by

Dr. Chris Kacher

Gold's Rally in Times of Crisis: Wars, Financial Turmoil, and the 2008 Lessons

Gold has long been viewed as a safe-haven asset, often surging in value during periods of economic upheaval or geopolitical conflict. Historically, it rallies at the onset of wars due to heightened uncertainty, inflation fears from disrupted supply chains (like oil), and a flight to tangible assets amid market volatility. For instance, during the 1990-1991 Gulf War, gold prices climbed about 7.5% over six months, while the 2022 Russia-Ukraine invasion sparked similar gains of 5-15% in the initial months as investors sought protection from risk.

The 2008 global financial crisis provides a classic case study of gold's behavior in economic crises. Triggered by the Lehman Brothers collapse and banking failures, the crisis unfolded in two phases for gold:

1. **Initial Plunge Amid Liquidity Panic**: In late 2008, prices dropped roughly 30% from around $1,000 per ounce to $700, as investors liquidated assets—including gold—to secure U.S. dollars for margin calls and deleveraging. Here, gold acted like a commodity, correlating with falling stocks rather than as a haven.

2. **Strong Recovery and Rally**: As panic eased, central banks like the Federal Reserve slashed interest rates to near zero and unleashed quantitative easing (QE), flooding markets with money. This weakened the U.S. dollar, ignited inflation concerns, and eroded faith in fiat currencies. Gold rebounded sharply, soaring over 170% from $700 in late 2008 to a 2011 peak of $1,917 per ounce. Key factors included a flight to safety from crashing equities (stocks fell 37% in 2008), its role as an inflation hedge, and dollar depreciation making it more accessible globally.

| Period | Gold Price Change | Key Drivers |

|--------|-------------------|-------------|

| Sep-Oct 2008 (Crisis Peak) | -30% (~$1,000 to $700/oz) | Liquidity crunch, asset sales for USD |

| 2009-2011 (Recovery) | +170% (~$700 to $1,917/oz) | QE, low rates, inflation fears, weak USD |

In essence, gold's post-2008 rally wasn't driven by the crash itself but by the policy response—loose money that devalued currencies and boosted demand for gold as a store of value.

Contrast this with the ongoing 2026 US-Iran conflict, which began with US-Israeli strikes on February 28 and has spiked oil above $100 per barrel. Despite an initial jump to ~$5,400 per ounce, gold has since retreated to around $5,100, down 2.5% weekly. Why no sustained rally? A strong U.S. dollar as a rival safe haven, high Fed rates (3.5-3.75%) raising gold's opportunity cost, profit-taking after 2025's 50% surge, and war-fueled inflation potentially delaying rate cuts are overriding traditional boosts. Odds markets said European Central Bank rate hike odds rose to 70% for two 25bp hikes by year-end 2026 (first by July), driven by soaring energy prices and inflation fears—reversing prior cut expectations. Broader 2026 hike odds sit at 44% on Polymarket.

Analysts predict possible gold upside to $6,300 by year-end if escalations continue, but today's environment—unlike 2008's easing—highlights how macro conditions can mute gold's geopolitical appeal.

