by Dr. Chris Kacher

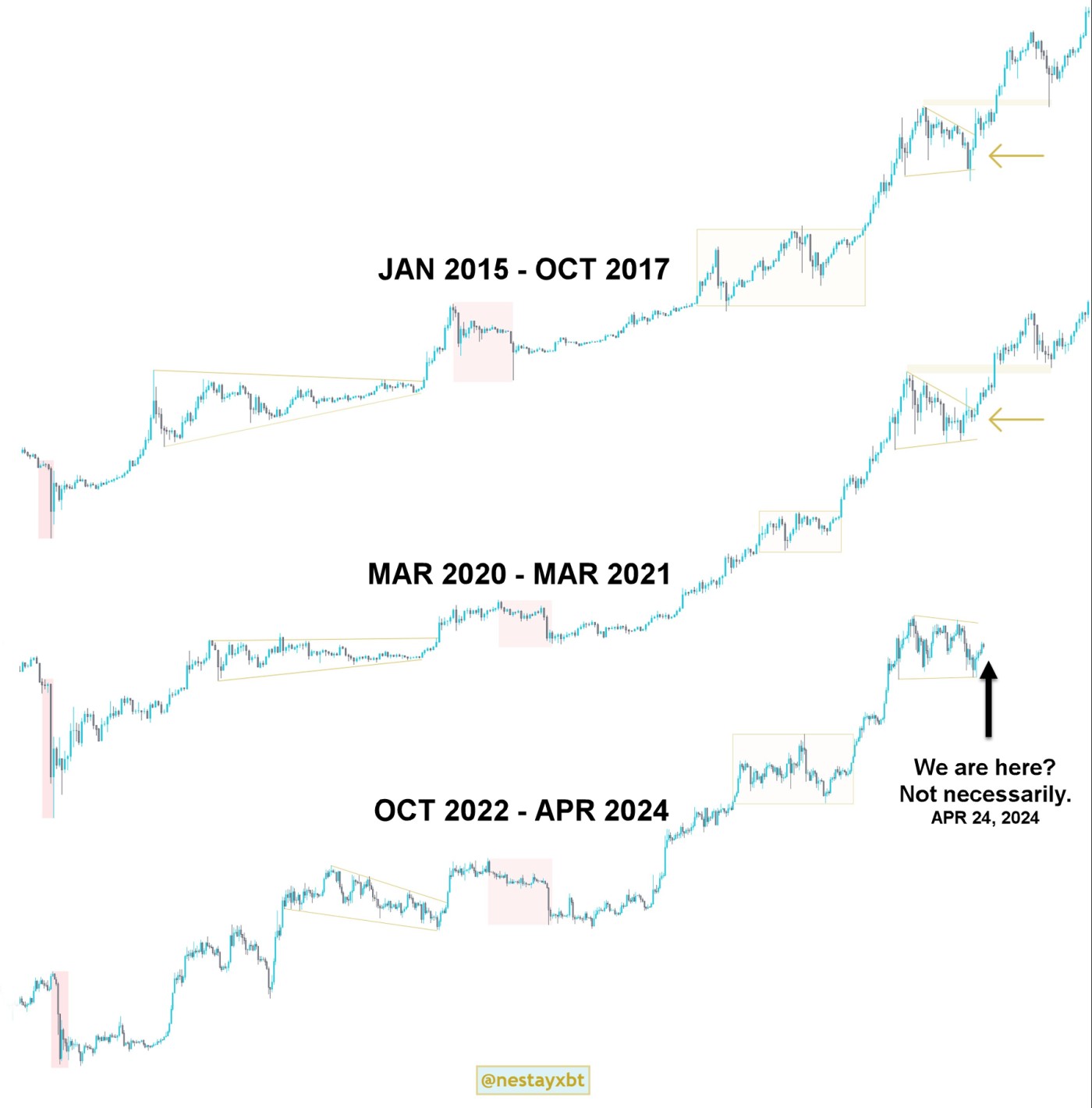

The following chart shows where we are now in the Bitcoin cycle. ETH has always topped later with alt coins making huge gains near the end of the ETH top. Bitcoin has been in a downtrend with lower highs and lower lows.

