by Dr. Chris Kacher

The Federal Reserve which remains focused on inflation is likely to keep rates on hold at their upcoming meeting due to the stronger-than-expected 0.4% rise in average hourly wages.

But the Fed has a dual mandate to also keep unemployment at bay. A number of recent factors point to potential trouble ahead. The labor force participation fell to 62.4% from 62.6%, employment-to-population ratio dropped to 59.7%, the lowest since January 2022, 696,000 Americans lost their job in May, the second-largest number since 2020, and 623,000 people left the labor force in May, accounting for most of the decline in the household survey, among other factors. Despite these declines, the official unemployment rate held steady at 4.2% because many people exited the labor force entirely rather than becoming unemployed.

In consequence, CME FedWatch only sees two more rate cuts this year with a 99.9% chance of no rate cuts when they next meet this week.

The magnificent rocket

For the latest quarter, the Magnificent Seven posted aggregate earnings growth of 27.7% compared to a year ago. While that’s slightly below the average 32.1% seen over the last three quarters, it still outpaced the 9.4% of all the other companies in the S&P 500. Six of the seven names beat expectations, and total earnings growth exceeded forecasts by almost 15%. Various facets of AI are growing at beyond breakneck speeds, doubling every 6 months. This is producing hypergrowth among certain individuals and companies which, while perhaps a small but growing component of an individual's or a company's bottom line, is starting to make a material difference. No prior technology has compared to this level of growth. Even the fastest growth the internet experienced in its earlier days pales in comparison. This is why the Mag 7 have invested a massive part of their R&D into AI. Each knows that to maintain pole position, such investments are necessary.

Bitcoin in an AI world

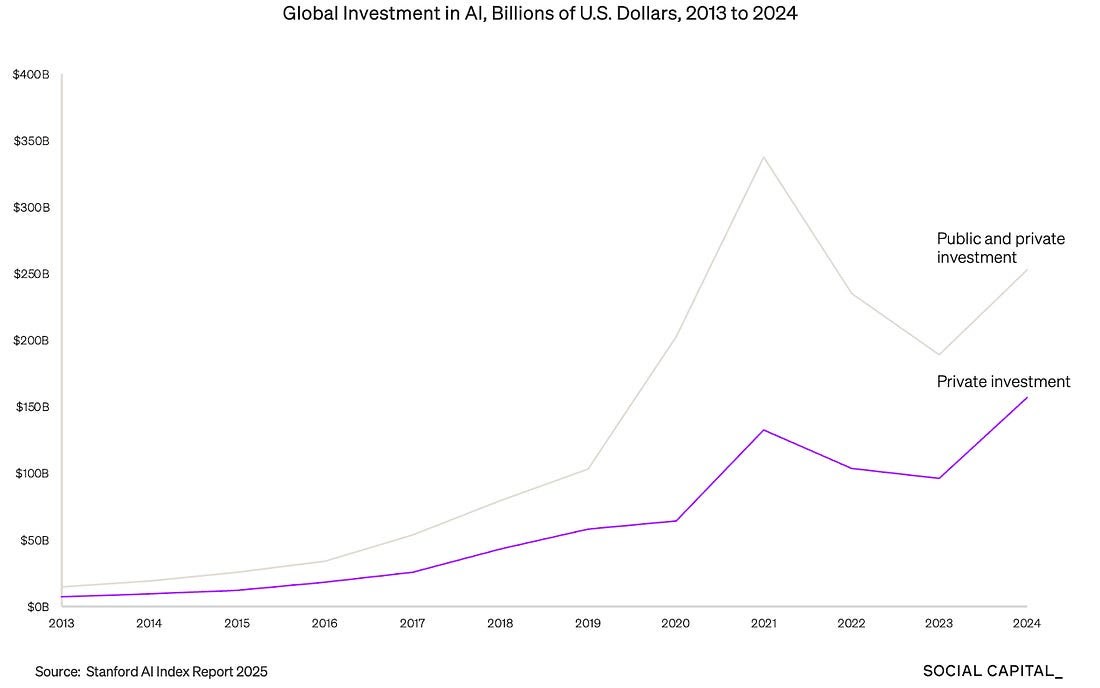

Venture private investment in AI reached a record $150 billion in 2024, nearly doubling from 2023 levels. Capital was allocated into every layer of the ecosystem, with the bulk of it going into the foundational model layer and the AI application layer. The momentum is carrying into 2025. The share of new venture funds focused on AI has grown dramatically, rising from just 5.4% in 2022 to 24.5% in 2025, reflecting exponential growth and strong investor confidence in the sector’s long-term potential. Mega-rounds—funding rounds of $100 million or more—are becoming more common, and the average deal size has soared. The overall pace and scale of investment suggest that the AI funding boom is accelerating as adoption broadens across industries and as new use cases and infrastructure needs emerge.

|

Bitcoin is one of only three enduring “moats” alongside gold and religion due to its:

Decentralization: No reliance on corporate structures or governments, making it resistant to AI-driven disruption.

