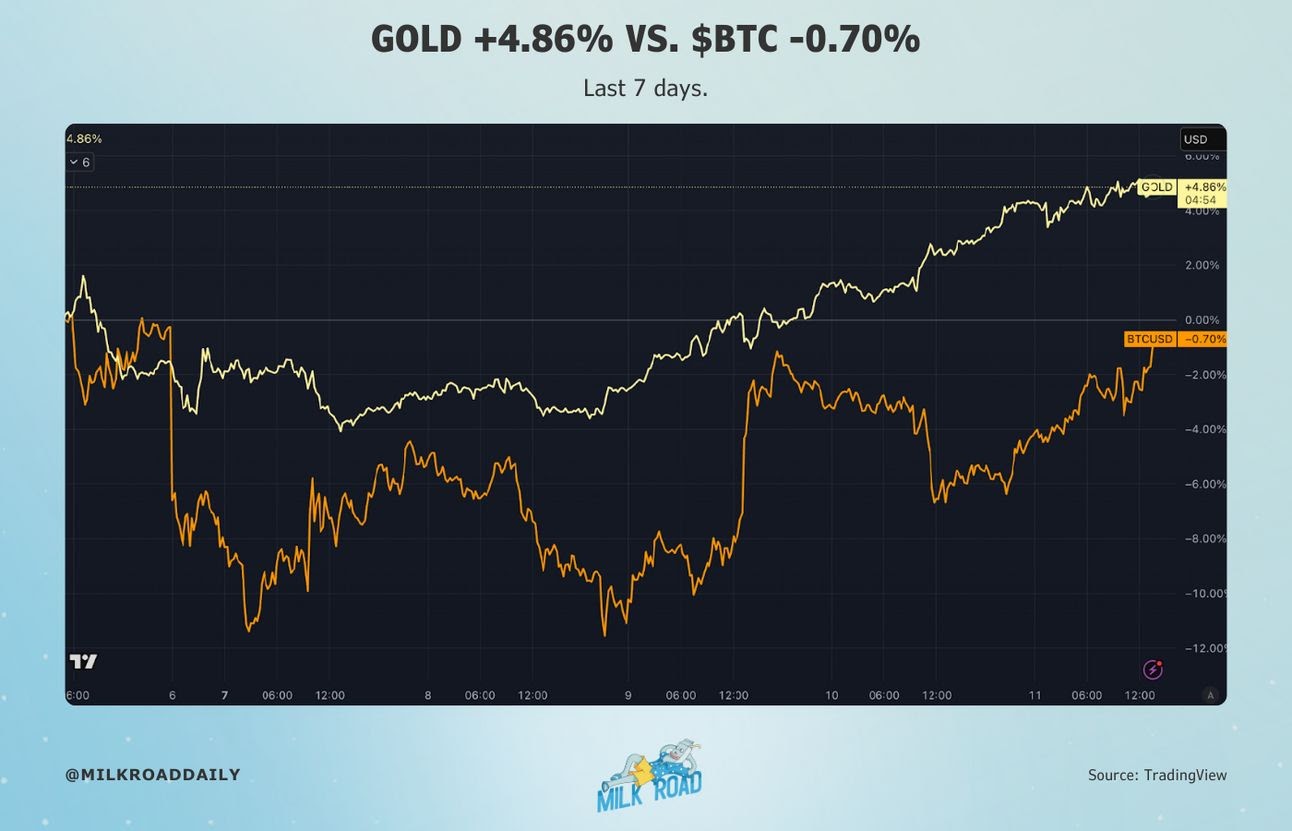

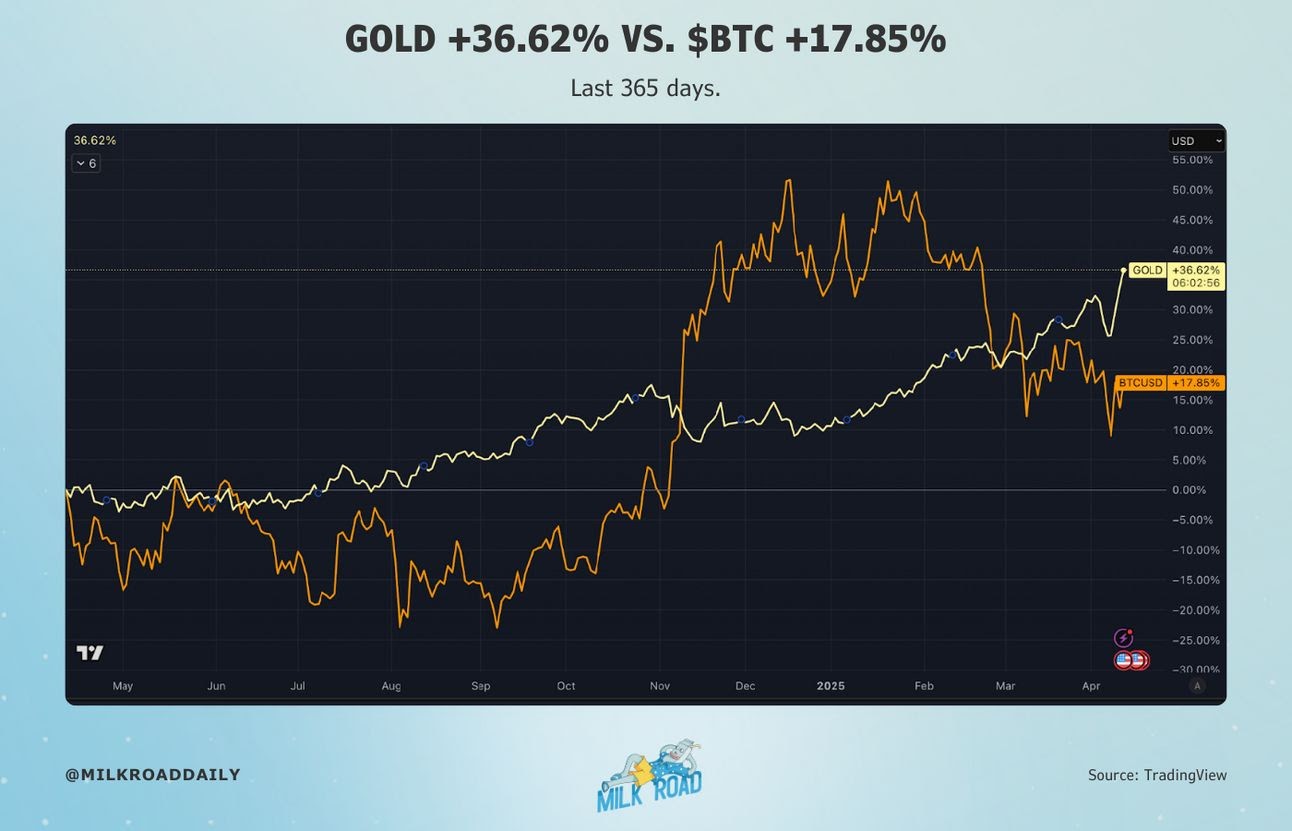

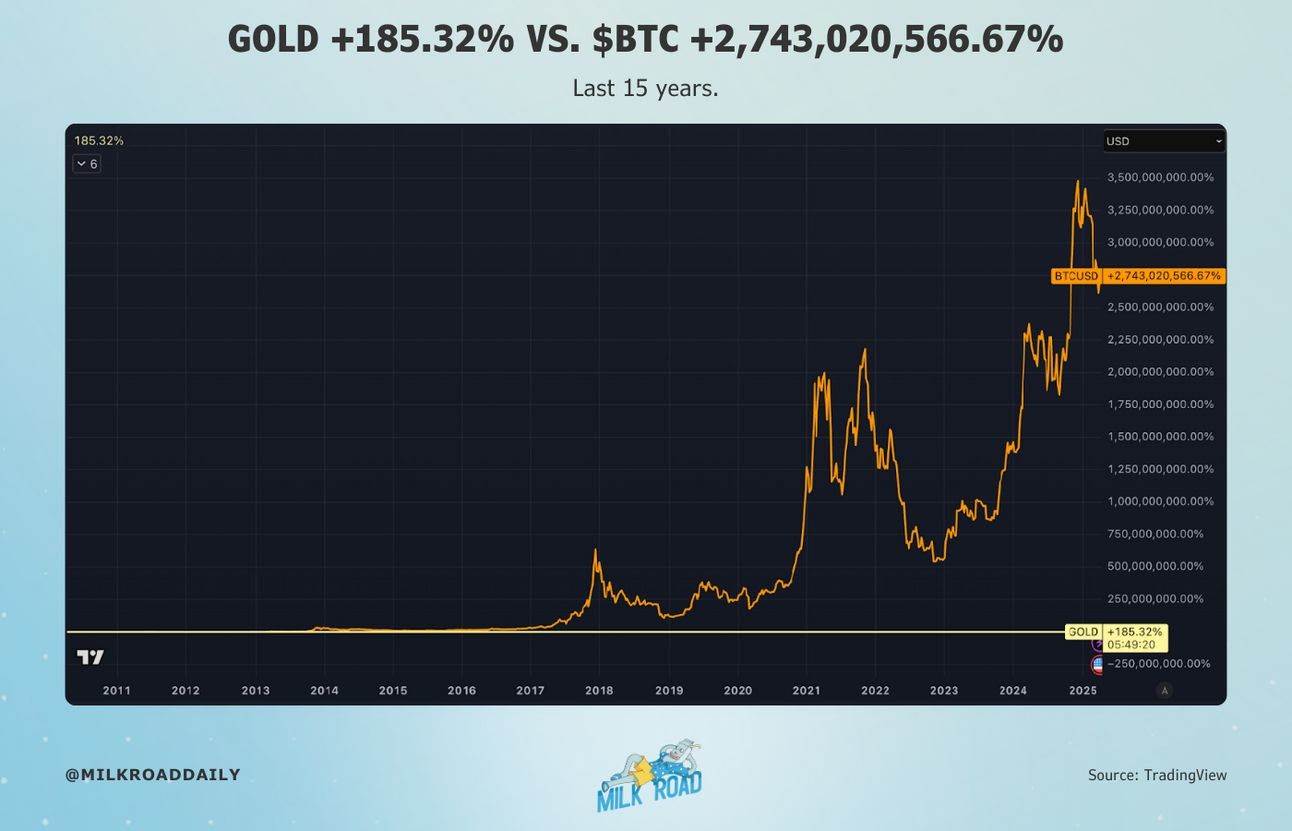

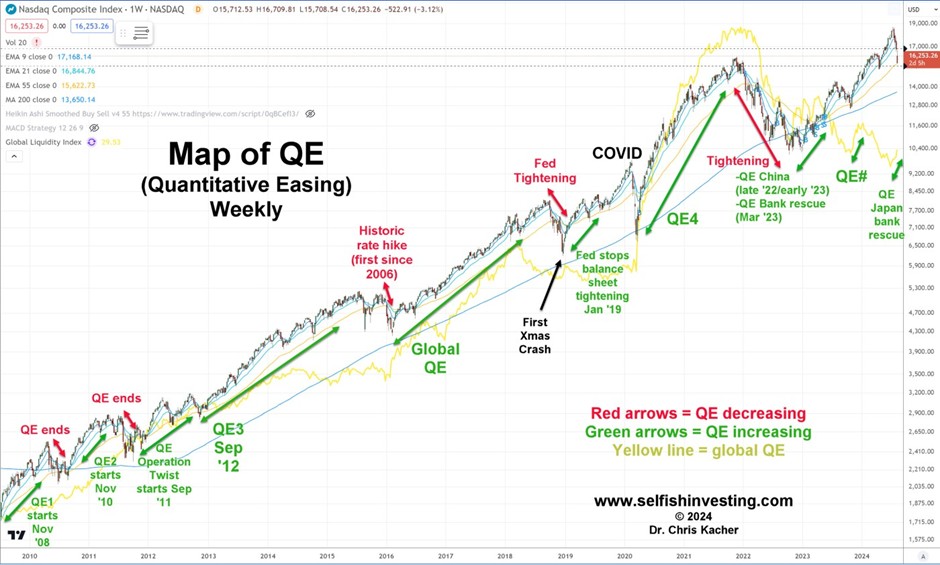

QEndless: Bitcoin vs. gold vs. fiat

Performance comparisons over various timeframes. Bitcoin represents the devaluation of fiat. As long as central banks and fractional banking remain in place, the inflation megatrend will continue. Bitcoin, stocks, and real estate will continue to hit new highs.

