Market Lab Report

by Dr. Chris Kacher

The Web3 Evolution Will Not Be Centralized™

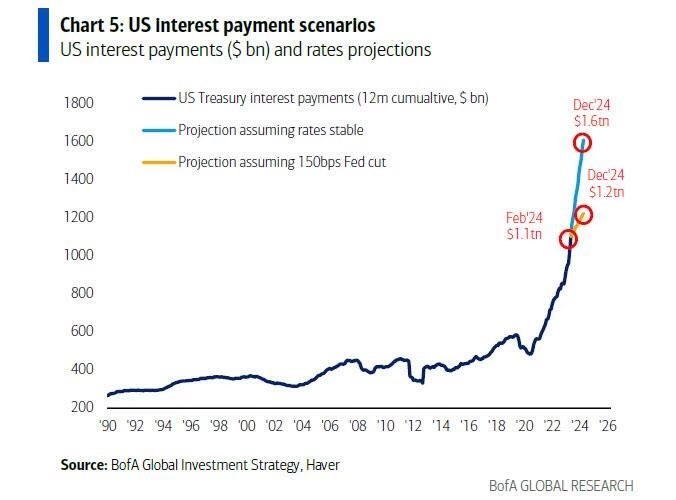

From 1990-2019, debt rose but at a regular pace. Since COVID hit, starting in Mar-2020, debt has soared. Over the last three years US Treasury interest payments have been rising 15-fold. A few years now is 105 years in the old world. If rates stay elevated, the US Treasury debt interest payments of $1.1 T in Feb-2024 will soar to $1.6 T by Dec-2024. Following April’s weaker-than-expected job growth and moderating wage gains, CME FedWatch is pricing in a second rate cut by the end of the year. This may change depending on whether inflation remains elevated. The start of the year projection of 6 rate cuts by Dec-2024 is completely off the table. Even if we did get 6 fabled rate cuts, debt interest payments would still rise to $1.2 T.

