by Dr. Chris Kacher

A perfect storm

The perfect storm of 1) temporarily easing global liquidity combined with an economy that is growing but not as fast as some would like, 2) the Fed's initially hawkish stance on a rate cut in December due to inflation, 3) overvalued AI stocks, and 4) the jobs report giving the Fed reasons not to cut rates all caused the November sell off in stocks and bitcoin. A large fear is that the AI spending frenzy may not generate the returns needed to justify the investments, which is why tech stocks have been hammered this month. Yet nothing fundamental has changed regarding AI and bitcoin. That said, bitcoin has come under selling pressure due to two temporary one-offs: 1) market maker liquidity which has been scant for several weeks, and 2) possible removal of MSTR from indices. We wrote about both in prior reports.

This is therefore potentially another correction, not a major top, in the context of a bull market.

Steady payroll growth above estimates (strong) alongside rising unemployment (weak) complicates the Fed's policy outlook by sending conflicting signals about the labor market's health and inflation risk. This tension leaves risk assets vulnerable to whipsaw moves as investors weigh these opposing indicators ahead of the Fed's December meeting. Nevertheless, John Williams indicated that the Fed could lower interest rates in the near term, a statement perceived as dovish by the market. His remarks, coming from a key policymaker, significantly shifted sentiment. The odds of a rate cut in December jumped from under 40% to 84% on Polymarket and 83% on CME FedWatch.

Is the growth of AI truly transformative enough to warrant today’s elevated valuations?

ChatGPT alone has more than 10% of the world's population using the platform. Meanwhile, AI allows companies to do more with less so job cuts will continue. At the same time, new jobs are being created at an even faster pace due to AI. AI is already outperforming humans in most tasks including senior-level professionals. AI will power humanoid robots, autonomous vehicles, drones, and countless other machines that will reshape our world. Massive sums are being invested into these areas. Change is becoming hyperexponential. Over the decades, companies that embraced new technologies did well. AI is the largest tsunami yet. A log plot of QQQ underscores this trend. The straight line shows growth is exponential. Global liquidity correlates highly with QQQ. Whenever its rate slows, so do both stock and bitcoin markets at least on a quarterly timeframe if not sooner.

