by Dr. Chris Kacher

Bubble, toil, trouble, and all the rest

Despite bubble fears with the S&P 500 near record highs, historical patterns and current macro conditions point to a favorable setup for stocks in 2026. Over the last 4 decades, when the Fed has cut rates with the S&P within 2% of all‑time highs, or has cut without a recession, the index has been higher 12 months later 100% of the time in past episodes, with average gains of roughly 14% and 18%, respectively.

On top of that, we have additional bullish “tailwinds” from:

=Accelerating AI trade

=Robust earnings

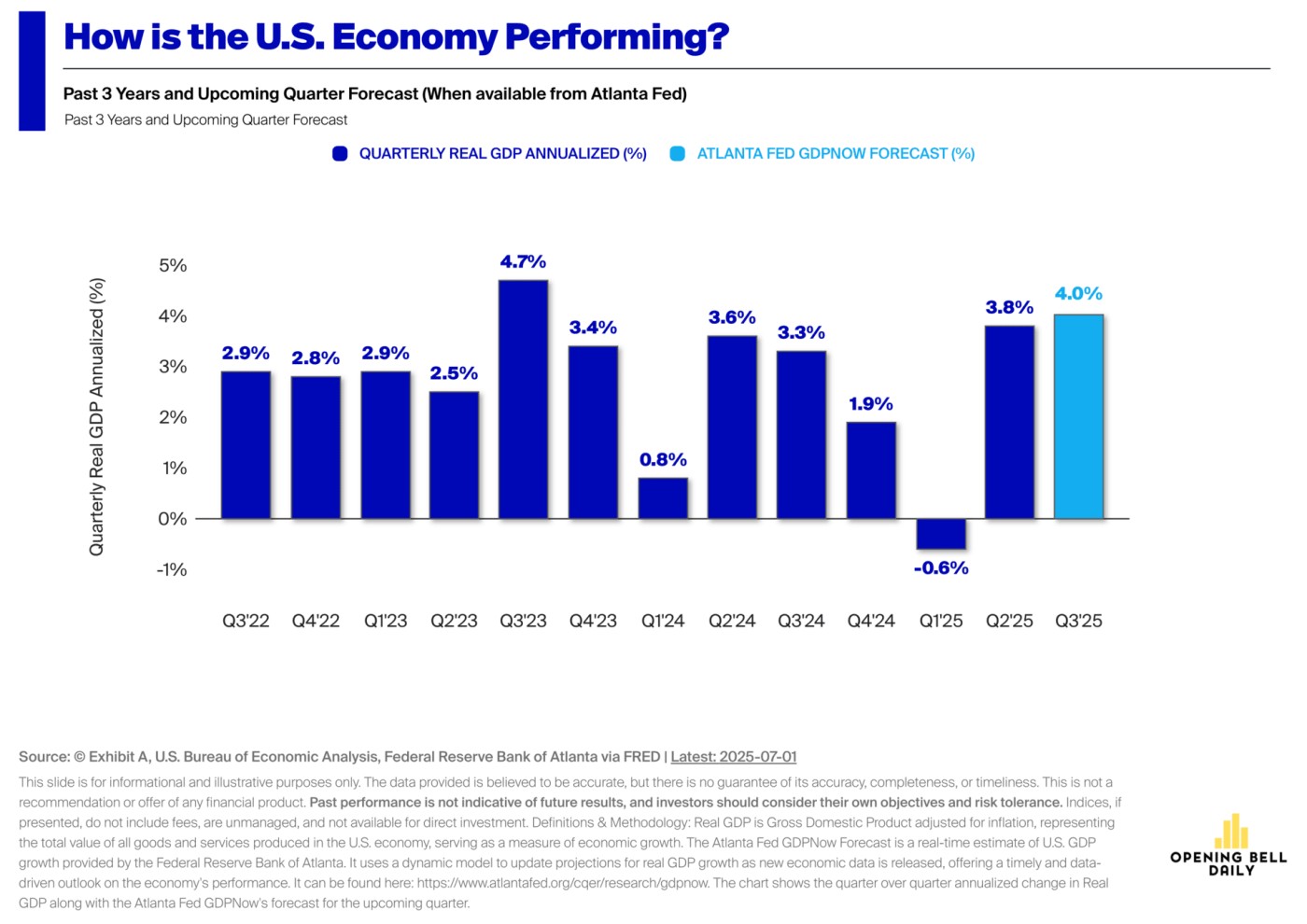

=Rising growth expectations where GDP came in at 4% in Q3'25

=Fiscal stimulus from the Big Beautiful Bill

But there are caveats. Volume on the NASDAQ Composite has been tapering on this bounce. Whether this turns out into a dead cat bounce or a sustainable rally depend on Powell's testimony on December 10. The Fed chair could remain hawkish in his testimony since CME FedWatch shows the next rate cut not until 4 meetings later on June 17. Japan also decides on its interest rate policy on Dec 19. A hike which seems likely could create another yen carry trade disaster as it did from July into August 2024. Japanese long bond yields continue to hit new highs ahead of the meeting.

For years, traders borrowed in yen at near‑zero rates, converted to dollars or other currencies, and bought higher‑yielding assets (U.S. stocks, bonds, BTC, tech, EM, etc.). But this works only if:

Japanese rates stay very low, and

The yen stays weak or stable.

But BOJ officials signaled they’re moving toward rate hikes and away from ultra‑easy policy; 2‑year JGB yields jumped above 1% and 10‑year yields toward ~1.8%, the highest in about 17 years. The yen strengthened and markets priced a high probability of a December hike, implying a structurally higher cost of yen funding.

As yen funding becomes more expensive and the currency rises, leveraged positions funded in yen turn toxic: traders must unwind risk assets and buy back yen to repay loans. The unwind hits anything on the other side of the trade: U.S. equities, bonds, and especially high‑beta assets like Bitcoin, which saw a sharp drop and large liquidations as Japanese yields spiked.

