Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

The Evolution Will Not Be Centralized™

Brighter skies ahead?

As prior reports stated, the bounce is looking more like a sustained uptrend. More progress was made between the US and China on the tariffs matter. The US will cut tariffs on Chinese goods to 30% from 145% for 90 days, and China will lower tariffs on US goods to 10% from 125% for 90 days.

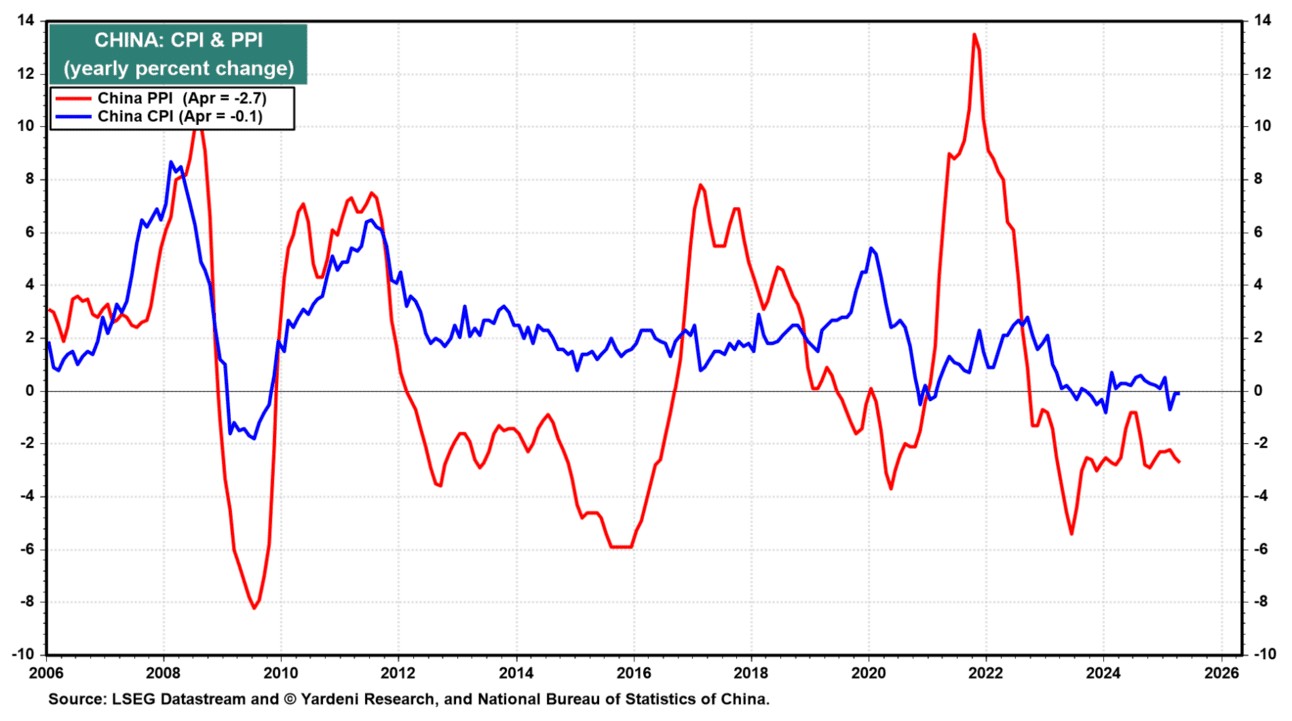

Markets are pressuring a trade deal get done satisfactorily between the US and China. While Trump has said he will not let markets lead him by the nose, when markets had their mini-crash, the Trump administration took notice thus took prompt action which pushed markets higher. Meanwhile, China has been attempting to manage deflation, collapsing factory activity, and faltering consumer demand. Prices in China have dropped for 31 months in a row. The nation’s troubling trajectory resembles that of Japan in the 1990s which suggests China is looking for a tariff deal sooner than later.

Yardeni analysts wrote, “President Trump’s tariffs are a hurricane-force headwind that China hardly needs. Even if Trump’s claim that the China tariff will be slashed considerably holds, a 30% import tax is still no joke. We think the trade issue will be behind us by July or August. If so, then the focus should be on how much Trump's tariff skirmishes weighed on the economy and earnings. We expect both will remain surprisingly resilient.”

Markets are always forward-looking. They continue to see more trade deals on the horizon, and the price action suggests a friendlier White House as well as a belief that the worst of the tariff shock is behind us. The Fed has also said that while they are not beholden to Trump or to the markets, if liquidity becomes an issue, they will step in with various forms of quantitative easing which could be in the form of lower rates among other tools at their disposal. This is known as the Fed put where markets have a floor of sorts since liquidity generally correlates with market direction at least on a quarterly basis if not much sooner.

As for inflation, it slowed to its lowest pace since 2021. The core CPI came in 0.1% under estimates at 0.2%. Analysts had expected tariffs would add maybe 6-7 bps to core inflation readings in April, with the bulk of the tariff-passthrough effects to come later in Q2 or in Q3.

Bitcoin, COIN, et al

Wall Street is quickly embracing Bitcoin and crypto, as shown by several major developments: Coinbase is becoming the first crypto company to join the S&P 500, DeFi Technologies has started trading on Nasdaq, and new bitcoin treasury firms like Nakamoto are raising hundreds of millions of dollars, while companies such as MicroStrategy and Metaplanet are making large bitcoin purchases. This wave of activity shows that traditional finance isn’t being left behind by crypto. Instead, asset managers, hedge funds, and banks are actively profiting from the sector’s growth, with index funds and institutional investors gaining exposure as digital assets go mainstream. Those who ignore this shift risk missing out, as significant value is being created for anyone willing to engage with crypto, regardless of background or wealth. Crypto’s rise signals its maturity and growing influence in global finance, with both new and established players benefiting from the transformation.

