by Dr. Chris Kacher

DXY trending lower

The euro makes up 58% of the DXY basket so has the most inverse influence on the direction DXY. When the euro rises, DXY is likely to fall. Currencies are driven by interest rates. Rising rates attract capital so strengthen the currency.

The Fed is about done raising rates after one more 25 bps hike, but the ECB still has to hike more than this because the Fed has hiked 125 bps more than the ECB to date in this tightening cycle, plus rates of inflation in the EU are higher than in the US.

This divergence in monetary policy between the US and EU will likely contribute to a weaker DXY. The spread between short-dated yield in the EU vs. the US are pointing to a lower DXY. This can have a somewhat bullish impact on the major averages and Bitcoin. But a more hawkish Fed stance due to strong corporate earnings and sticky inflation will strengthen DXY which can push markets lower.

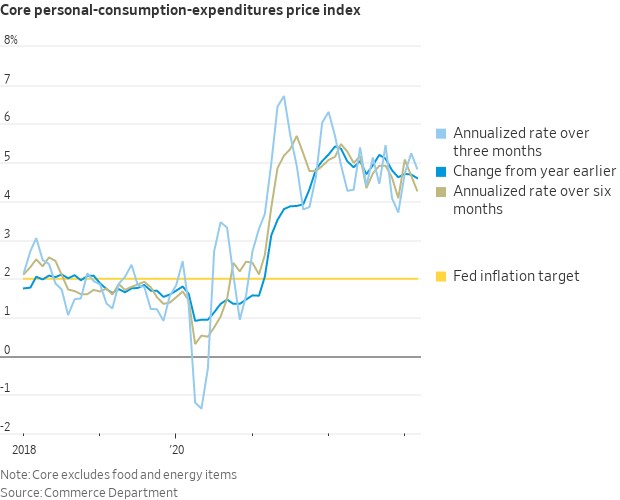

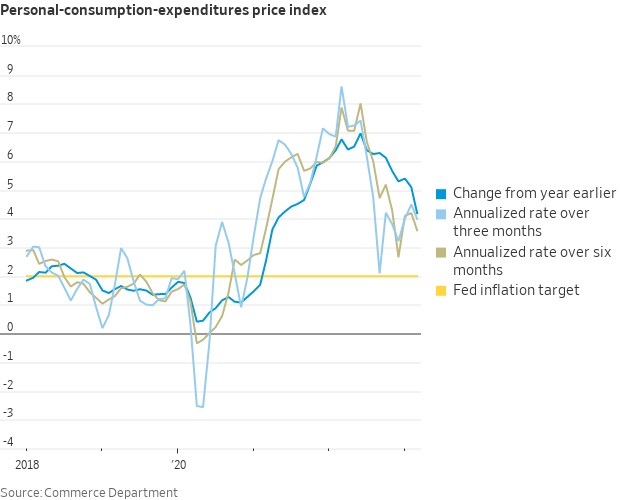

PCE inflation

Despite the Fed nearly done with rate hikes which can bring a weaker dollar, they may have to keep rates at lofty levels because core PCE is not coming down nearly as fast as overall PCE:

This implies stickier components such as food and rent could remain elevated for a prolonged period thus rates may too remain elevated.

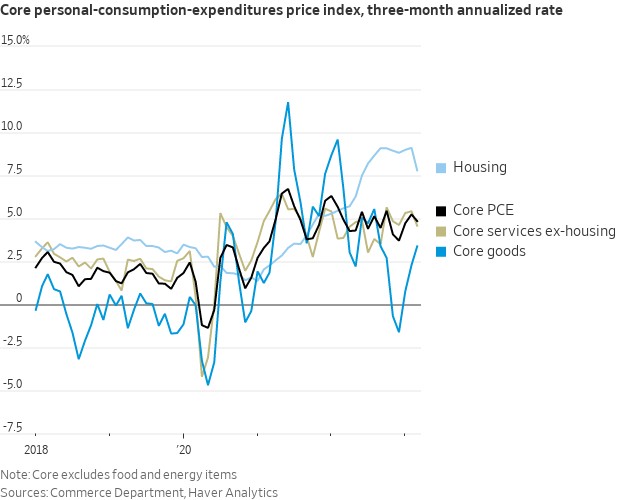

The core PCE matched estimates at 0.3% MoM but on a three-month annualized basis, core PCE goods inflation has bounced while shelter PCE is moderating.