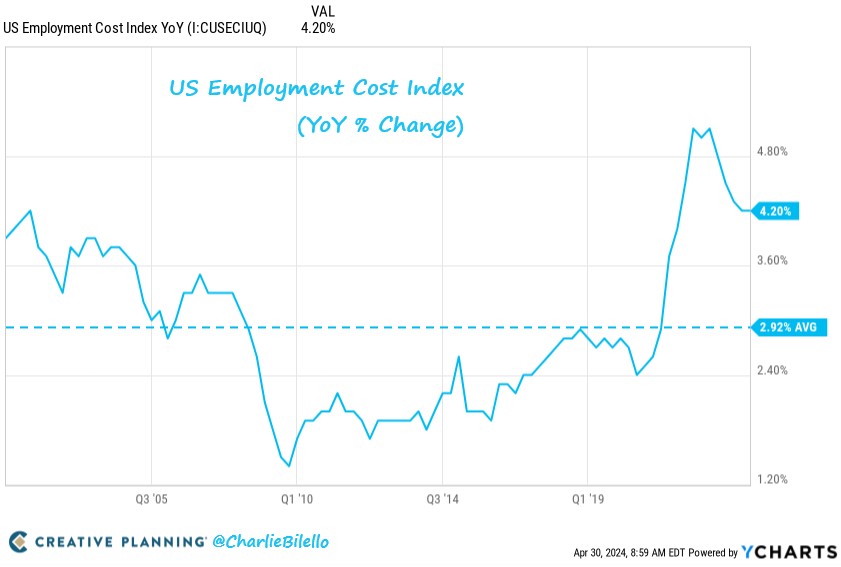

While history suggests Bitcoin will eventually resolve to the upside, Bitcoin still remains a highly risk on asset so relying on two prior events is unwise. Rather, Bitcoin's general direction will largely depend on global liquidity which continues to fall and on inflation which has come in above estimates across three CPI reports, the recent PCE, and the US Employment Cost Index.

This will keep interest rates higher for longer. They may even get hiked if hot inflation persists. According to CME FedWatch, only one rate hike is now priced in for the remainder of this year. I have been saying all year that global liquidity continued to fall which was a concern since macro is one of the key metrics when it comes to general market direction. Nevertheless, a few bullish factors countered this fall in liquidity, plus there can be a lag time of a number of weeks between macro and market direction but markets eventually follow macro.

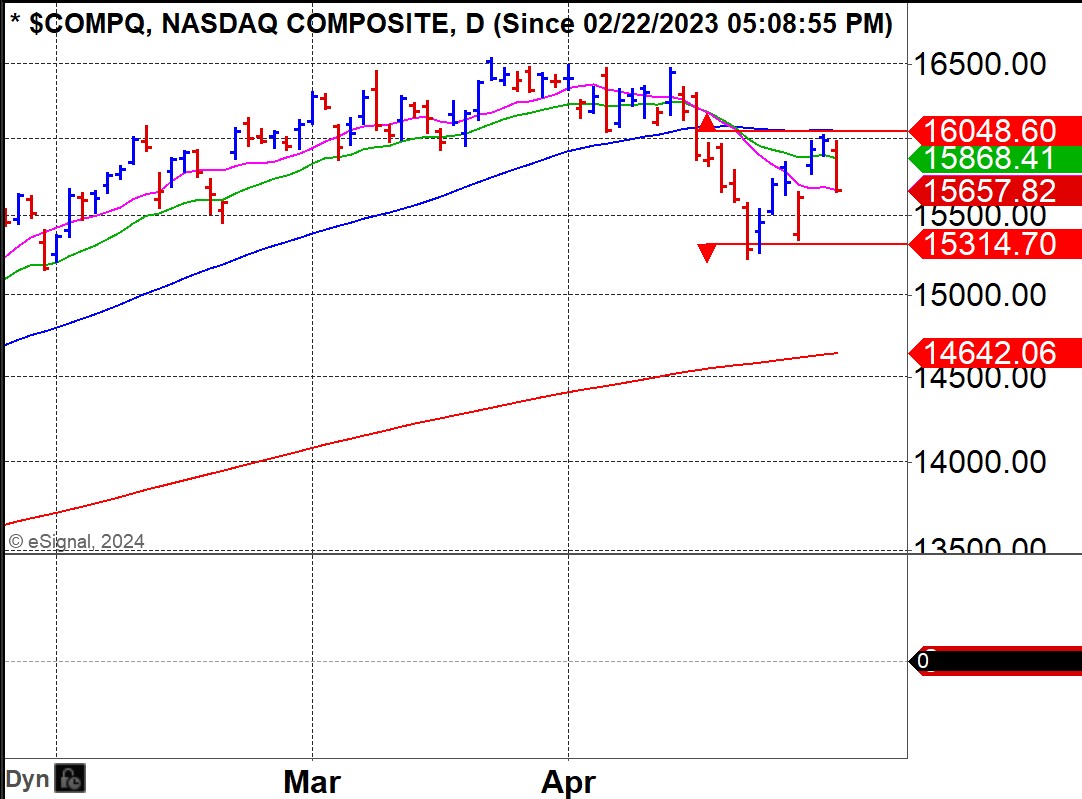

Liquidity, inflation, and interest rates continue to look bearish for both Bitcoin and stocks. Further, both leading AI meme stocks AMD and SMCI could not manage strong earnings reports. Will NVDA also succumb when it reports on May 22 after the close? The current action in the major averages shows the dead cat bounce is rolling over.

