by Dr. Chris Kacher

Consequences of record debt

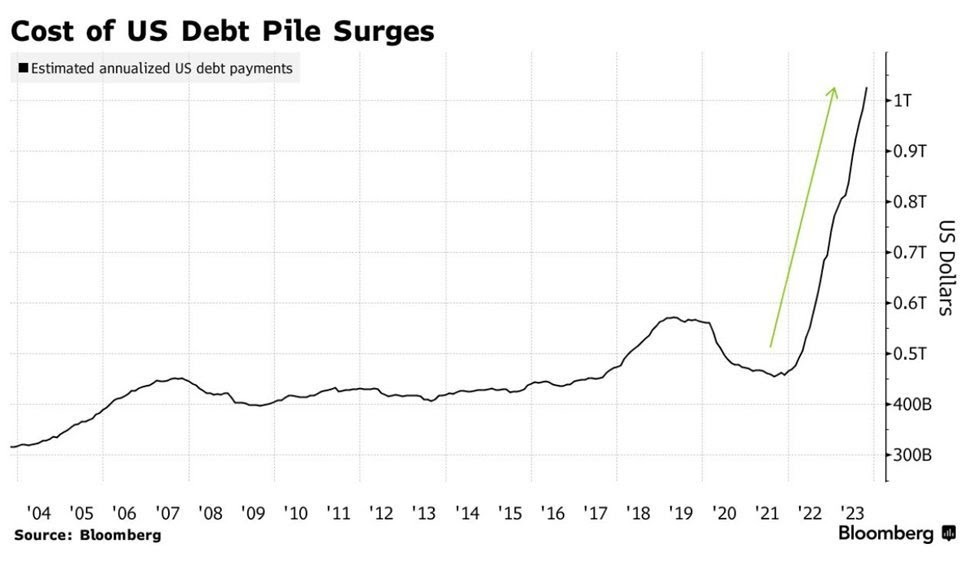

The US is officially spending more than $1 trillion on annualized interest payments to service the national debt which stands at nearly $34 trillion. That makes it the second largest budget item behind unfunded liabilities such as Social Security. More money is spent on interest payments than education or innovation.

|

Other major central banks are going to spend $2 trillion annually on net interest payments in 2023 which could balloon to more than $3 trillion by 2027. This does not account for the depreciation of fiat as more money gets printed to fund wars, deal with the consequences of global warming, and fund unfunded liabilities such as pensions and IRAs with the aging population.

|

Raising taxes, reducing spending, or digging a deeper debt hole are viciously debated. No one can come to an easy solution. If governments were corporations, they would all be bankrupt. So instead, they hunt for money via tax hikes which further suppress innovation. It seems Ray Dalio's prediction of being at the eleventh hour of the long-term debt cycle is coming true.

Stanley Druckenmiller has called for a potential lost decade looming ahead due to the failure of the government to refinance the national debt at low rates. Ray Dalio and Ken Griffin are both deeply concerned that monetization of debt is the beginning of the end of this long-term debt cycle which Dalio wrote extensively about in his book. Such would push inflation even higher across all goods and services. Studying the last several hundred years of cycles, he observed that every 75 to 125 years, a long term debt cycle plays out, ending in revolution and major wars. The last time this happened was during World War II. The US won so its dollar became the world's sovereign currency. Dalio says we are at the eleventh hour of this debt cycle. He also observed that historically, we are two years before WW I and two years before WW II. He is concerned the current situation in Ukraine and Israel will spread and escalate into global war within the next couple of years.

The US and other central banks will be forced to create fiat to fund war efforts. In consequence, fiat will devalue which will push the price of hard assets, real estate, stocks, and cryptocurrencies higher with crypto being the highest risk-on asset thus having the highest asymmetrical advantage.Bearish issues:

1) A slowdown in the economy would force the Fed to lower rates. But this may not happen until sometime mid-2024. After the recent CPI, CME FedWatch futures predict the first rate reduction will be in May 2024. If history is any guide, after such a series of sharp rate hikes in record time, should the economy begin to falter, this would force the Fed's hand to intervene with a series of rate cuts.

2) The Fed uses skewed statistics such as the CPI, PPI, and PCE to underplay the severity of inflation. The basket of goods used excludes necessities such as food and energy when it comes to core CPI and core PPI. It's great way to distort the facts. But the manipulation doesn't stop there. The Fed also removed motor vehicles when they created their Multivariate Core Trend metric. But even with all these manipulations, the PCE is still not close to their 2% target.