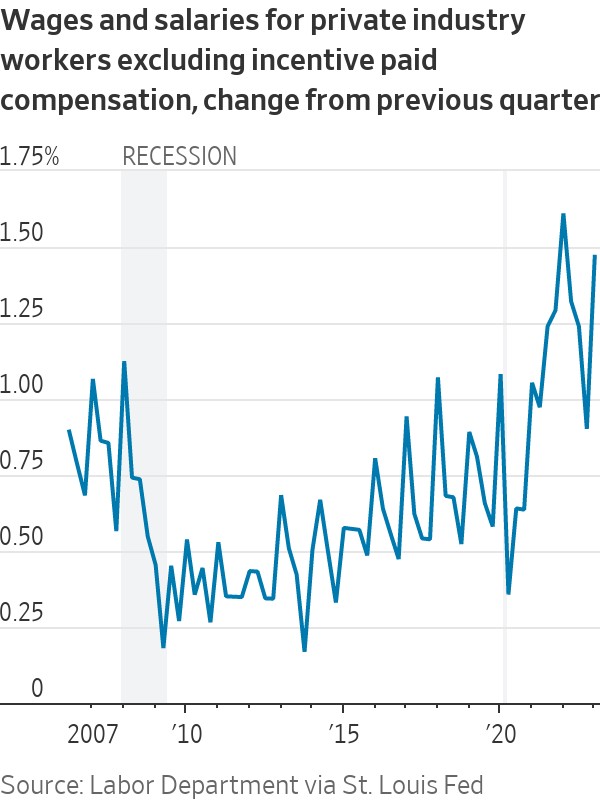

Wages and salaries for private sector workers excluding incentive paid occupations also showed no meaningful deceleration in Q1 +1.5% QoQ (the highest reading on record after the 1.6% gain in Q1 '22). The wage report from the ECI is important because several Fed officials have said it is their favored measure of labor compensation.

Ongoing banking crisis

First Republic Bank (FRC) then PacWest (PACW) have been the next dominos to fall with $102 billion in customer deposits leaving FRC. Notice how Bitcoin jumped higher in price during the price collapse of PACW yesterday? As with the other bank failures, First Republic has also faced losses on its loans and investments. JPMorgan Chase will acquire FRC so will backstop the deposits of FRC which eliminates the need for another one-off injection of QE to guarantee deposits exceeding $250,000, the limit for deposit insurance. But had a deal not been reached, the Fed would have had to inject another one-off round of QE to backdrop depositors to avoid a bank run. This begs the question of what bank will fall next and will they be bought out or will the Fed have to print?

According to Goldman Sachs, a 10% decline in bank profitability could reduce lending by 2%. If deposit betas reach 2007 levels, it could cause a 3% to 6% decline in lending in the US. With loan-to-deposit ratios sitting near 80% for many small banks compared with 60% for large banks, the likely solution for smaller banks will be to reduce lending, further slowing down the economy. One the one hand, this tightening of available liquidity could prevent the Fed from having to raise rates beyond Wednesday's 25 bps rate hike. Fed officials have said that while the battle with inflation is far from won, they may pause hikes after May but this is data dependent. But because inflation may remain elevated, so too may rates until the economy starts to show definitive signs of slowing even by the doctored data. Indeed, the Fed may have to stay hawkish given the stickiness of recent core inflation data and strong corporate earnings. Expect more chop as markets are about back to where they were a month ago having traded sideways since the start of April.