Scarcity: Fixed supply contrasts with fiat currencies, which are vulnerable to inflation and geopolitical tensions.

Global utility: Enables fast, low-cost transactions critical for integrating unbanked populations into the AI-driven digital economy.

AI’s efficiency reduces the need for human labor and debt, accelerating the transition to a digital economy. Bitcoin, as a neutral medium of exchange, becomes essential in this landscape:

Replaces fiat: Tariff wars and distrust in government-backed currencies (e.g., USD) and government-backed bonds are pushing adoption.

Hedge against obsolescence: Unlike companies, Bitcoin isn’t tied to innovation cycles.Most corporations will struggle to maintain value in an AI-abundant future, whereas Bitcoin’s “lack of intrinsic value” becomes a strength.

The other week, Facebook parent META signed a 20-year deal to buy nuclear power from Constellation Energy, following the lead of its Magnificent Seven counterparts Microsoft, Google and Amazon which have made similar moves. We put out a report on some companies in this space. A handful of nuclear ETFs moved higher as the market knows that the next AI trade might be measured in kilowatts rather than chips. The Trump administration is pushing to quadruple US nuclear-generation capacity by 2050, and it’s also moving to streamline permitting in an effort to speed things up and spur investment. Regulatory easing will be key because it means lower cost and a quicker build for nuclear power plants. With Bloomberg Intelligence projecting AI energy demand to rise as much as ten-fold this decade, nuclear could end up as the next leg of the AI trade.