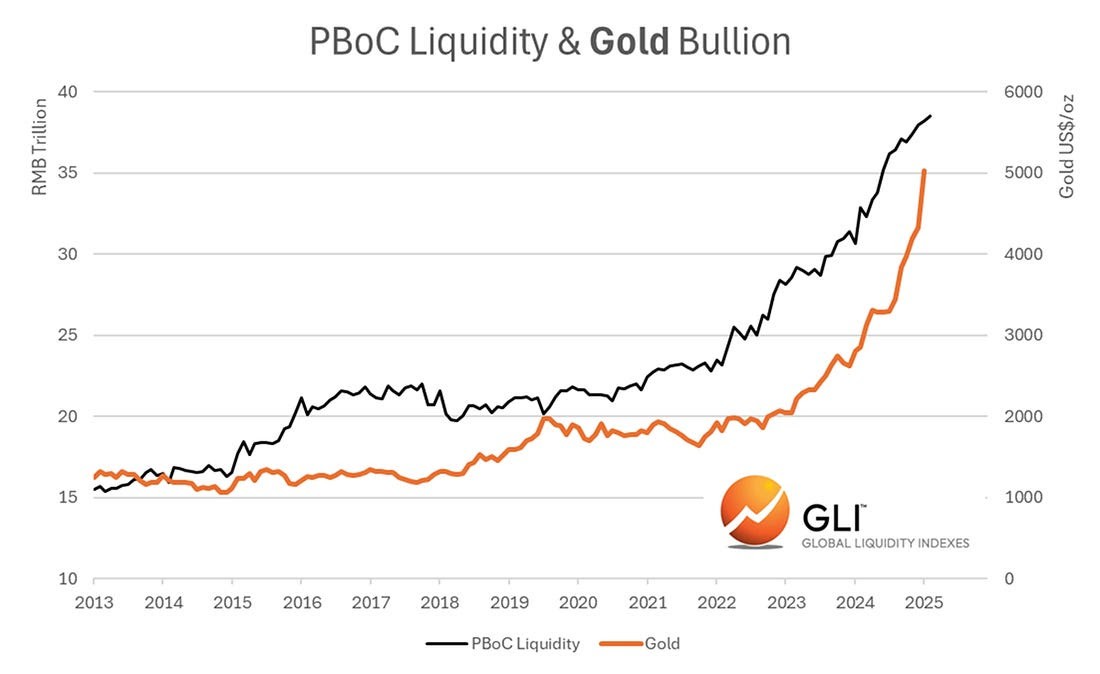

China PBoC Liquidity vs Gold

That said, gold's price dynamics are driven more by structural, long-term factors like China's aggressive stockpiling than short-term geopolitical flares like the Iran conflict. While the recent pullback in gold might seem counterintuitive given the war premium, the China angle provides a stronger explanation for gold's overall resilience and potential rebound.

### On Gold's Recent Dip (Going Lower Short-Term)

Gold's correction today isn't surprising in a volatile environment—it's down from recent highs near $5,400+, but this is typical profit-taking after a rapid surge. Key pressures include:

- A stronger US dollar (DXY up to ~99.1–99.3, a one-month high), which makes gold more expensive for non-USD buyers and exerts inverse correlation drag.

- Reduced near-term rate cut expectations (e.g., June hold odds >60%), as oil-driven inflation risks (Brent ~$80–$84) could keep real yields higher, increasing gold's opportunity cost.

- Overbought technicals after war-fueled buying—gold had rallied aggressively on Iran escalation, so a breather was due.

Historically, gold bugs do associate Middle East tensions (like 1979 Iran Revolution or Gulf Wars) with bullion spikes, as investors seek safe-havens. The current Gulf events (strikes, retaliation, Hormuz risks) have added a ~5–10% premium, but if they de-escalate quickly (per Trump's "weeks" timeline), further spikes may fizzle, contributing to near-term weakness. However, the narrative correctly points out this is secondary—the bigger story is China's role, which could limit downside and propel new highs.

### China's Stockpiling: The "Bigger Point" and Its Implications

Evidence strongly supports the claim that China is covetously stockpiling gold, both officially and potentially "secretively," as a strategic move tied to Yuan monetization and de-dollarization. This is disappearing into state coffers and private vaults, creating a structural demand floor for gold that's more powerful than episodic war trades.

- **Official Data**: The People's Bank of China (PBOC) has added gold for the last 15 consecutive months, lifting reserves to a record 2,308 tonnes (up 1.2 tonnes in January alone). This represents ~9.6–9.7% of total reserves, but analysts suspect underreporting—real holdings may be closer to 5,000 tonnes, with purchases potentially 10x higher than disclosed (e.g., Société Générale estimates up to 250 tonnes in 2025 vs. official 25 tonnes).

- **Dumping US Treasuries**: China has slashed U.S. Treasury holdings by ~11% YoY to $682–$775 billion (lowest since 2001), down from a peak 28.8% share in 2011 to just 7.3% now. This shift redirects capital into gold, reducing reliance on USD assets amid sanctions risks and volatility.

- **Private/Retail Demand**: Chinese households and institutions are fueling volatility—gold-backed ETF holdings doubled since early 2025, and Shanghai Futures Exchange volumes average 540 tonnes/day (up from 457 in 2025). Retail sees gold as "insurance" (currently ~1% of assets, potentially rising to 5%), with citizens facing limited financial options (falling housing prices, low 1% deposit rates).

- **Link to Yuan Monetization**: This stockpiling is interpreted as "secretive" support for Yuan internationalization—gold bolsters reserves without overt USD dumping (to avoid market disruption). It ties into de-dollarization efforts (e.g., oil trades in Yuan), hedging against U.S. financial pressure.

The chart explains puzzling dynamics:

- **US Treasury Stability**: China's gradual unwind (not a dump) of U.S. Treasurys avoids spiking yields/term premia—holding steady despite deficits, as other buyers (e.g., Japan, UK) step in.

- **Lackluster Crypto Market**: Crypto (BTC/ETH down YTD) suffers from risk-off flows and competition as "digital gold," while physical gold benefits from central bank/institutional preference amid de-dollarization. China's crypto bans reinforce this shift to traditional gold.

### Implications for Gold Prices

While Iran tensions provide short-term volatility (bullish spikes on escalation, pullbacks on de-escalation), China's demand is a **structural bull case**—limiting how low gold can go and positioning it for new highs ($5,500–$6,000+ by end-2026 in many forecasts). If stockpiling accelerates (e.g., to counter sanctions or boost Yuan credibility), it could outweigh war noise, explaining gold's resilience despite recent dips. The narrative is spot-on: Geopolitics grabs headlines, but China's "quiet" accumulation is the real macro force.