Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

The Evolution Will Not Be Centralized™

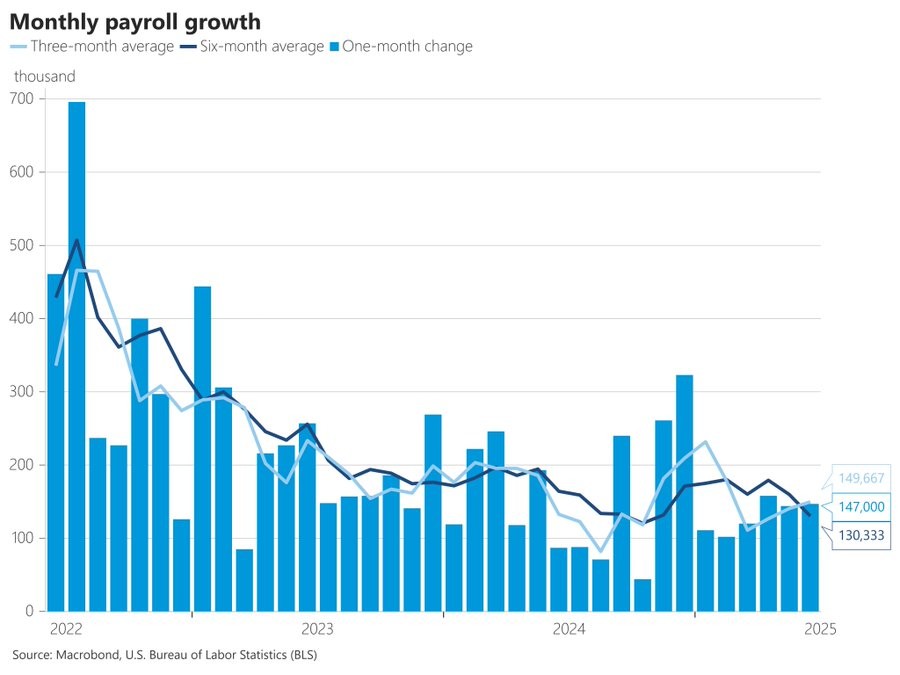

ADP payrolls showed a surprise decline of 33,000 private-sector jobs in June, a wide miss from the 98,000 gain economists forecasted, and was the second negative print since 2020. Meanwhile, job openings jumped to 7.8 million in May, and continuing claims just hit their highest level since 2021. The mix of fewer hires, more openings, and rising unemployment claims set the stage for a poor jobs report.

Yet the jobs report came in strong as it remains a slow-to-hire, slow-to-fire labor market. Employers added 147,000 jobs in June, above the 115,000 forecast. Unemployment was expected to rise by 0.1% to 4.3% but ticked down to 4.1%.

With moderating inflation, a decent jobs market, strong earnings, and rising global liquidity, the general uptrend in stock market averages and in Bitcoin should continue.

Dollar comeback?

The dollar is at an inflection point.

: Rate cuts are typically seen as bearish for the dollar, as lower yields reduce its attractiveness.

: In periods of global stress or disinflation, rate cuts can trigger a rush into U.S. Treasuries and dollars for safety and collateral needs, especially if global liquidity is tight.

: Many emerging markets have sought alternatives to the dollar (local currencies, gold, bilateral pacts), but global trade, finance, and debt remain heavily dollarized.

: Many corporations and sovereigns in non-U.S. economies still have substantial dollar-denominated debts. In a global risk-off or liquidity squeeze, demand for dollars can spike as these entities scramble to cover obligations.

The technical setup (DXY at channel support), the risk of a violent reversal, and the mechanics of dollar demand during risk-off events are well-supported by history and current market structure. The vulnerability of dedollarizing countries with USD liabilities is real. The idea that rate cuts can trigger a dollar surge in certain environments is supported by recent and historical events.

