by Dr. Chris Kacher

AI vs global debt

While the world grew its way out of its massive debt problem after World War 2, unlike the post-WW2 era, much modern debt is consumption-oriented, not investment in productive capacity. Debt spent on entitlements, social programs, and non-productive purposes does not increase future income sufficiently to “grow out” of the problem. Today's population is aging and shrinking compared to post-WW2 which was young and expanding. The growth rate then was over 3% while today it is 1-2% or less. There was room to cut spending while today's world is laden with entitlements and unfunded liabilities.

Summary Table: Post-WW2 vs Today

AI can enable workers and firms to produce more with the same or even fewer resources, lifting overall GDP. Higher growth means government debt and deficit ratios look smaller relative to a faster-expanding economy, making large public debts more sustainable.

Even “modest” annual productivity gains (1–1.5% per year) from broad AI adoption could significantly soften the debt/GDP ratio over a decade.

AI-driven cost reductions in goods and services can help contain inflation.

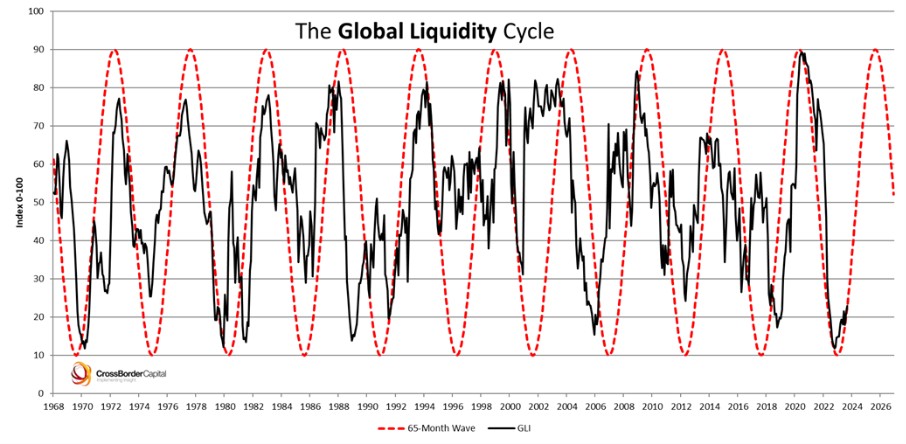

This time can be different due to the vast amounts of QE circulating in the ecosystem. It keeps markets humming and prevents recession. Global liquidity highly correlates on a quarterly or even monthly basis with stocks and Bitcoin.

Global Liquidity takes an international perspective, considering liquidity created by multiple monetary authorities, including central banks outside the US like China's PBoC. It also accounts for private sector credit provision through various channels, such as banks, repo markets, and shadow banks. Importantly, it embraces the concept of the "collateral multiplier," acknowledging that liquidity can be created outside traditional banks and is fungible. Whereas global M2 money supply of the world's four major central banks (the United States, Europe, Japan, and China) is limited thus not nearly as good a predictor of major trends in Bitcoin or tech-focused ETFs such as QQQ, TQQQ, and TECL.

Further, we have AI helping to boost productivity. As CEO Brian Armstrong recently wrote:

“Approximately 40% of daily code written at Coinbase is AI-generated. I want to get it to greater than 50% by October. Obviously it needs to be reviewed and understood, and not all areas of the business can use AI-generated code. But we should be using it responsibly as much as we possibly can.”