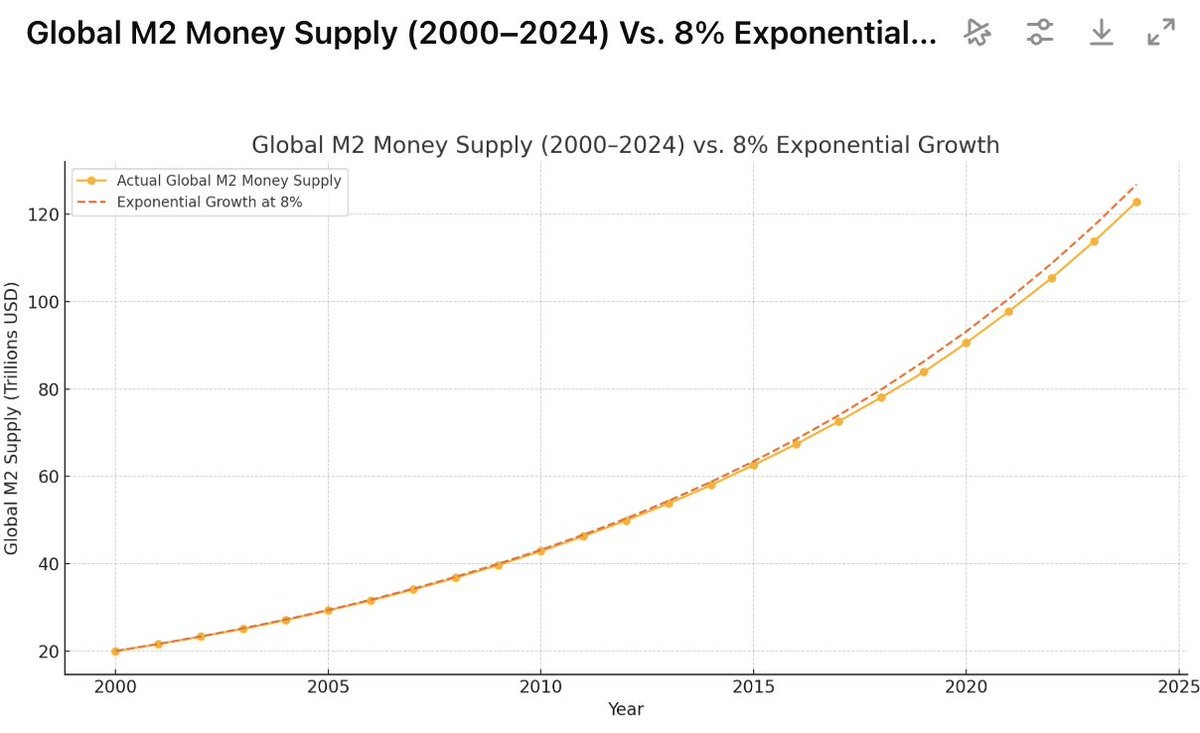

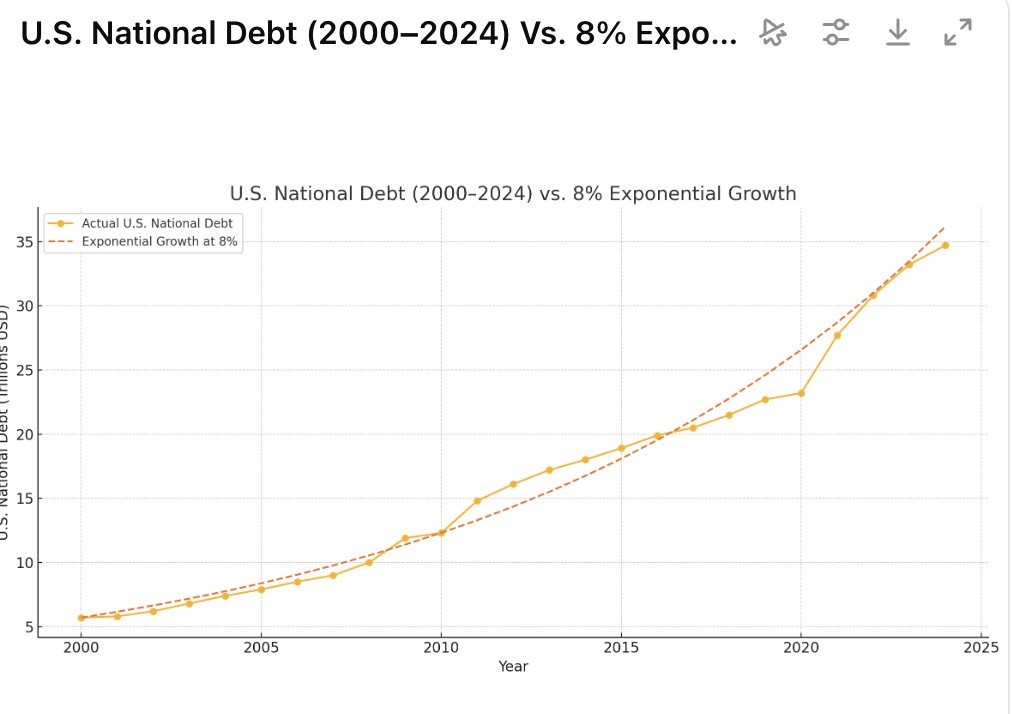

8% annualized debasement of fiat

Both global money supply and US national debt have been growing at 8%/year. This is a measure of overall inflation.