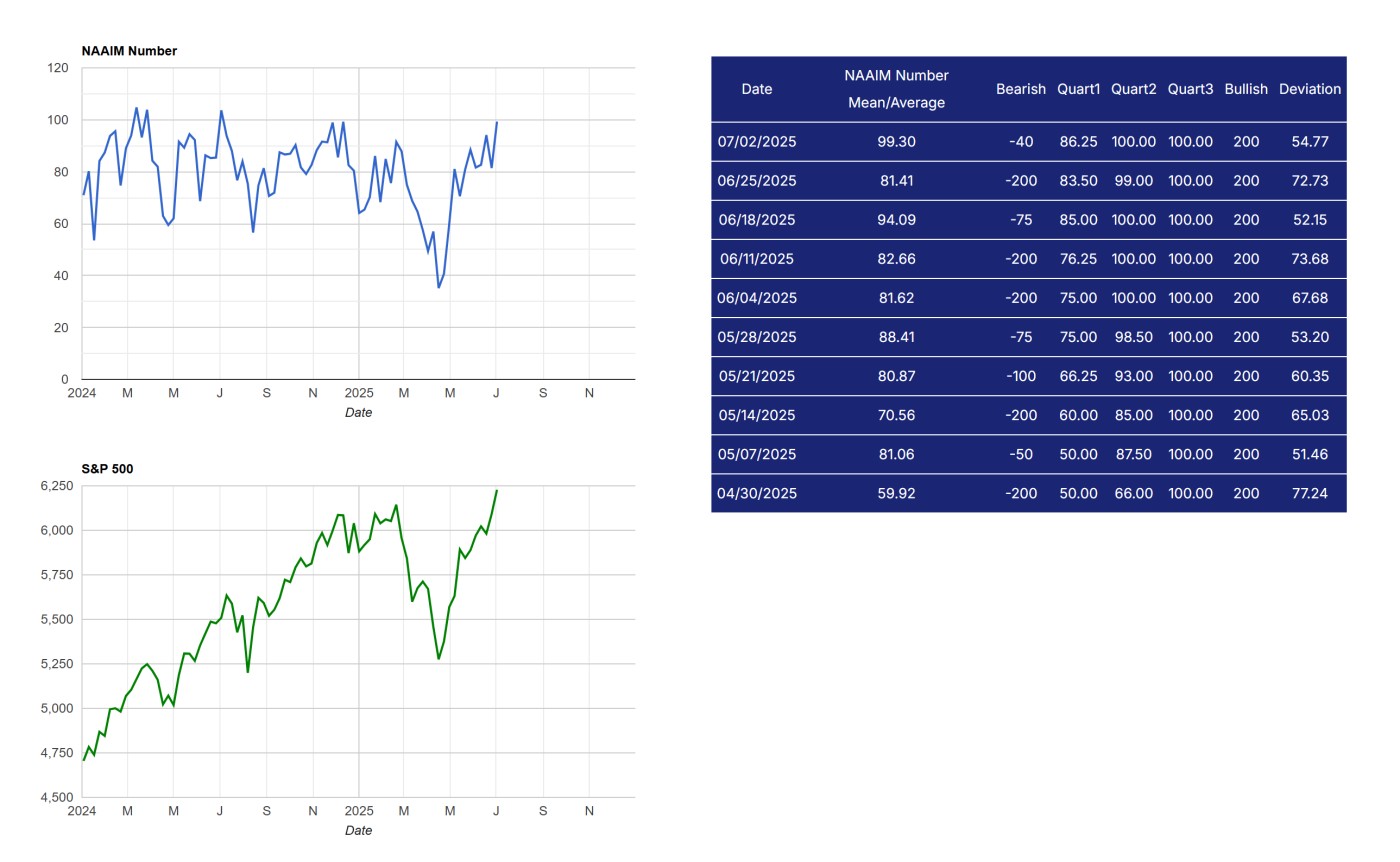

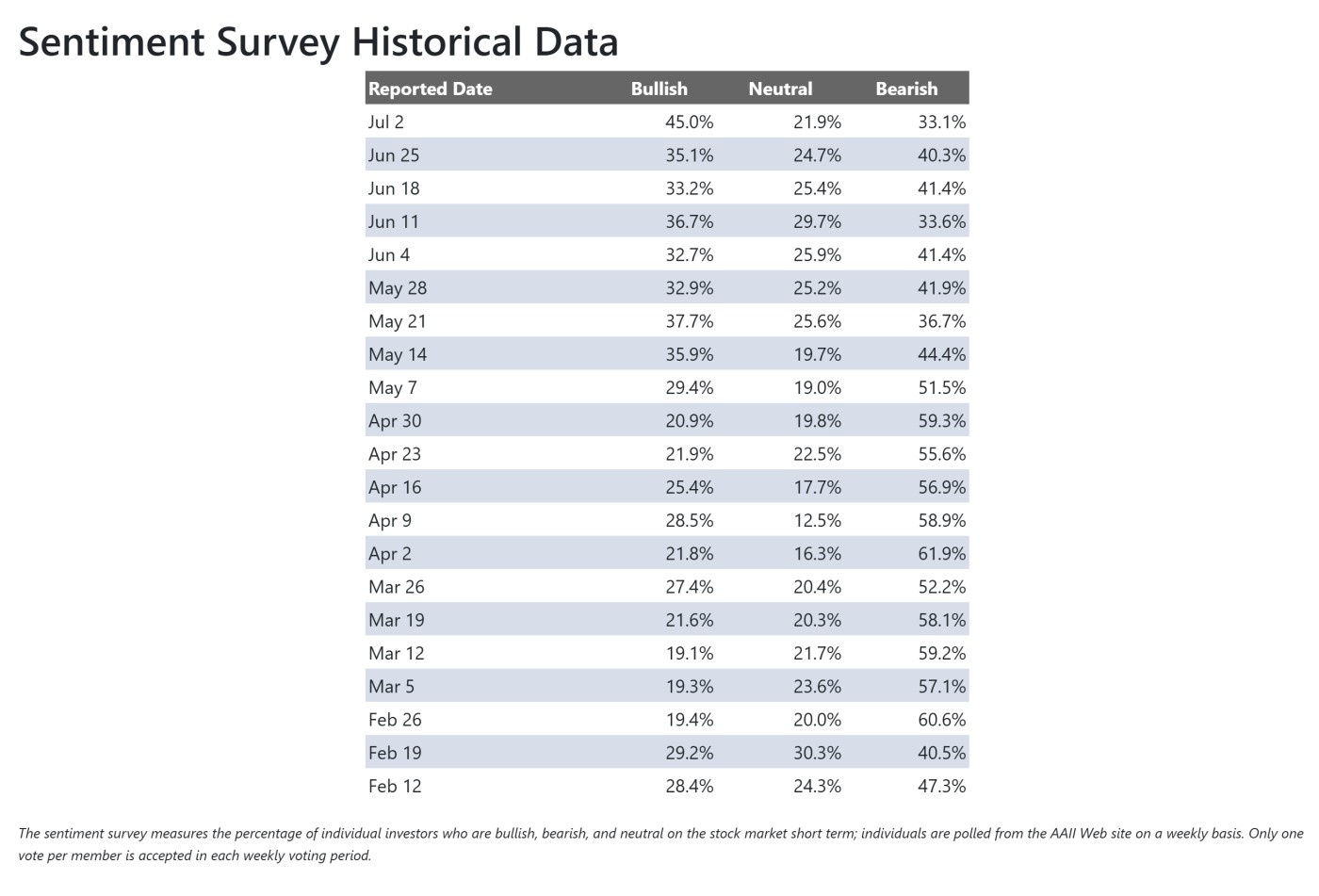

Minor top in market?

When sentiment numbers peak, markets often pull back. NAAIM and the AAII sentiment survey are hitting highs of sorts. With NAAIM:

Peaked March 13, 2024 --- S&P 500 peaked two weeks later on March 27, 2024

Peaked July 3, 2024 --- S&P 500 peaked one week later on July 10, 2024

Peaked Nov 27, 2024 --- S&P 500 peaked one week later on Dec 4, 2024

Peaked Jul 26, 2023 --- S&P 500 peaked to the day (though NAAIM > 90 for 3 weeks thus hard to catch the absolute top)

Peaked Dec 27, 2023 --- S&P 500 peaked 2 days later (though NAAIM > 90 for 2 weeks thus hard to catch the absolute top)

NAAIM may continue higher for another 1-2 weeks based on history and markets may not peak for another 1-2 weeks after that point, so it is possible markets could continue to rally for up to 4 weeks if history is any guide. In other words, it is challenging to catch the top. And sometimes, the top is very mild such as the Dec 27, 2023 top where the market fell for 4 days then continued its uptrend.