by Dr. Chris Kacher

Is deflation already here?

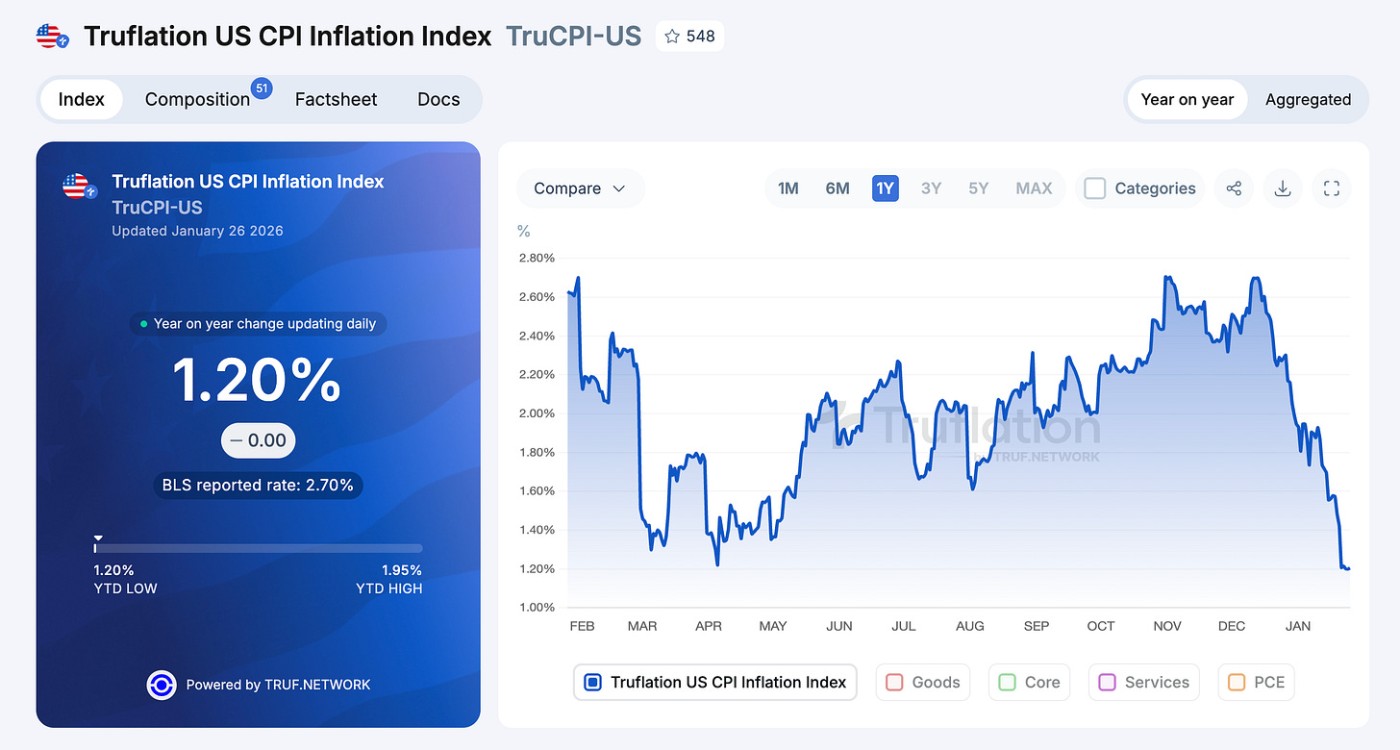

With advances in technology, deflation may beat inflation. Over the last year, mainstream media’s fear-mongering has been warning about inflation, but inflation actually fell at a rapid pace. Truflation is currently showing real-time inflation at only 1.2% year-over-year. Inflation has collapsed from its recent peak, dropping 151 basis points in just three months.

Contributing to this is a weakening labor market along with AI which is a very real deflationary force, and productivity which is booming thanks to the deregulation, tax cuts, and reshoring of American jobs and manufacturing. Trump's tariffs are another new factor. All of this has rapidly changed economic conditions of markets, and it is putting the Fed on their back foot. How well does the Fed really understand substantial changes across the economy, including new policies and advancements in cutting-edge technology like AI? Mainstream media doesn't seem to get it but that's standard.