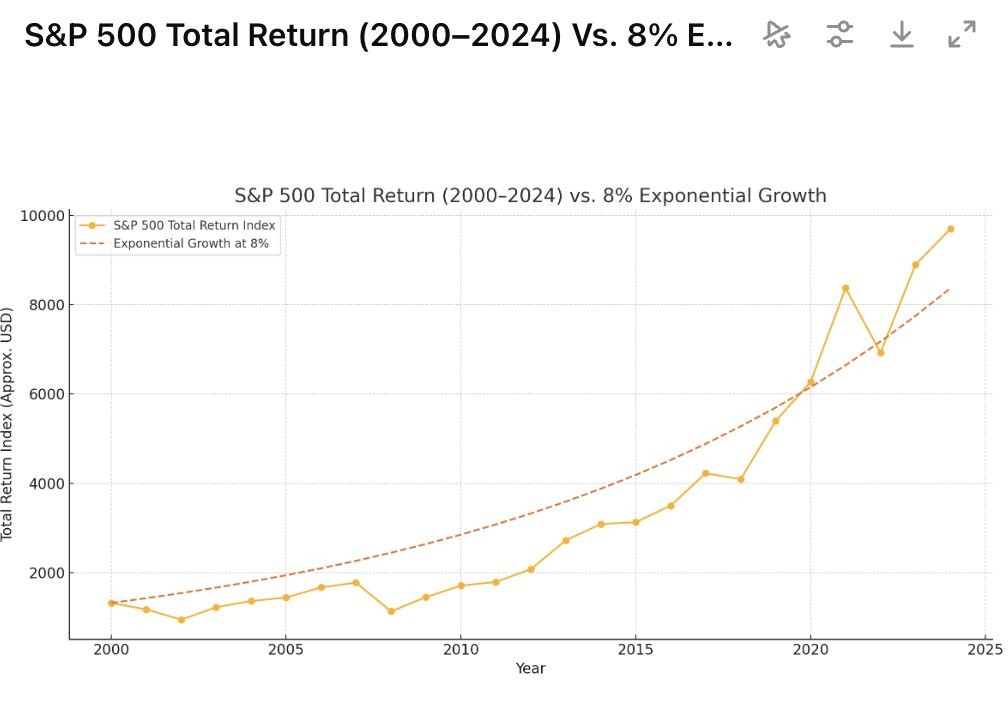

Meanwhile, the S&P 500 has been growing at roughly 8% before taxes.

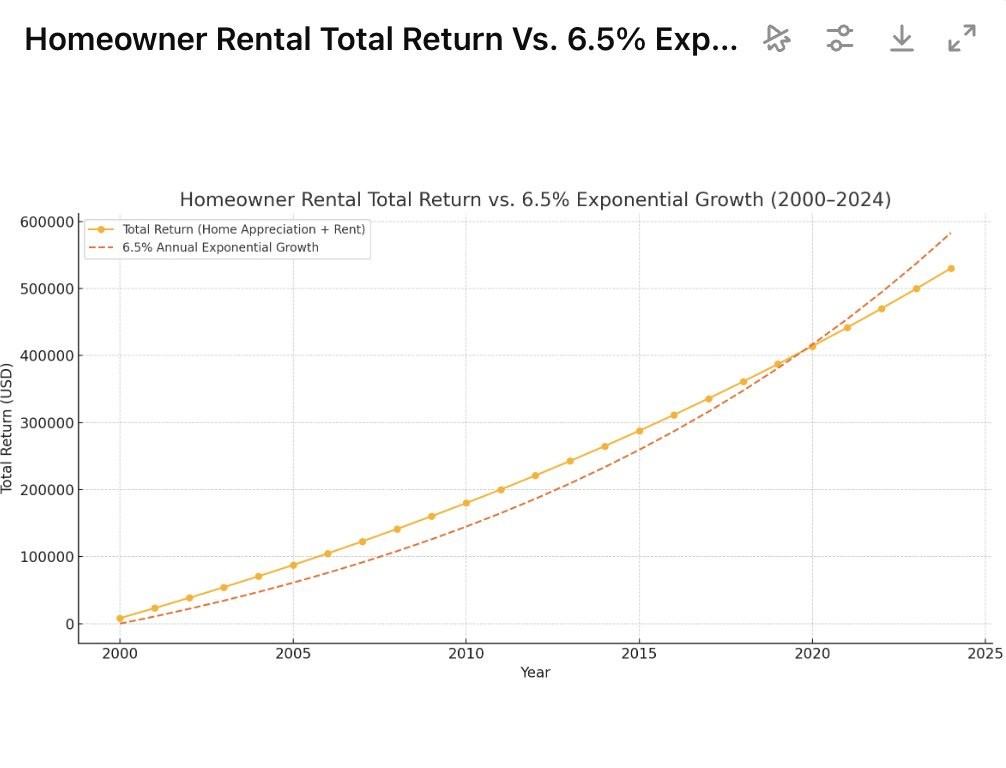

Housing only returns 6.5% annually.

So neither stocks after taxes or housing make up for inflation. Bitcoin is the only asset that beats inflation. Its annual growth rate over the last 10 years is 85% and if you look over the last 5 years, bitcoin’s compound annual growth rate is 62%.

