by Dr. Chris Kacher

Demographics drive debt

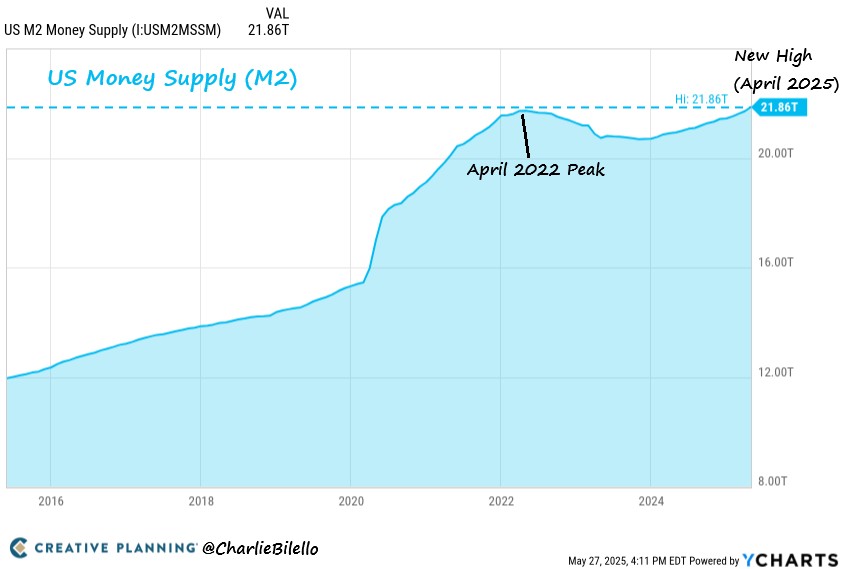

The US money supply M2 hit an all-time high in April for the first time in three years. The Fed started tightening in 2022 but only for a relatively short while. But M2 is only one measure of global liquidity. Global liquidity is more than $175 trillion because it is dominated in size by the private sector which continues to grow. Further, the trend towards lower interest rates remains intact as central banks rachet down their respective rates.

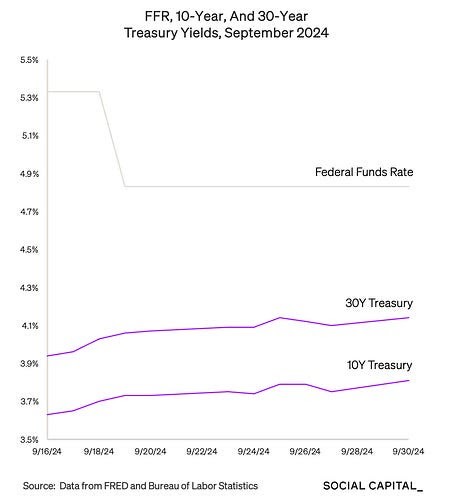

Despite lower rates, yields on the long end of the bond curve rose. This was a change from the past. As the US government continues to run large deficits even with full employment, a surge in Treasury issuance is heightening investor concerns about fiscal sustainability, while demand for government debt weakens due to the Fed shrinking its balance sheet through quantitative tightening (QT) and major foreign buyers like China and Japan reducing their Treasury purchases; this combination of increased supply and reduced demand is pushing yields higher.

Over time, due to aging demographics, governments need to borrow more money to support GDP growth to pay interest on the debt. At over 100% of GDP in debt there isn't enough economic cash flow to fund the debt growth so it gets "printed" via central bank quantitative easing (QE) and also forced, via regulation, onto the balance sheet of the banks. That debases the currency and lowers the denominator, optically making scarce assets more valuable. Bitcoin and gold, as Ray Dalio of Bridgewater has pointed out, are the better bets as they not only offset the annual 8% debasement of fiat but also gain value due to adoption effects. Dalio's main concern is that based on history, the US is headed towards a financial “heart attack” in the form of a debt crisis.

He says rightly that we need lower interest rates, less spending, and increased tax revenue to avoid this disaster. Plaque in the financial arteries of the US economy has taken years to build up, so while the warning signs are there, markets are not that worried. It’s like someone with a lot of plaque in their arteries who continues to eat a lot of fatty food thinking that since he's done it for years without a heart attack, he can continue to eat this way.

The tariffs can help raise tax revenue, Trump's administration can reduce spending, and the Fed will lower rates once they are convinced of the data which continues to show less inflation and sufficient jobs strength. If the budget deficit is lowered to about 3 percent of GDP from what Dalio and most others project to be about 7 percent of GDP, that would reduce the risks a lot. Currency and debt have to be effective storeholds of wealth or they will be devalued and abandoned.

Throughout history long term debt cycles from boom to bust have occurred in virtually every country. They go back as far as there is recorded history. This is the process that led to the breakdowns of all reserve currencies like the British Pound and the Dutch Guilder before the Pound.