Elon Musk has said deflation will outpace inflation caused by QE within the next couple of years. As one of many examples, insurance technology company Lemonade has announced that it will offer a 50% rate cut for drivers of Tesla vehicles with FSD steering because it had data showing it reduced accidents. Technology improved and prices dropped.

In education, Chegg (homework help SaaS) saw its stock plunge 50% in 2023 after admitting ChatGPT was eroding subscribers. Students switched to free/low-cost AI for answers, deflating edtech pricing.In music, from $15 CDs in the 1990s to $10/month unlimited Spotify today (or free ad-supported YouTube), digital tech has deflated music costs by 90%+. digipal.ai AI-generated music (e.g., Suno or Udio) is now pushing even further, creating custom tracks for pennies or free.

In healthcare, tools like AI diagnostics (e.g., Google's DeepMind for eye scans) reduce costs 20–30% by catching issues early. Drug discovery AI (e.g., AlphaFold) has slashed R&D timelines from years to months, potentially deflating pharma prices.

In supply chain logistics, Amazon's 520,000+ robots in warehouses have deflated fulfillment costs, enabling cheaper/faster shipping.

Musk has said AI and robotics will create "significant deflation" within "three years or less" (by around 2028) because productivity/output of goods and services would surge faster than governments can print money.

What if bond markets are dead wrong?

Long-term Treasury yields are spiking even as the Fed slashes rates. Classic signal: bond traders smell sticky inflation ahead. Higher yields offset the erosion of fixed coupons' real value. Old-school view? The market's calling the Fed's bluff: "2% inflation? Nah, it's going higher."

There's nuance: yen stress might force Bank of Japan to dump U.S. Treasuries, pushing the Fed to print and cap long-end rates. Markets aren't crystal balls.

But what if Elon Musk and the AI army are right? What if robotics, AI productivity bombs, and tech's relentless cost plunge unleash massive deflation? Musk's call: "three years or less" to output exploding past money supply.

Early proof? Lemonade's slashing auto rates 50% for Tesla FSD drivers. Crashes plummeted. Insurance gets dirt cheap when AI safety works.

My base case: deflation's already here.

Sticky CPI (~2.7% late 2025) masks the truth. "Diabolical" inflation in non-tradables (education, healthcare, food, energy, housing) stays glued by regulatory capture, zoning hell, medical monopolies, farm subsidies, and permitting nightmares.

But tradables? Deflation tsunami:

Batteries: -90% in a decade

Solar panels: plunging

Compute: exponential drops

Streaming/edtech: ChatGPT kills premium tutoring

Logistics/robotics: imminent

The regime flip is coming fast.

Musk's abundance shock isn't making rent free tomorrow. It's tradables going near-zero, real purchasing power exploding, non-tradables cracking:

AI diagnostics gut healthcare overhead

Online certs nuke college debt traps

Modular/3D housing smashes zoning walls

Watch the canary: long-end yields.

If they roll over while Powell preaches "soft landing," reflation trade dies ugly. Deflation wins. Next 12-24 months sort signal from noise. Which "un-deflatable" sector breaks first? Game over.

Japanese bond yields drive QE

Normally, no rate cuts would be bullish for the dollar. But as I mentioned briefly above, the recent stress in the yen and Japanese government bond (JGB) market is a warning signal that could trigger a new round of indirect money printing by the Fed which supports more global liquidity which is bullish for markets.

The yen has weakened while long-dated JGB yields have risen, signaling loss of confidence in Japan’s ability to control inflation, deficits, and its bond market.

- This creates a risk that Japanese investors dump U.S. Treasuries and repatriate capital, pushing U.S. yields higher just as the U.S. runs massive deficits.

- The U.S. will not allow this and will respond via a coordinated Fed–Treasury–BoJ setup that quietly expands the Fed’s balance sheet.

From this, the dollar weakens which loosens financial conditions without a rate cut by easing capital at the margins while supporting corporate profits.

A weak dollar also offsets the Trump tariff impact. Stephen Miran’s infamous paper titled A User’s Guide To Restructuring the Global Trading System clearly states, “Tariffs provide revenue, and if offset by currency adjustments, present minimal inflationary or otherwise adverse side effects, consistent with the experience in 2018-2019. While currency offset can inhibit adjustments to trade flows, it suggests that tariffs are ultimately financed by the tariffed nation, whose real purchasing power and wealth decline, and that the revenue raised improves burden sharing for reserve asset provision.”

In the end, all of these factors help lift stocks as global liquidity expands.