In consequence, productivity is spiking upwards, while employment is falling. Meanwhile, the number of junior roles are declining by a larger number than the number of senior roles are increasing which is contributing to the higher rate of unemployment. Alex Cheema shows junior roles are down 23%. Senior roles are up 14%.

|

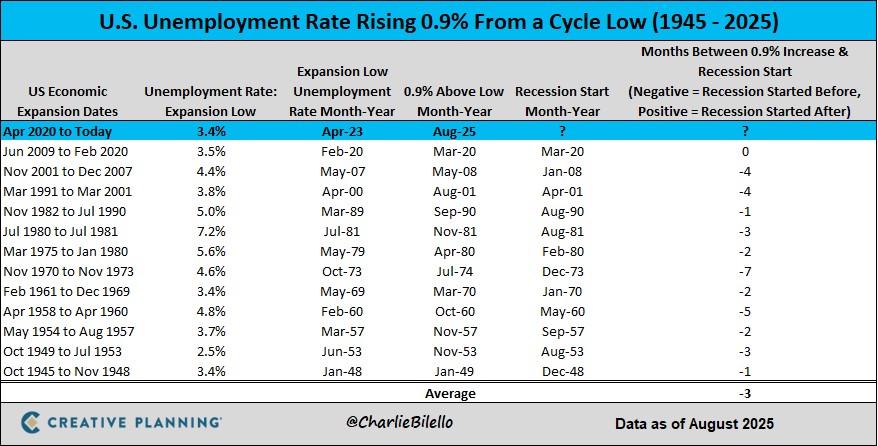

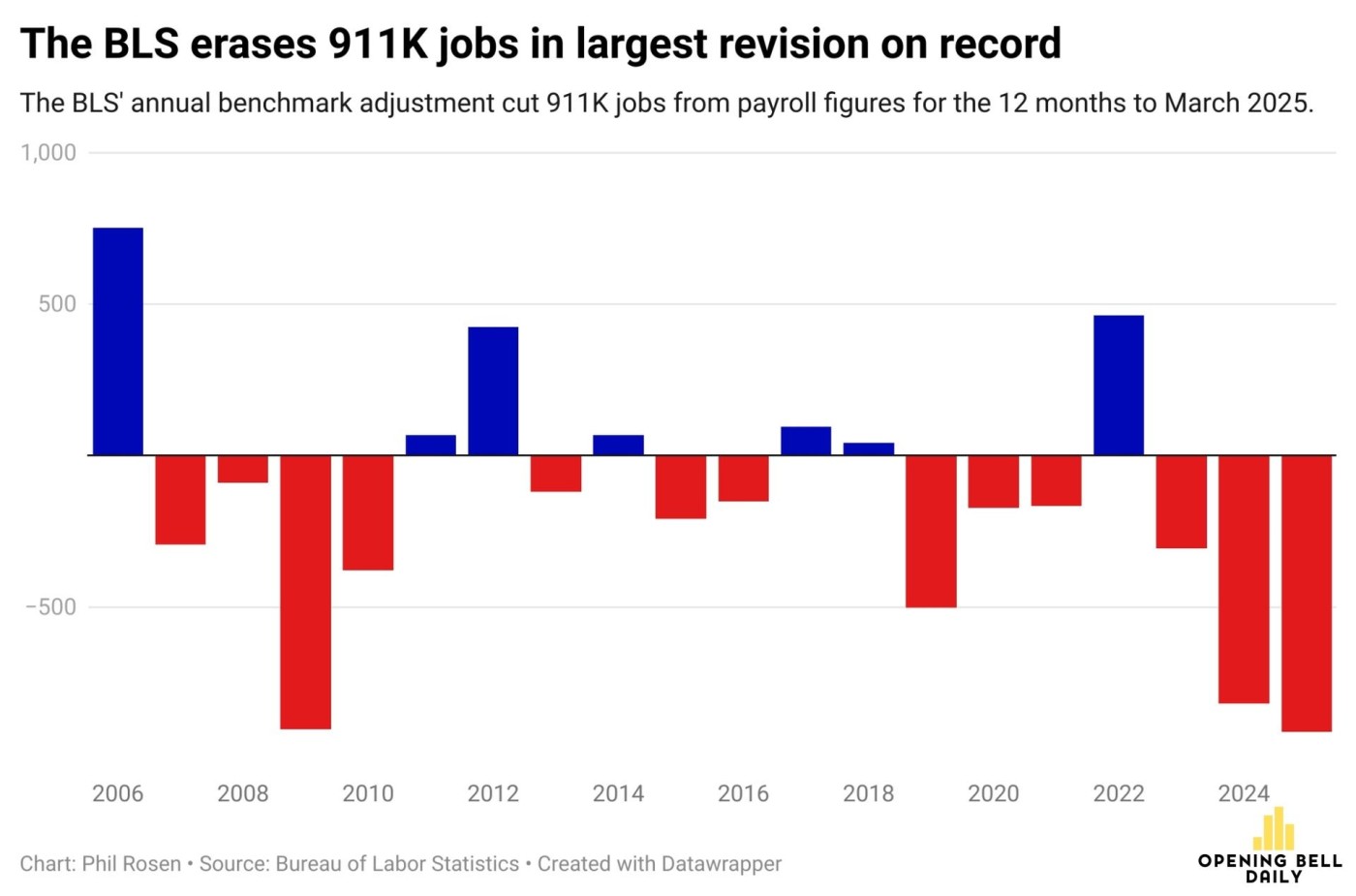

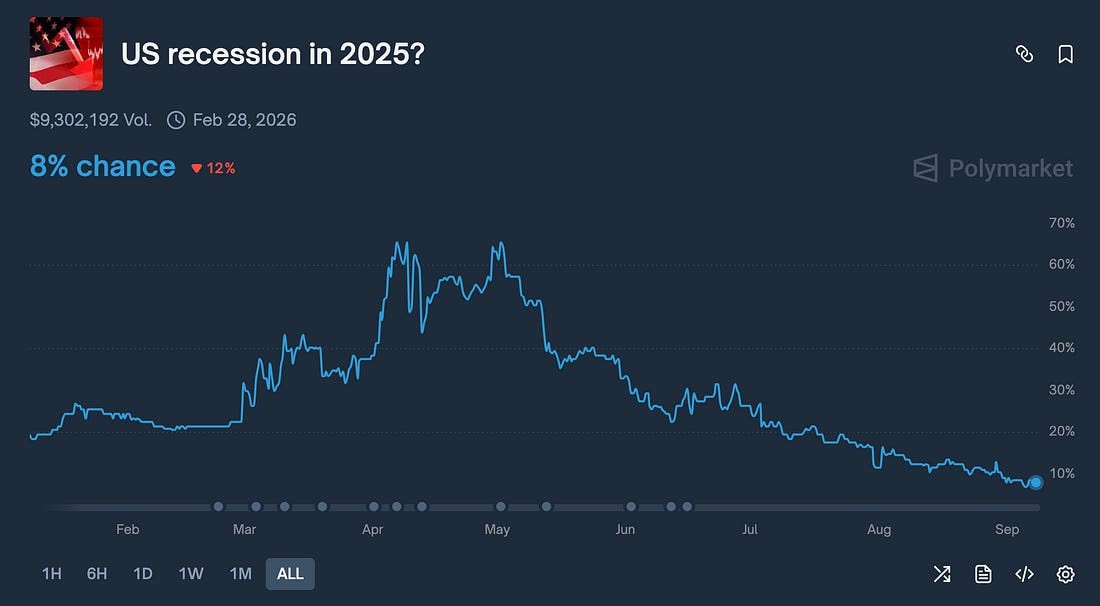

So while the bears keep predicting a recession especially given the largest revision in jobs numbers of nearly 1 million jobs

the odds on Polymarket have fallen from 65% in May to only 8% today as business fundamentals remain strong as companies become more efficient.

|

As for the record levels of debt, there is a way out if the US implements at least some of Dalio's suggestions, or if AI can drive growth beyond expectations which would overcome wanton spending which devalues fiat, otherwise, the can just keeps getting kicked further down the road to nowhere.

