Market Lab Report

by Dr. Chris Kacher

The Web3 Evolution Will Not Be Centralized™

Bitcoin as a substitute for fiat

Bitcoin has been criticized for not being a medium of exchange. But just as one wouldn't chip off a piece of a van Gogh painting to pay for dinner, we shouldn't expect to use Bitcoin in the same way for everyday purchases. Many vendors have been slow to accept crypto as payment because many banks still prohibit such transactions. The banking juggernaut Transferwise now known as Wise bans accounts if caught transacting in any cryptocurrency.

Homeowners or collectors often leverage their assets for liquidity by taking out loans against them. Bitcoin has been borrowed against on many platforms that enable such borrowing. Some have even used it to secure mortgages.

Of course, its real "killer app" is its store of value as its price against fiat continues to hit new highs since it was created in Jan-2009 as an antidote to wanton central bank money printing which degrades fiat appreciably over time. With recent black swans, more fiat has been created since COVID than in the last century. The first wave inflation hit which further separated the haves with assets which rose in value vs. the have-nots who lack assets such as real estate, stocks, and collectibles.

Corporate Bitcoin

Companies are starting to add bitcoin to their balance sheets. Semler Scientific announced that it has purchased 581 bitcoins for an aggregate amount of $40 million. According to the Chairman of the company:

“Our bitcoin treasury strategy and purchase of bitcoin underscore our belief that bitcoin is a reliable store of value and a compelling investment. Bitcoin is now a major asset class with more than $1 trillion of market value. We believe it has unique characteristics as a scarce and finite asset that can serve as a reasonable inflation hedge and safe haven amid global instability. We also believe its digital, architectural resilience makes it preferable to gold, which has a market value of approximately 10 times that of bitcoin. Given the gap in value between gold and bitcoin, we believe that bitcoin has the potential to generate outsize returns as it gains increasing acceptance as digital gold. Furthermore, we are energized by the growing global acceptance and 'institutionalization' of bitcoin -- reflected most recently by the Securities and Exchange Commission's January 2024 approval of 11 bitcoin exchange-traded funds. These funds have reported more than $13 billion of net inflows, with investments from nearly 1,000 institutions, including global banks, pensions, endowments and registered investment advisors. It is estimated that more than 10% of all bitcoins are now held by institutions."

Other companies are doing similar. This trend should continue as Bitcoin is slowly turning from a high-risk asset into a risk-reduction tool for the suits.

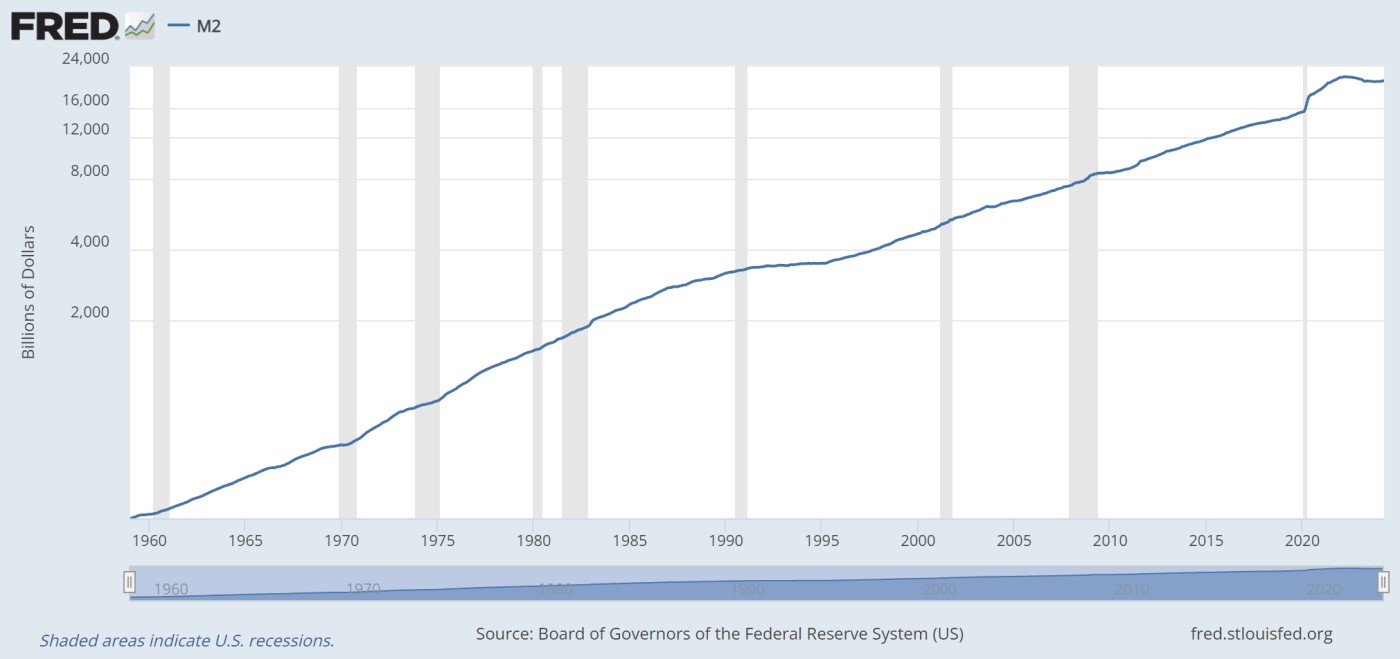

QE accelerates M2

The majors continue to grind their way higher on a string. Price/volume action has been poor as the market has never been led by so few names. Markets have never been so bifurcated. Look under the hood at various groups such as the financials and not all is well. But stealth QE has been the driving force that keeps the bull alive. This has been the theme all year.

M2 has been suppressed since 2022 so is looking to make a comeback as it always has in the past. This means any newly created money above and beyond stealth QE will flow into leading stocks pushing the majors higher so further extending this bull run. But even if M2 remains flat as it did in the first half of the 1990s, markets still behaved bullishly though took a pause in 1994 due to aggressive rate hikes after which the Fed kept rates elevated, but the markets nevertheless roared ahead in 1995. In 1994, rates were hiked six times sending markets lower, but then in 1995 after the seventh rate hike in Feb-1995, M2 started to rise. Rates were then cut twice in Jul and Dec-1995, cut once more in Jan-1996, then stayed elevated for years. Markets thrived in this environment but this was due to the increase in M2 at the start of 1995 as well as the anticipation of a rate cut which markets got in Jul-1995.

But in today's market, debt is far more problematic which necessitates stealth QE. Taxes only cover so much even though the IRS is armed to the teeth so the Fed must make up the balance. Other rising costs including uneconomic global warming policies, funding the war effort, and unfunded liabilities such as pensions and IRAs, among other issues.

But is recession in the cards? The latest US GDP data is due Thursday, and Wall Street expects the government to revise its first-quarter growth figure to 1.2%, down from the prior estimate of 1.6%. But lower economic growth keeps inflation in check spurring the possibility of lower interest rates. Underscoring this are the soft labor market reports showed declining job openings and hiring numbers. But due to stealth QE, markets dont have to have a major correction just yet. The theme of the past year is markets that grind higher without the requirement of confirmation days, three steps forward and two steps back. Plus, earnings have come in strong with first-quarter EPS beating consensus forecasts by 3% and rising 7% compared to a year ago. Further, analysts across the board have raised their outlooks for the remainder of the year.

By way of adept maneuverings via the manipulation of data and QE in all its forms, the can continues to get kicked down the seemingly endless road. But for how much longer?