by Dr. Chris Kacher

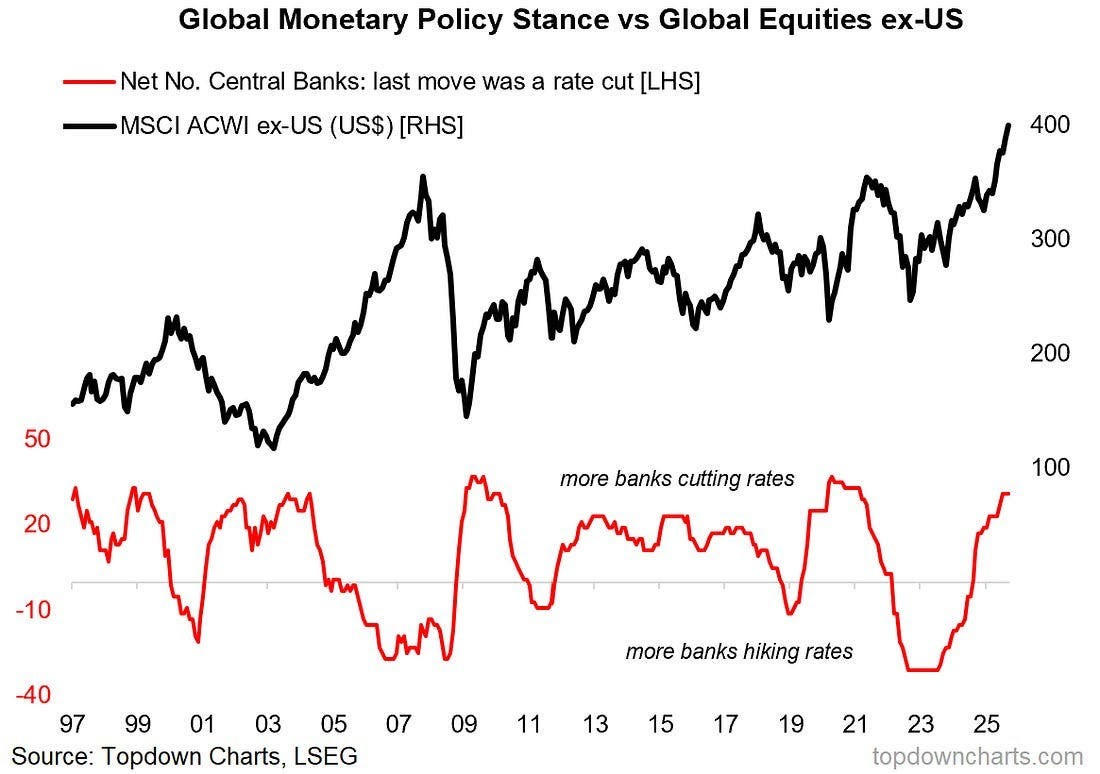

This chart nicely illustrates how central banks normally cut rates when markets make lows. But in this brave new world where stealth QE in all its forms spurs global liquidity to pay for record levels of debt, pensions, and global boomer debts, global central banks now ease when markets are at new highs. Another reason this time is different.

Meanwhile, total assets in money market funds have hit a record $7.7 trillion, tripling over the last 8 years.

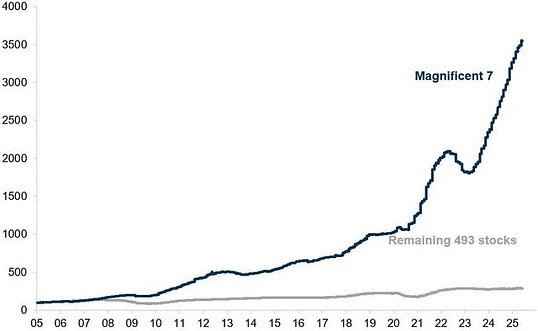

The top 10 stocks now make up 41% of the S&P 500, AN ALL-TIME HIGH. The Magnificent 7’s share has also hit a new record of 35%. Out of 500 stocks, just 10 are driving the entire index. Monetary expansion into these trillion dollar companies is part of the explanation where fund managers have to keep up with their bogies, but the deeper explanation is that the Internet/AI economy is overtaking the legacy economy.