Bitcoin spot ETF inflows have been falling along with GBTC outflows. While spot ETFs still can be a bullish factor, inflows have been negative due to weakness in the markets. Investors put less money into corrective markets as we are currently witnessing in both stocks and Bitcoin. Major institutions with Bitcoin mandates therefore have less inflows from investors, so they need to buy less Bitcoin. Meanwhile, sell orders persist which can well exceed any inflows, so dont assume heavy selling of Bitcoin cant take place within these spot ETFs.

Further, there is an overly optimistic expectation of the Bitcoin halving that disagrees with history. In the weeks following the prior two most recent halvings (May 11, 2020 and July 9, 2016), Bitcoin traded in choppy fashion. Bitcoin did not launch into a sustainable uptrend until a few months later. But keep in mind that the macro picture looked healthy after prior halvings. Macro takes priority so until it improves, Bitcoin is unlikely to manage any sort of sustainable uptrend.

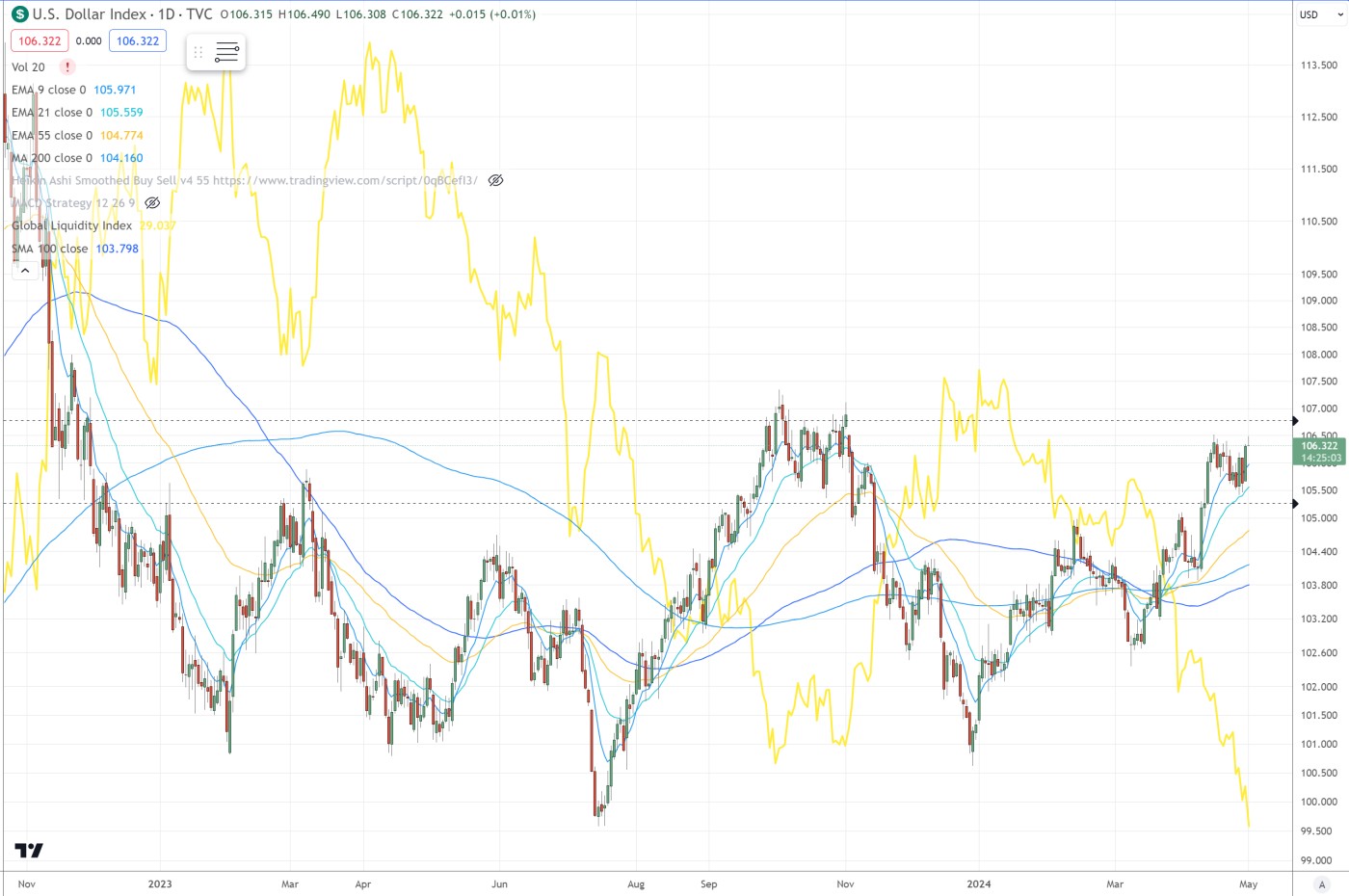

Global liquidity, inflation fears, and interest rates

Stealth QE remains intact but for now remains insufficient to counter diminishing global liquidity, inflation fears, and interest rates. I continue to closely monitor these three metrics among others.

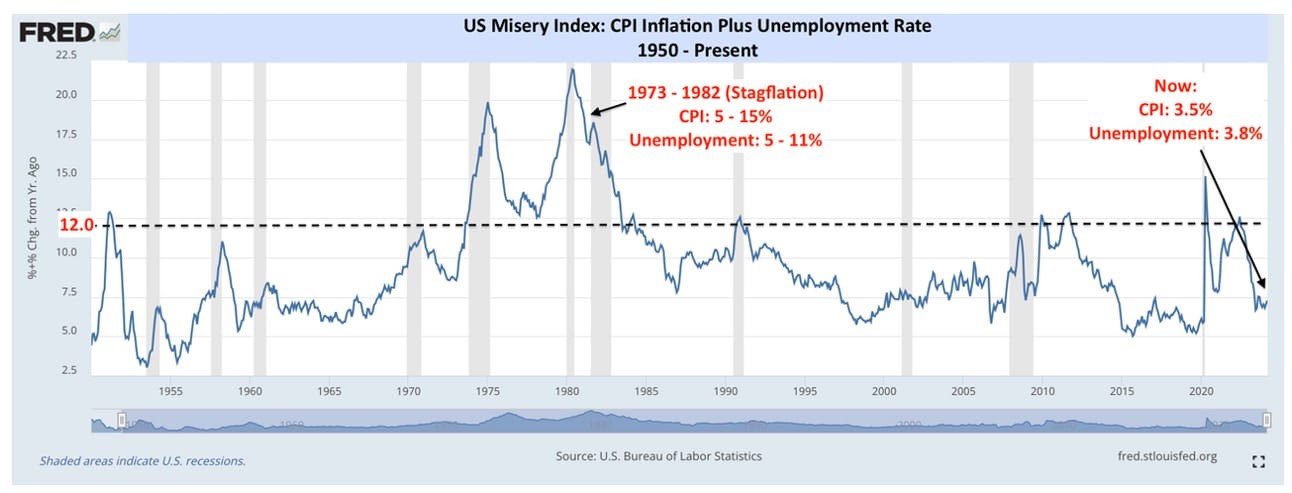

Comparisons between now and the 1970s show inflation and unemployment were far worse then than they are now.