Tipping points that favor the bulls:

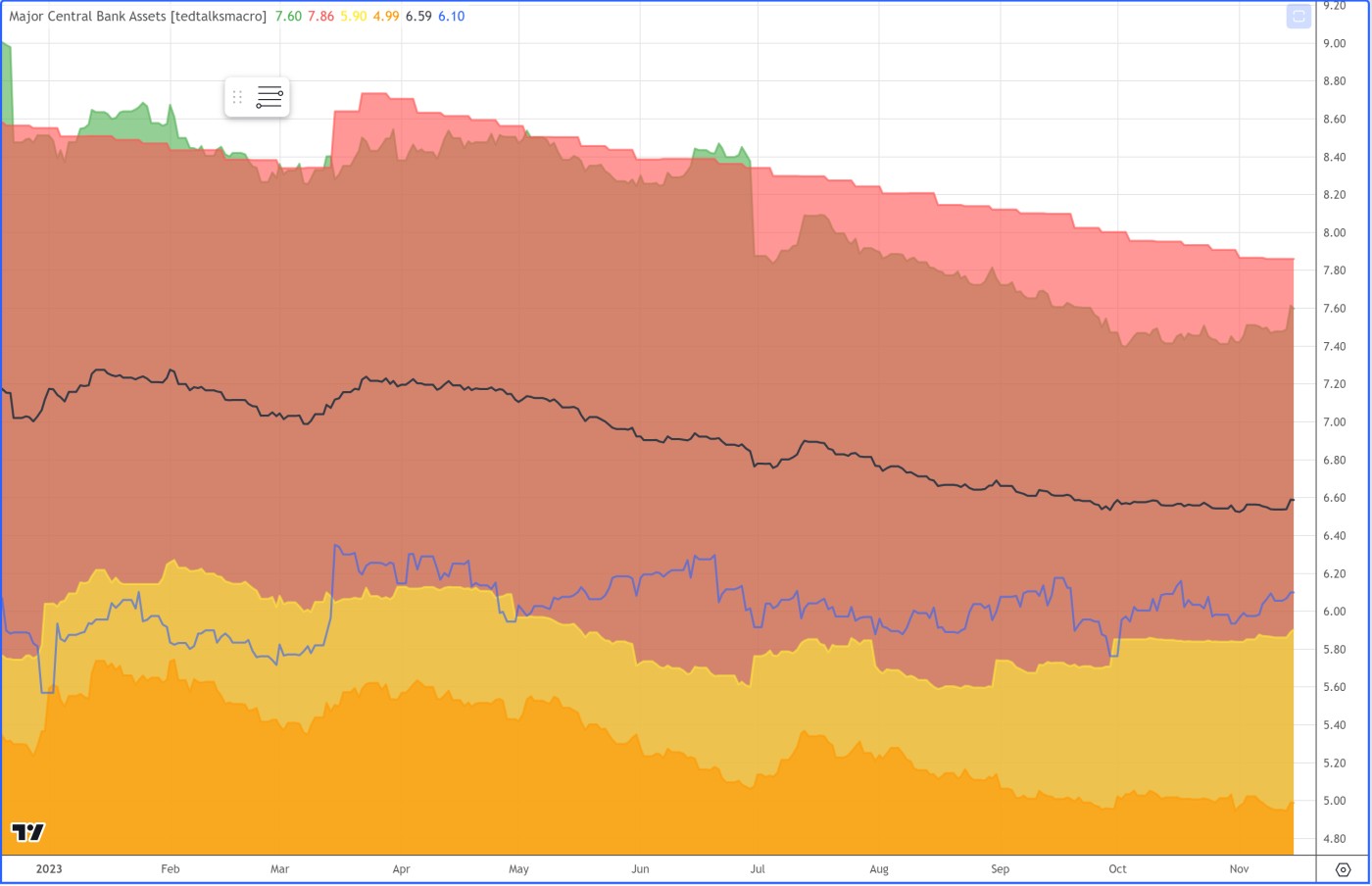

1) Liquidity may continue to trend higher then accelerate as the US is forced to print to pay debts and fund ongoing war expenses. Other major central banks will also be able to print money without weakening their currencies because of loosening monetary conditions in the US. The US Treasury yield curve had been steepening since its inversion when tight money policies ruled the day.

[The black line above represents all central banks and has been going sideways since October.]

[The black line above represents all central banks and has been going sideways since October.]2) A spot Bitcoin ETF is likely to be approved sometime in early 2024. November and December also tend to be bullish months for Bitcoin. A spot Ethereum ETF is also likely to be approved as Blackrock submitted an application.

3) Long bond yields and the dollar are less likely to trend higher in anticipation of the halt in interest rate hikes.

Shortly after the Christmas crash of Dec 24, 2018, the Fed stepped in and said they would cease tightening the balance sheet, ie, would halt rate hikes. This was the market low. Both stocks and crypto rallied in the ensuing months. The Bank of England and European Central Bank have also both signalled the end of rate hikes as well though this always remains data dependent. Since 2022, rates were hiked in record time which caused some banks to destruct due to their long bond exposure. So while the Fed tries to fight inflation, it is forced to print along the way to rescue banks, service its onerous levels of debt, and fund unfunded liabilities such as pensions and IRAs.

4) An economy that remains too strong or inflation that ticks higher could force the Fed to potentially hike rates again. An economy that starts to deeply falter would force the Fed to lower rates in a hurry. At present, we seem to be in the middle ground thus stock and crypto markets could continue to rally overall at least for now.