And dont forget the MSCI decision on whether to delist MSTR on January 15 which has been weighing on bitcoin and bitcoin-related instruments. Passive funds tracking those MSCI indexes would be forced to sell; JPMorgan estimates about $2.8B of outflows from MSCI‑linked vehicles, and up to $8–11B if other index families copy the rule.

It's bad for bitcoin because exclusion would push MSTR toward the fringes, shrinking liquidity and making it harder for some institutions to gain BTC exposure via equity. Index‑driven selling, lower share price, and higher financing costs mean MSTR would be less able to raise cheap equity/debt to accumulate additional Bitcoin.

An interesting pair

SNOW (Snowflake) provides a cloud-based data platform—the “AI Data Cloud”—that lets organizations store, manage, and analyze large volumes of data across multiple public clouds (AWS, Azure, Google Cloud).

SNOW gapped up yesterday mainly on bullish read‑through from MDB's (MongoDB’s) strong Q3 results which surged over 20%; traders began bidding SNOW in anticipation that its AI‑data‑cloud metrics could also surprise to the upside when it reported on Dec 3 after the close. Instead, it surprised to the downside due to less than stellar Q4 product revenue guidance which disappointed investors expecting stronger acceleration amid AI hype. It is an unforgiving environment where stocks are priced to near perfection.

Definition: An AI data-cloud runs on top of data‑center hardware comprised of powerful computers (GPUs, TPUs, high‑end CPUs) plus heavy‑duty networking, cooling, and power systems built specifically to run AI workloads.Keep in mind that AI has had a strongly bullish effect on numerous other groups since its impact is broad. We have mentioned such groups in the past which may either be turning off lows such as the quantum computing group or the nuclear energy group, or are continuing to rally such as precious metals. Reports highlighting certain names have been or are being sent out to members.