by Dr. Chris Kacher

The core CPI came in at 4.8% vs 5.1% estimates, the lowest since August 2021. Core PPI also came in tame. Markets naturally rallied as the odds of rate hikes later this year diminishes. Earlier, PCE as “the Fed’s inflation metric” as it is considered to be less volatile than CPI also came in under expectations. The Fed prefers PCE over CPI when directing monetary policy decisions. Core PCE (PCE excluding food and energy) is carefully watched.

For May PCE:

Core (YoY): 4.6% vs. 4.7% in April

Core (MoM): 0.3% vs. 0.4% in April

Headline (YoY): 3.8% vs. 4.3% in April

Headline (YoY): 0.1% vs. 0.4% in April

Core PCE now sits at the lowest growth rate since April 2021. Nevertheless, Powell said, “I wouldn’t take moving at consecutive meetings off the table at all.” Powell said current monetary policy while restrictive may not be sufficiently restrictive, or hasn’t been restrictive for long enough. So the Fed could hike more than in subsequent meetings later this year.

Initial Jobless Claims numbers which started to rise over the last few weeks dropped over the past week.

|

These stronger than expected economic points, combined with Powell’s hawkish tone at the ECB Forum, had led the market to begin pricing in higher rates to come though current inflation numbers are tempering this. Nevertheless, rates could stay elevated for a prolonged period though this of course is data dependent.

The Fed is close to pivoting away from their most aggressive tightening regime in history. CME Fed Futures show one more rate hike when they meet in July. They will keep rates elevated until a series of interest rate reductions starting Jan 2024 leading all the way down to 350-375 bps by Dec 2024.

The strong data combined with a lower than expected PCE caused a bounce in the major averages.

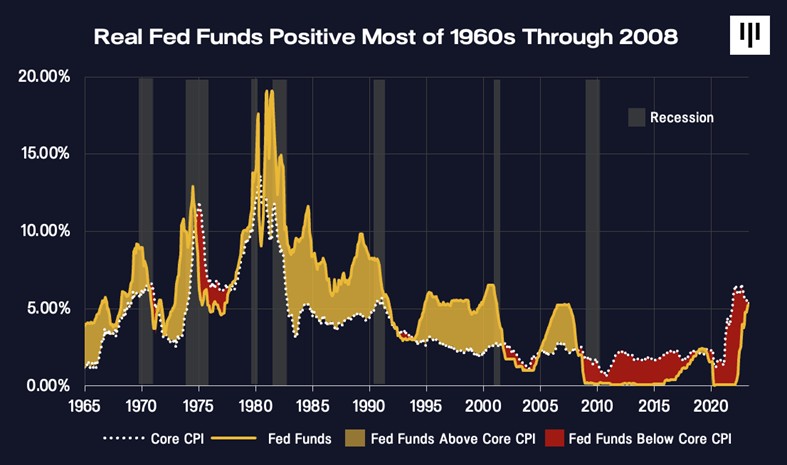

During the central banker days of the 1970s and 1980s leading up to the Great Financial Collapse of 2008, central bankers kept rates 1.8% above inflation on average. Since 2008, the era of Quantitative Easing has kept rates 1.52% below inflation, or a substantial difference of -3.32%. Thus it is no wonder inflation has been on a tear with massive incentive to borrow, buy homes, and spur speculative investing. The yellow regions mark when the fed funds were above core CPI while the red regions mark when the fed funds were below core CPI.

Rates may therefore likely have to remain higher for longer than the markets think before the Fed can tame inflation down to their target 2%. Thus bonds remain a higher-than-normal risky investment unless we get another black swan which forces rates back down in a hurry.