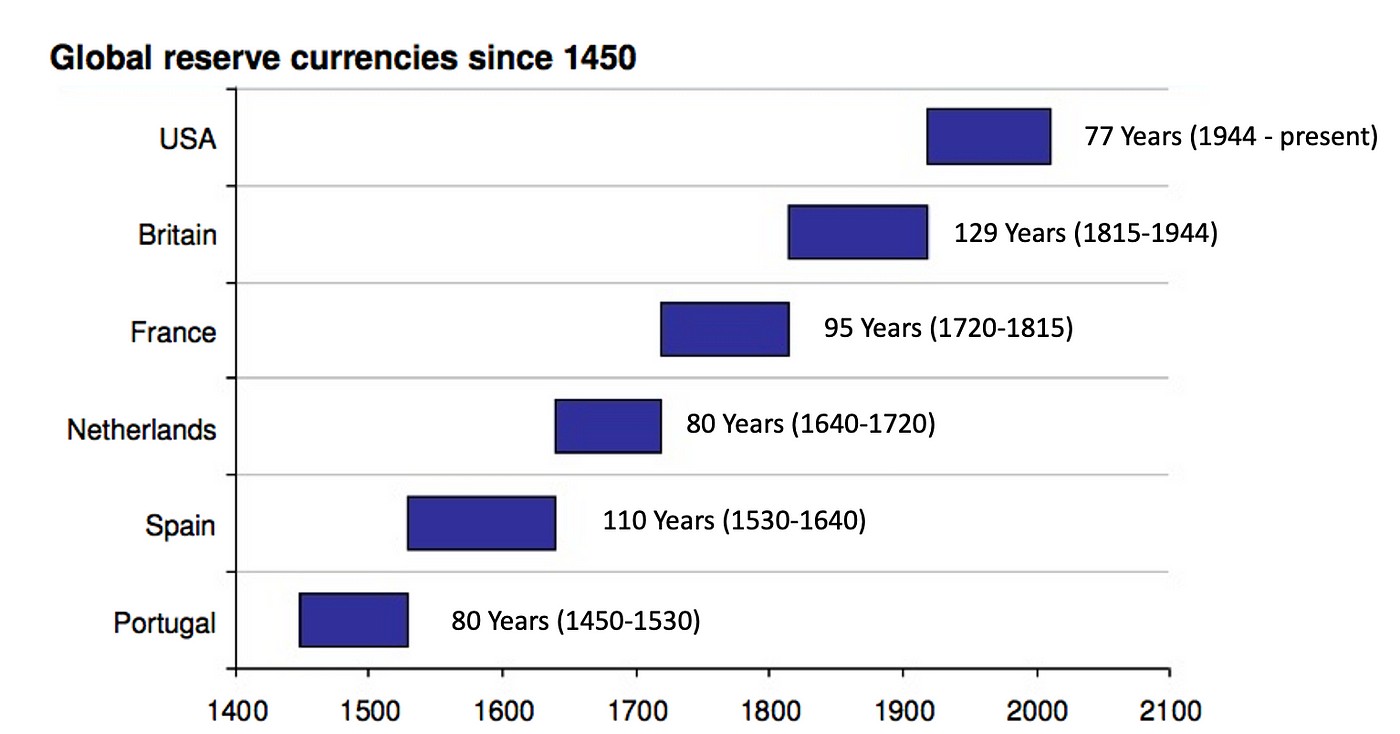

It seems the US dollar has crossed the event horizon to use the black hole analogy. This is the point at which nothing can escape a black hole's gravitational pull. In terms of sovereign fiat which is the US dollar, debt continues to pile up which increases debt interest payments in a flywheel effect. Eventually, global reserve fiat fails. This is why such currencies have a limited life span.

The US economy remains strong in part due to petrodollars which significantly bolster the US dollar's status as the world's primary reserve currency. This system, where oil transactions are predominantly conducted in US dollars, ensures global trade with the US. While contenders such as BRICS and CANZUK (Canada, Australia, New Zealand, UK) are up and comers, they are still tiny by comparison to the western nations (US, Canada, UK, EU). The US dollar therefore should have at least a decade or two left to continue as the global reserve currency.

But should World War III happen in the next couple of years as Ray Dalio has wondered, the winning country's currency would take on the mantle. The unthinkable nuclear war hopefully remains off the table as the most powerful nations know this is an end game or by far the worst setback over the last millenium. Therefore, if a conventional global war occurs, it remains to be seen whether the US, China, or some other major would emerge victorious.

More QE ahead

As for the recent testimony given by Fed chair Powell, he said they would start to taper the taper by reducing the Treasury runoff cap from $60 bil to $25 bil which was $5 bil above estimates. This is dovish thus bullish. Indeed, global liquidity jumped the most since the start of this year perhaps signalling a change of trend.

But the issue of persistent inflation remains thus the number of rate cuts had dropped to just one by the end of the year. That said, the weak jobs report pushed the number of cuts from one to two. The dollar weakened and the 10-year Treasury rallied on the news, but we are not out of the woods yet. The Bitcoin downtrend remains intact for now while major stock market averages could be choppy going forward.