Atlanta Fed GDPNow

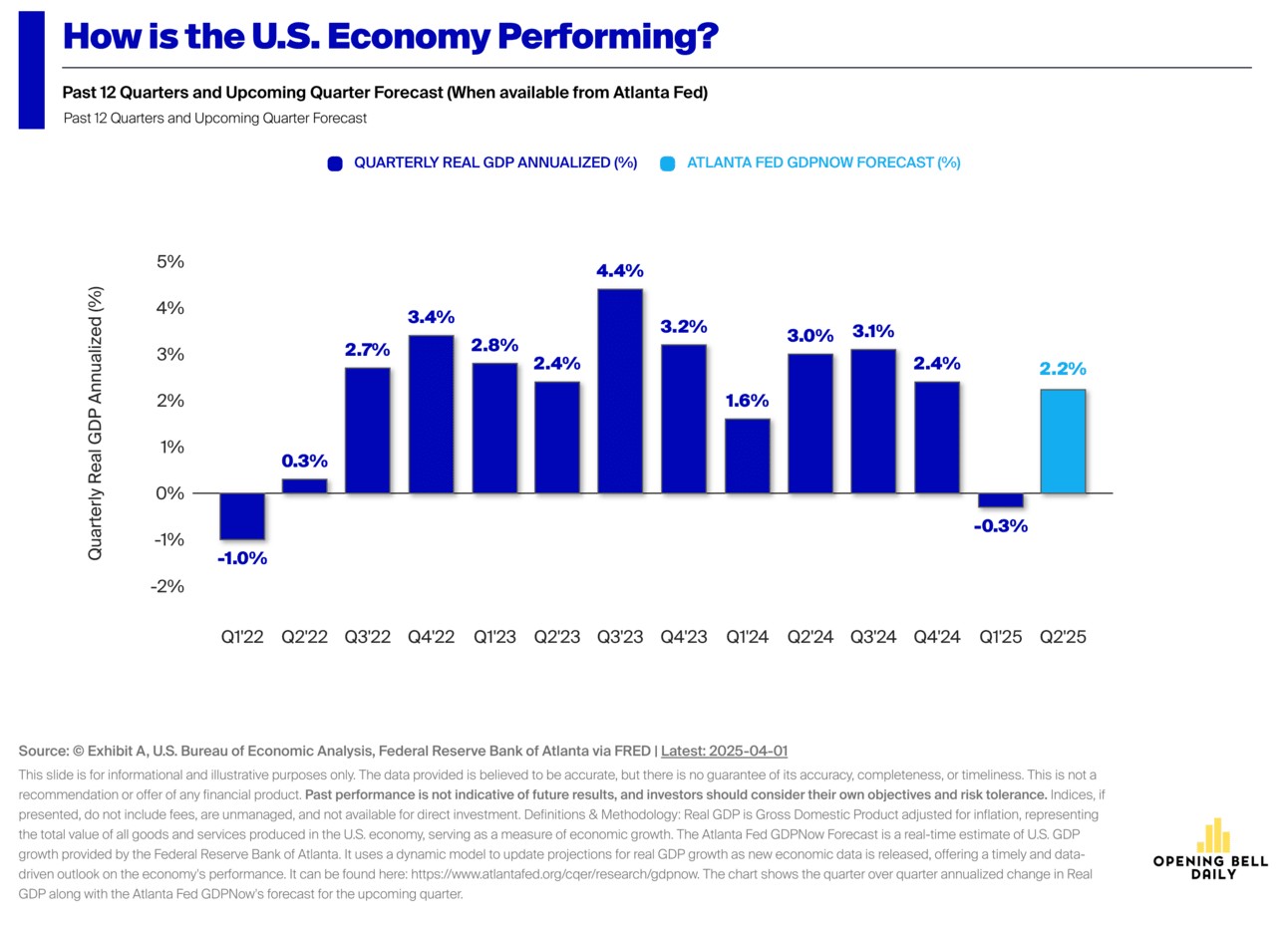

The Atlanta Fed updated its economic growth projection where it estimated a -2.5% contraction for the first quarter of 2025 which was its first negative projection in years. This was in sharp contrast to other estimates which were positive. GDP came in at -0.3%. While this created some concern about a recession, the Atlanta Fed now estimates 2.2% for Q2 2025.

The discrepancy between Atlanta Fed GDPNow estimates for Q1 2025 and official GDP growth estimates reflected differences in forecasting methodologies and data interpretations.

GDPNow is a real-time estimate of economic growth that updates often as new data comes in. It looks at 13 parts of the economy, like consumer spending and trade, using methods similar to the official government numbers. However, it doesn’t adjust for unusual, one-time events like severe weather or sudden tariff changes.

The GDPNow estimate for the first quarter of 2025 was heavily influenced by a sudden jump in imports, especially gold. These gold imports are mostly for investment and don’t mean that US production is weak. But because the model counts all imports as a negative for GDP, it makes the economy look worse than it really is.

GDPNow also doesn’t adjust for one-time shocks or unusual events. It simply projects trends forward, while human analysts might ignore these temporary factors. Many private sector forecasts are also more positive, expecting consumer spending and industrial production to bounce back.GDPNow is a helpful real-time tool, but its numbers can swing sharply due to volatile data and don’t always tell the full story.