But even if the US has a heart attack which still may take years to manifest which implies the US dollar would no longer be the world's reserve currency, both Bitcoin and gold should do well as they become the fear and inflation trade should such a scenario unfold.

Furthermore, demographics drive debt. As populations age, governments are forced to borrow more to sustain economic growth and cover rising debt interest, but when debt exceeds 100% of GDP, there isn’t enough real economic activity to support further borrowing. To bridge the gap, central banks create money through QE and regulations push banks to hold more government debt, which ultimately debases the currency and makes scarce assets like Bitcoin and gold appear more valuable. As Ray Dalio notes, these assets not only protect against the roughly 8% annual loss in fiat currency value but also benefit from increasing adoption, making them attractive hedges in a world where demographic trends are fueling ever-higher government debt.

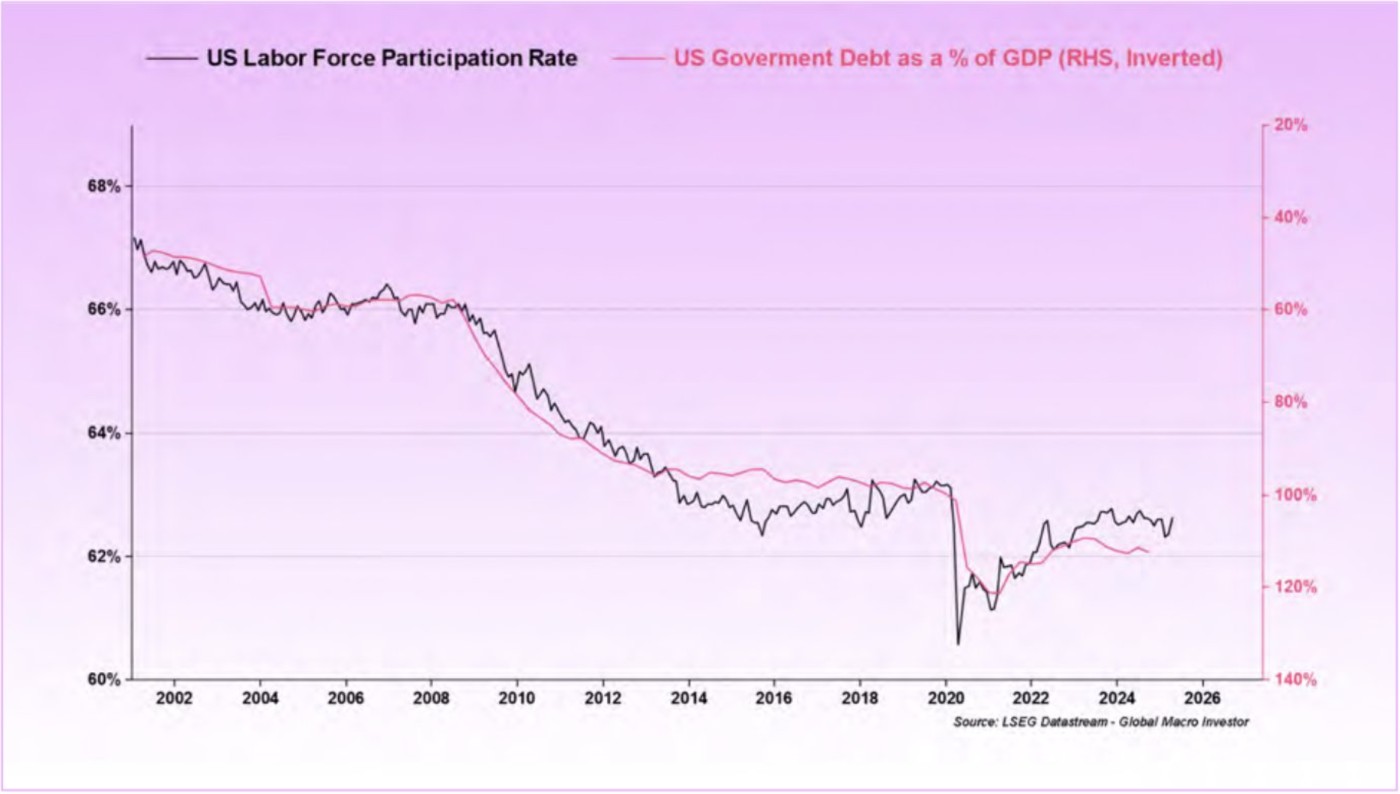

Notice how the number of working people correlate with US government debt as a % of GDP. As the number of retirees increases, the labor force participation rate falls which increases debt as a % of GDP.