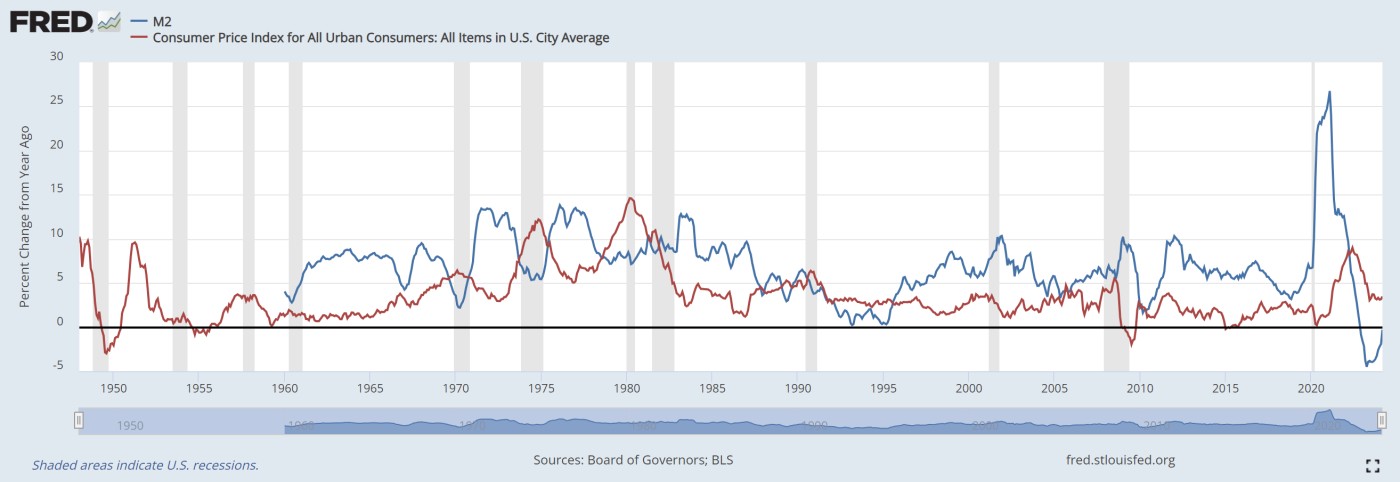

Stealth QE will increase on June 1 based on this reduction in the Treasury runoff cap. M2 % change from a year ago is about to turn positive, but until the inflation and interest rate situation improves, whether stealth QE and the tapering of the taper can push stock and crypto markets back into uptrends remains to be seen. Are we in store for chop suey markets?

1970s, 1994/95, and 2018/19 compared to today

One could try to compare Jan-2019 when the Fed said they would stop tightening the balance sheet after the Christmas crash on Dec 24, 2018 when markets hit their major lows. This coincided with the Fed making an emergency announcement that essentially they would give markets what they wanted, ie, less tightening. The formal announcement then followed on Jan 4, 2019. But inflation and interest rates were not problematic back then. The Fed had room to taper then cut rates. Today, the Fed can't just start cutting rates until inflation starts to subside further. Three hot CPI reports, a hot PCE, and a US Employment Cost Index that came in above estimates puts the Fed in a very difficult position.

Comparisons have also been made between the stagflationary 1970s and today. While inflation, growth, and unemployment in the 1970s were a lot worse than today, we have a steady flow of stealth QE to service debt interest, fund wars, deal with climate change, and fund pensions and IRAs, among other major costs. The central bank has to create $1 trillion every one hundred days. This is why our debt-to-GDP is at all-time highs and climbing. In consequence, the inflation megatrend remains intact suggesting more QE thus higher stock and crypto markets are likely over the next year. But in the shorter term, hot inflation and elevated interest rates act as headwinds. Given stealth QE in the form of $1 trillion every 100 days and climbing, it seems inflation would not drop sufficiently to accommodate the Fed's mandate of 2% inflation. Rather, inflation would likely remain persistently elevated suggesting rates also stay elevated. This fear has caused the recent correction in stocks and cryptocurrencies. Going forward, weak but not too weak economic reports such as the jobs report we got on Friday will be bullish for markets because it suggests the Fed will have to cut rates sooner than later. Granted, the actual report was weaker than reported but markets care about perception. Ultimately, if sticky inflation remains stubbornly elevated, it will be bearish for markets since the Fed will have to postpone rate cuts further.

Some bulls could try to use 1994-95 as the example where the Fed kept rates elevated but the markets roared ahead. In 1994, rates were hiked six times sending markets lower, but then in 1995 after the seventh rate hike in Feb-1995, rates were cut twice in Jul and Dec that year, cut once more in Jan-1996, then stayed elevated for years. Markets thrived in this environment but this was due to anticipation of a rate cut which markets got in Jul-1995. Inflation was not an issue back then and debt was nowhere near the levels it is today.

All that said, the tapering of the taper is a bullish event but markets remain highly data dependent on inflation and signs of strength or weakness in the economy. To add to the bulls vs bears noise, the number of times the word “recession” came up on earnings calls and investor events has dropped from 302 a year ago to 100 this quarter, a two-year low. This pushed analysts to raise earnings estimates by 0.7%.

To recap, stocks plunged, executives spoke less about a recession, and analysts turned more optimistic all while persistent inflation remains an issue. But consumers keep spending, layoffs haven’t spiked, and economic growth is still decent. In consequence, Goldman Sachs raised its second-quarter GDP estimate from 3.3% to 3.4%. But how long can the economy remain in what the market believes is a Goldilocks phase?