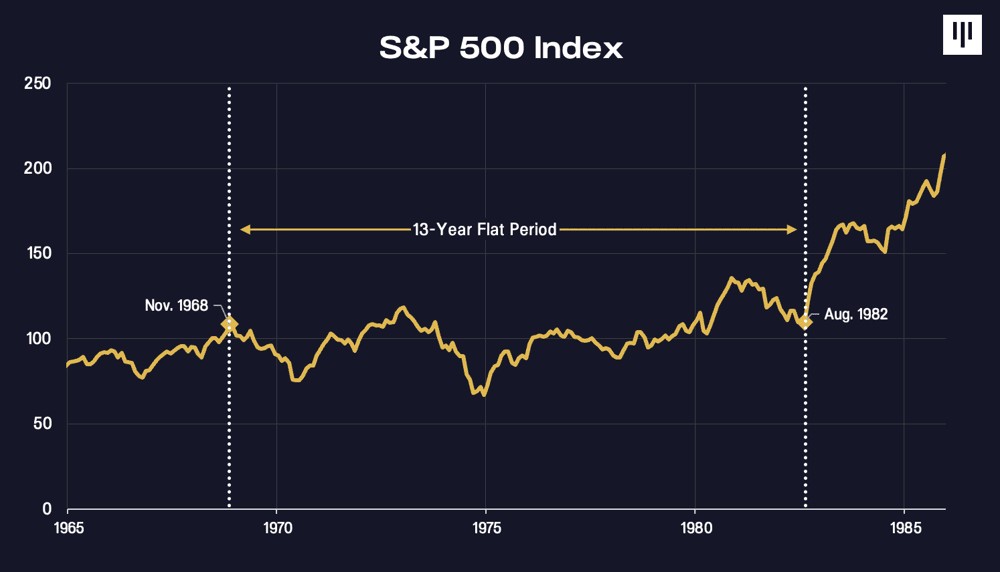

Rising rate environments such as we saw in the 1970s make for challenging markets as it decimates value in interest-rate sensitive assets classes. In consequence, the S&P 500 was overall flat with minor rallies and major bear markets for the entire 70’s. But should inflation be tamed faster than expected, along with AI-meme stocks which continue to steamroll in one of the most bifurcated market environments in history, major averages could continue to trend higher. Further, precious metals could continue to move higher as we have seen with the silver stocks.

Bitcoin

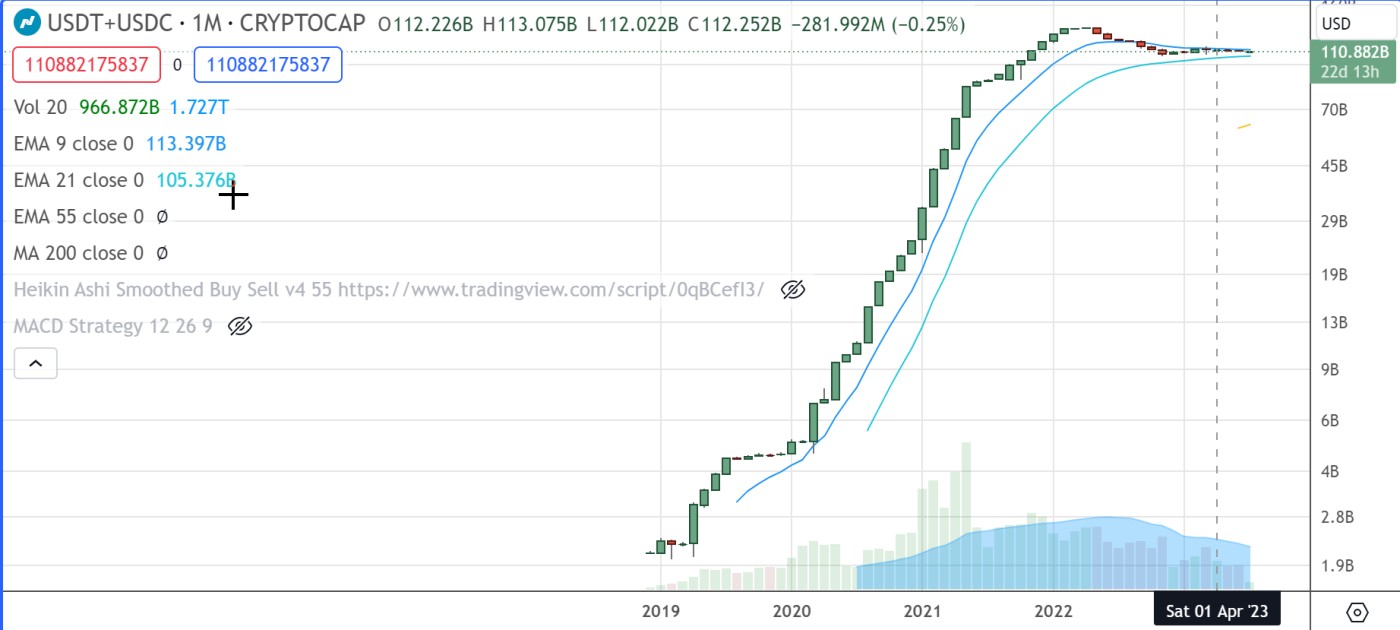

At present, Bitcoin is trying to break through the 31-32K resistance due to the positive news that declared XRP (Ripple) not a security. But we also see USDT+USDC has been declining or flatlining compared to the prior big bull market which ran from 2020 to end of 2021.

DXY dollar index was holding strong because of expected higher rates until Wednesday's tame core CPI number was reported.

AI-meme stocks

A number of AI-meme stocks have been at odds as of late though the recent CPI and PPI numbers helped these stocks higher. MSFT and AMD have corrected down to their 50dmas while GOOGL traded below its 50dma but is bouncing. ADBE had a pocket pivot this last Monday and is well above the price on the day we sent a report on June 9.

Remain on the lookout for pocket pivots, undercut & rallies, and volume dry ups in these AI-meme names for low risk entry points. Indeed, NVDA was exhibiting a minor volume dry up then broke higher. As legendary futures trader Ed Seykota once famously said, the trend is your friend until the end when it bends.