But the risk in both cases is stagflation. Should the economy falter or another black swan arise, the Fed would likely unleash more quantitative easing (QE) which would breath life back into markets. For now, with the economy still looking okay despite the weak GDP number and with hot inflation, the Fed's hands are tied. They must keep rates higher for longer. This has been the case for other major central banks, thus global liquidity continues to fall. The 10-year Treasury and dollar continue to trend higher as an omen for potentially higher rates which could materially weaken the economy.

In the meantime, stealth QE is alive and well. US government spending (inflation-adjusted) since 2020 now exceeds the combined spending of: World War I, World War II, and the 1970 to 1990 time period.

|

Inflation therefore remains elevated. The government is spending like drunken sailors. Due to QE, the US consumer and major corporations have extra cash in their coffers. In fact, US corporations have never had more cash on-hand than they do right now. Some of this liquidity finds its way into stocks, real estate, and Bitcoin. Expect more of the same with intermediate corrections along the way such as the one we are in right now as the inflation megatrend runs its course with additional QE at the ready when the Fed most needs it as such has been the case since 2008 when QE was first launched. That said, the only correction that could be classified as a bear market was the one in 2022 when the Fed hiked rates at a record pace. Should the Fed break with tradition and not supply the markets with money created from QE in the event of an incoming recession, expect another bear market. However, given Powell's testimony on Wednesday, he is likely to supply the market with additional liquidity. He will start tapering the taper in June.