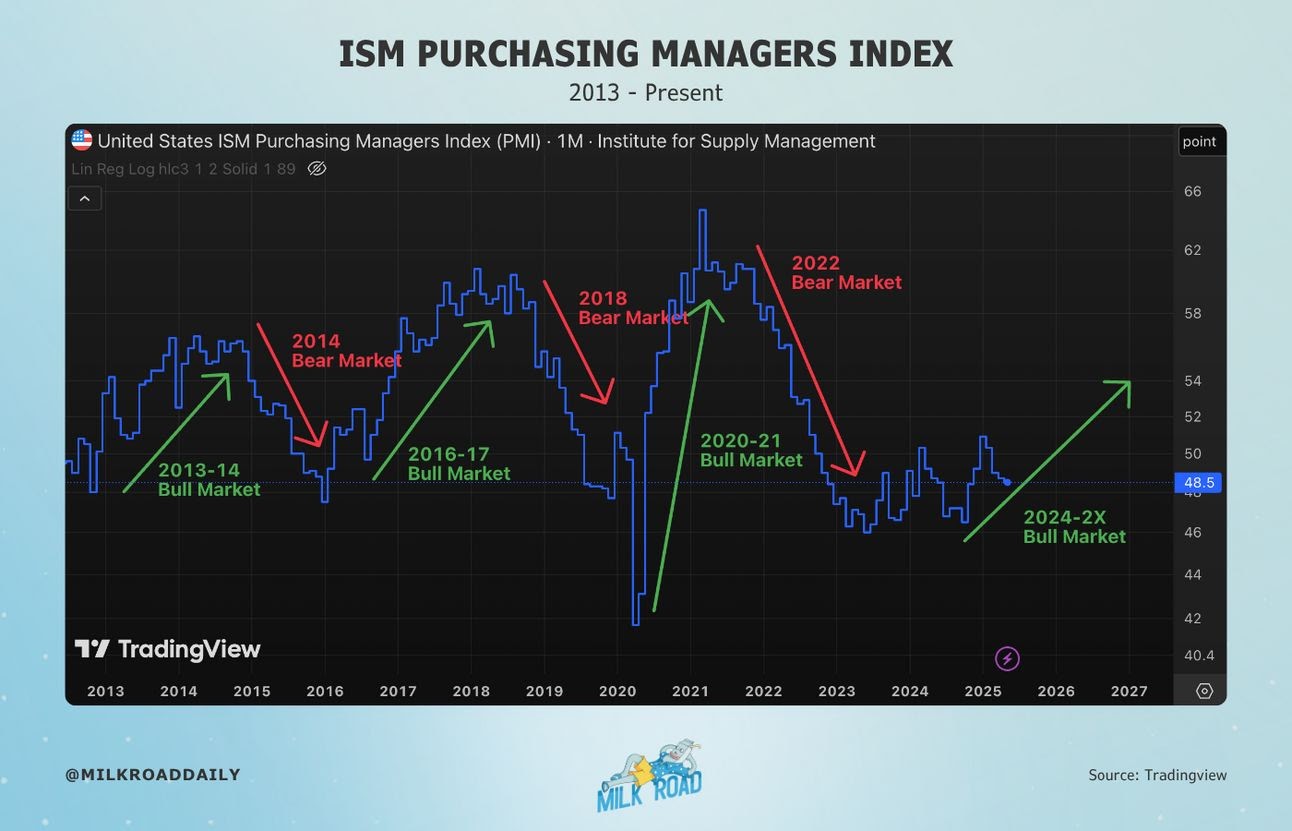

ISM

Finally, as discussed in prior reports, the ISM purchasing managers index shows that while 2024 was 5 steps forward, 4 steps back, rhyming with what we saw in 2015-2016, it is likely to trend higher in the coming months, bringing Bitcoin along for the ride. The necessary component of global liquidity is also likely to trend higher when both public and private investment are considered especially as rates continue to fall. Even should rates on the long end rise, this is bullish in the long run for Bitcoin as diminishing confidence in sovereign debt takes hold.

That said, this is the first time the ISM has been trending in a choppy, sideways manner. While various metrics I've discussed in prior reports show it should resume to the upside, the market climbs a wall of worry. The worries right now are that the long end of the yield curve continues to rise. We also have issues in Japan on their yields plus the yen carry trade matter. The market also continues to worry about not if but when recession. Should recession hit, Bitcoin is not immune nor is the ISM purchasing managers index. But so far, economic signs suggest stability in jobs and inflation which can push rates lower. We also have M2 money supply as well as global liquidity which continue to trend higher, keeping the momentum. These two forces are fundamental to where markets go. So until we get surprise rate hikes which also end up slowing global liquidity, signs point to overall higher markets ahead, minus the occasional sharp pullbacks due to news-related events such as tariffs, bond yields, or worries about the economy that could push rates higher.