The highest alpha vehicles such as ETFs TQQQ and TECL along with BTC vehicles are the best bets for the long term health of one's portfolio. My macro/global liquidity timing system captures the major trends since the NASDAQ Composite, leading stock ETFs, and BTC correlate to near perfection on a quarterly basis.

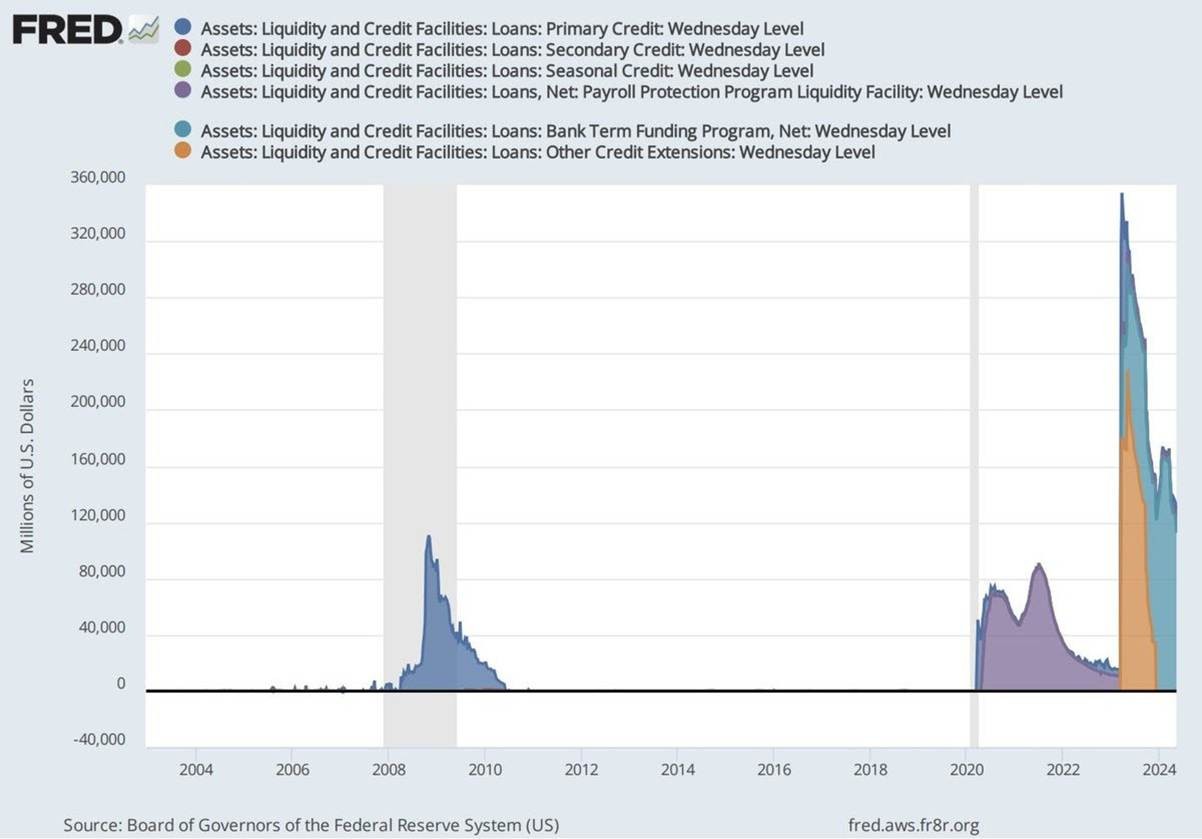

The QE money train will not stop. The Fed made more emergency loans in 2023 than during the financial crisis of 2008 and during COVID of 2020. We had one of the largest banking crises in 2023 because the US government first sold billions in bonds to financial institutions then devalued them by hiking rates at the fastest pace in history from near zero levels.

The blue bump below on the left is the lending from the global financial crisis of 2008, the purple bump is COVID, and the orange/aquamarine monster on the right is the 2023 banking crisis.

The US government also printed more under the "Biden boom" than it did during COVID. COVID borrowing was at ~0% rates but today's borrowing is above 5%.