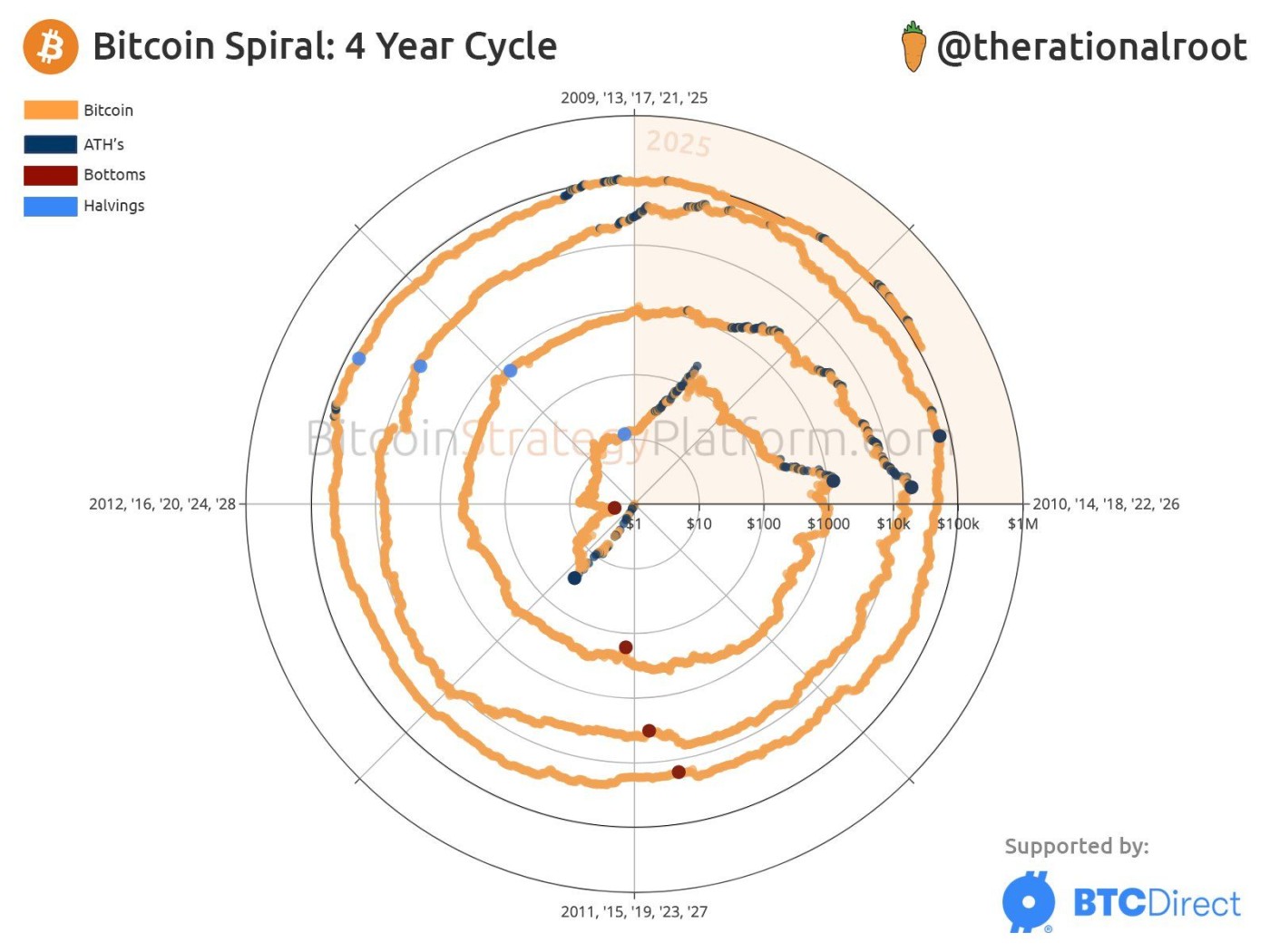

Bitcoin's cycles in one chartHalvings. Bottoms. ATHs. History may not repeat, but it sure rhymes in circular fashion.