Some say this is similar to the dot-com bust of 2000, but valuations can go to extremes before bubbles burst. And this bubble may have a ways to go as these mega cap companies are driving record profits and revenue growth year-over-year, spurred by bleeding edge tech.

Powell on inflation

Meanwhile, some still think tariffs are inflationary. By placing the tariffs on imports, there is the claim that consumers are required to pay a higher price, which would make tariffs a tax. But that has not yet happened. Federal Reserve Chairman Jerome Powell said it himself yesterday:

“We’re now collecting a good bit of revenue...$300 or 400 billion dollars a year pace [from tariffs].” “Who’s paying that? So far...it looks like it’s the middle group, retailers and importers, THEY’RE NOT passing along to consumers that much of the cost. The actual impacts on inflation have been quite modest so far. It’s a small amount.”

So Powell is saying the previous consensus on tariffs was wrong. In fact, Truflation shows that inflation has dropped from over 3% at the start of the year to only 2.05%. Keep in mind its inflation statistics are based on the rate of change in a broad basket of goods and services, weighted by consumer spending patterns, not just a few categories. Truflation’s drop from 3% to 2.05% means that the overall rate of price increases has slowed in the full basket of tracked goods and services. Sectors outside of food and energy, especially housing-related components, have experienced flat or falling prices, bringing down the “core” inflation rate, which accounts for a large share of total inflation.

|

So the Fed and Truflation are telling you tariffs didn’t bring inflation. But many don't believe it because the cost of essentials from food to energy to housing to education to healthcare continue to climb albeit at a slower pace. The discrepancy is partly due to deflationary AI and the tariffs which at least are not inflationary so far. It could also be due to doctored data which skew the results in favor of lower inflation. Either way, markets vote with their capital based on the numbers, whether doctored or not, thus the march to new highs for leading stocks and major averages.

Further, GDP is surging higher as the impact of AI is felt. Companies are growing faster and doing more with less employees. Efficiency is taking over the market. The government is capturing hundreds of billions of dollars in newfound tariff revenue. Interest rate reductions are another tailwind. In the words of William O'Neil, never argue with the market.

The new career path & uranium stocksIndeed, the evolutionary path of AI continues onward and upward spurring uranium stocks to new highs. Uranium ETFs such as URA continue to trend higher. We have been sending reports on some of these to members.

There has been a major paradigm shift. 4 year degrees leaving a student saddled in debt was the "safe” traditional path. It required a student to believe that industries would not get disrupted and that their learned skills would remain of use. The reality brought on by AI, hype and all, is that industries are being disrupted and skillsets need to be constantly upgraded.

Job security died when the half-life of skills dropped below the half-life of careers. Layoffs across a broad spectrum of industries including tech due to AI automation show that traditional employment is a risky proposition. As quarterly profits at companies rise with a smaller workforce, job security is at a major low and trending lower.

Today, climbing a corporate ladder carries great risk. Instead, one must be self-reliant. Founding a company has become statistically safer than climbing a corporate ladder. As an entrepreneur you may fail, but you'll fail forward with transferable skills with a larger network, on and offline.

While massive tech layoffs hit 150,000+ workers in 2023-2024, successful entrepreneurs built lasting value and optionality. The ability to code, create, and raise money is growing rapidly which will eventually create more jobs which will outnumber the number of jobs destroyed. But in the meantime, expect escalated demand for energy which is the lifeblood for AI compute. Uranium companies are benefiting greatly.Overall, $1B a day is being invested into AI, growing to >$3B per day by 2030. The leading AI-related names continue to trend higher which explains the Magnificent 7 + ORCL as it is the field that is exploding while traditional employment is shrinking. Incidentally, the Q2 real GDP number revised higher to 3.8%, which is significantly higher than the estimated 3.3% from economists.

All that said, in the shorter term, markets have not appreciated Powell's recent hawkish declaration on potentially fewer rate cuts. Markets had also gotten ahead of themselves as the S&P 500 went 107 sessions without a drop of 2% or more, the longest streak in more than a year. So weakness in leading names and major averages are no surprise as both the S&P 500 and NASDAQ Composite pull back to their respective 20-demas and bitcoin-related names such as GBTC trade under their 50-dmas.