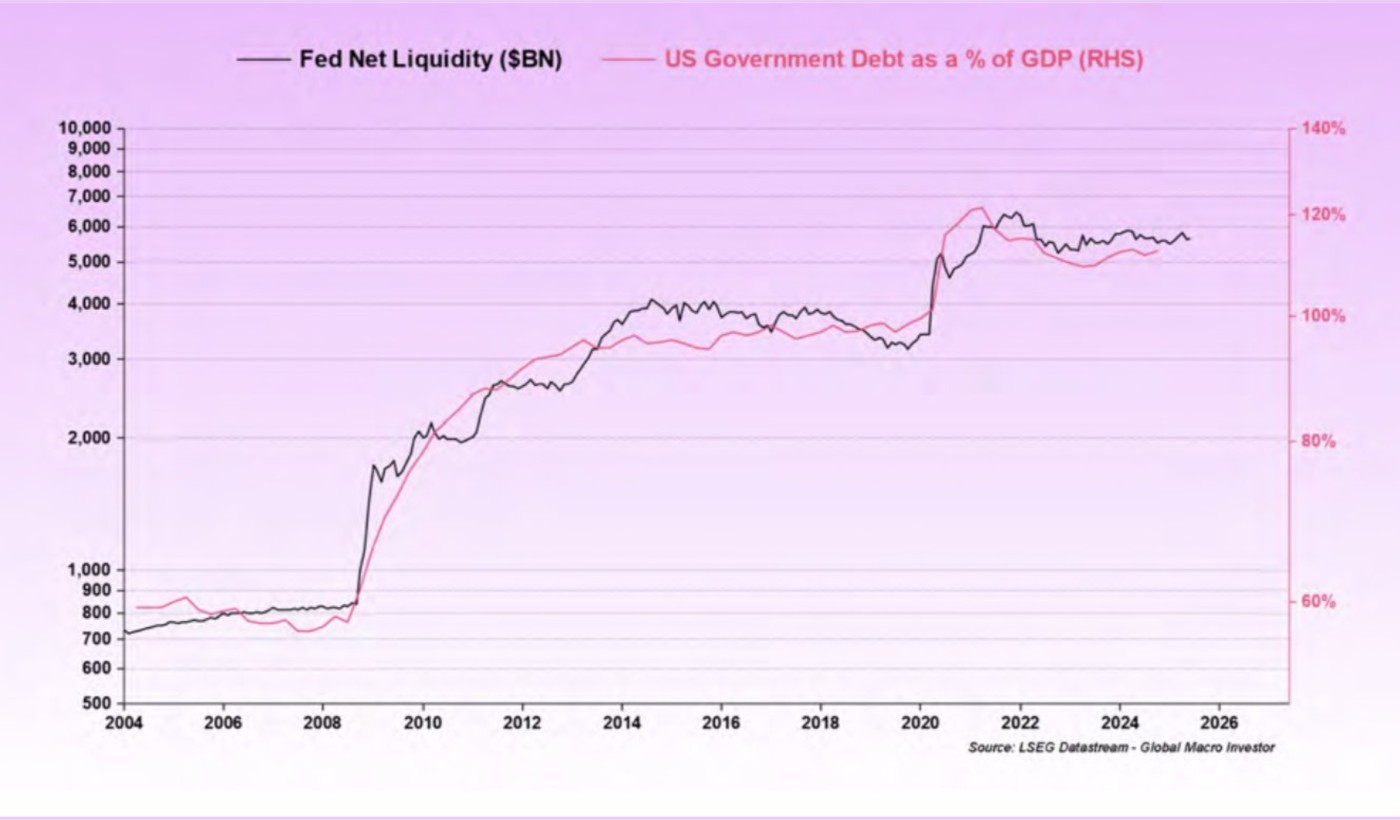

Also notice how QE correlates with US government debt as a % of GDP. As QE increases, debt as a % of GDP increases.

Also notice how QE correlates with US government debt as a % of GDP. As QE increases, debt as a % of GDP increases.

Tariffs or no tariffs, global liquidity will continue to rise. Such liquidity will experience exponential growth if we get another black swan, but in the meantime, rising bond yields can create short term corrections in markets which will spur additional levels of quantitative easing (QE).

GDP estimates shoot higher

The Atlanta Fed’s GDPNow model sharply raised its estimate for US economic growth in the second quarter of 2025, now predicting a 4.6% annualized increase in real GDP as of June 2, up from 3.8% just a few days earlier. This significant upward revision is driven by stronger-than-expected business investment and an increase in consumer spending, as reflected in recent data releases from the US Census Bureau and the Institute for Supply Management.

The model’s nowcasts for Q2 show real personal consumption expenditures growth rising from 3.3% to 4.0%, and real gross private domestic investment swinging from a negative -1.4% to a positive 0.5%. The sharp upgrade comes after a weak first quarter, when GDP contracted by 0.2% due to a large drag from net exports and softer consumption. Improved trade data, specifically, a halved trade deficit, suggest net exports will be a positive contributor in Q2, further supporting the robust forecast.

While this bullish estimate signals strong economic momentum and could ease recession concerns, some analysts remain cautious, noting the volatility in recent quarters and the potential for renewed trade tensions or policy shifts to quickly alter the outlook.