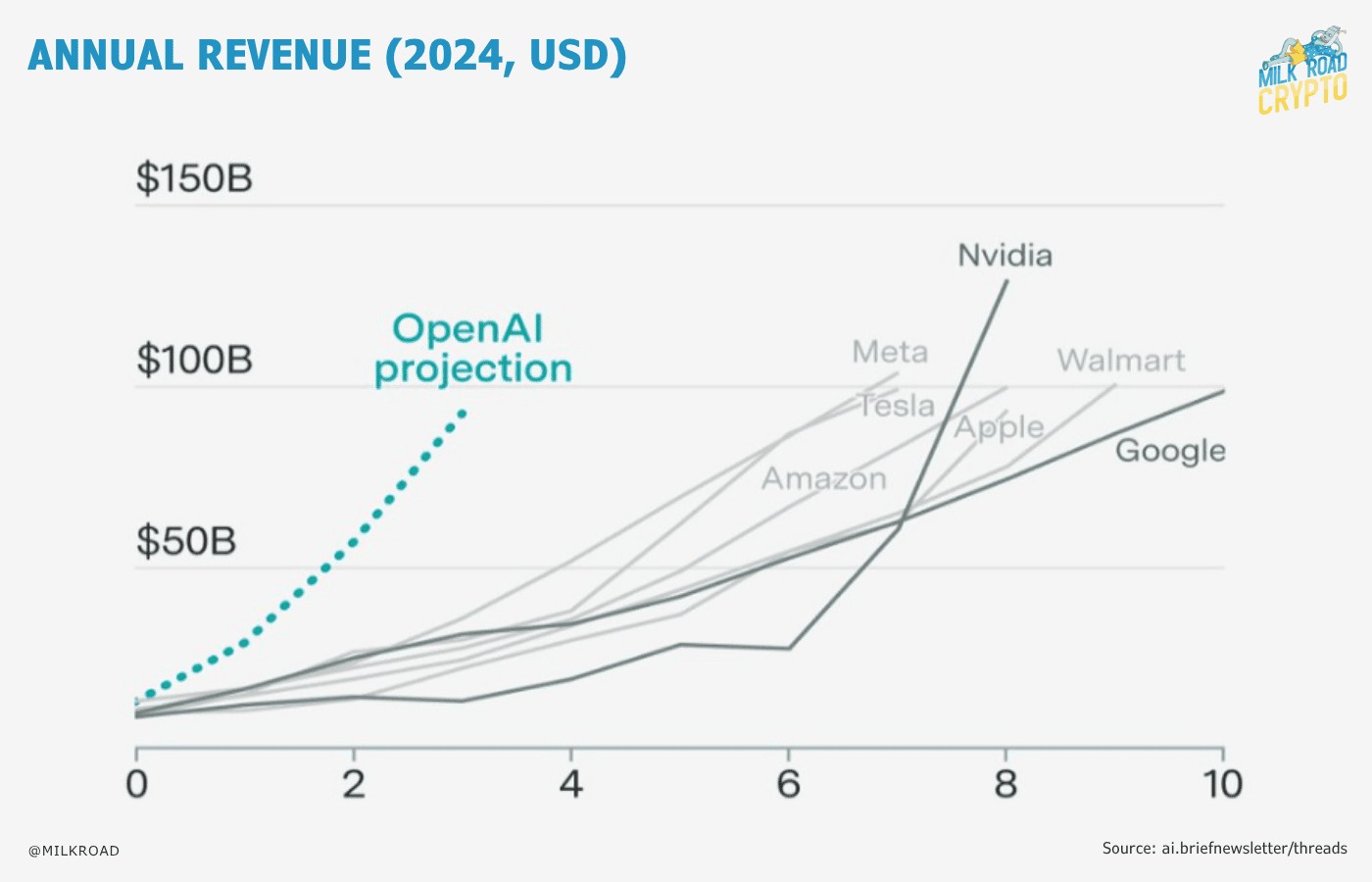

OpenAI is looking to be the fastest growing company yet. Its proposed $1 trillion IPO offering sounds staggering, like something that would occur around a major market top, especially when you consider that it is operating at a loss, maybe akin to AMZN in its early years despite its stock that continued to hit new highs due to immense growth potential. Many AI companies are currently unprofitable but are attracting massive valuations based on long-term societal and economic impact. Footing the bill are all the AI hyperscalers such as GOOGL, MSFT, META, and AMZN. One may think this is sounding like a Ponzi scheme where one segment feeds the other into eventual collapse. But they all see long-term strategic value that far outweighs any short-term profits.

For example, they want to lock in customers early, so when AI becomes more mature and profitable, everyone is already using their products. They are also willing to offer AI tools even at a loss because the data they collect helps them improve faster giving them a long-term edge. Companies that own and operate the essential hardware, data centers, and cloud services powering AI applications hold a critical and lucrative position in the AI ecosystem. Dominating infrastructure is key.

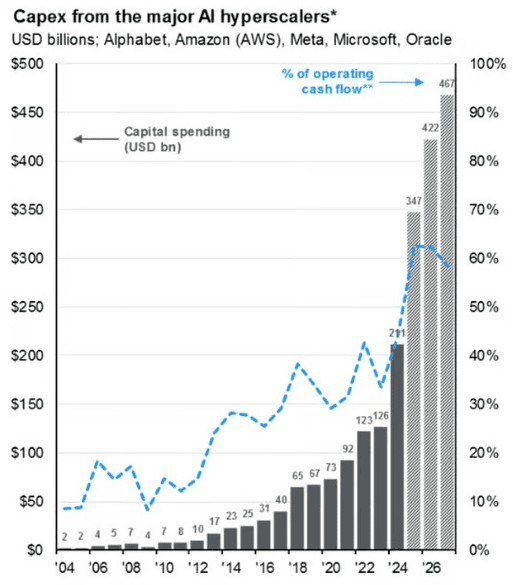

In consequence, the cashflow of leading tech companies that remains mindbogglingly massive is being spent on such infrastructure (capex) because they can afford to do so, yet their spending is still only around 50-60% of their free cashflow.

For the big AI players, capex focuses in areas such as building or upgrading massive data centers and buying powerful chips like GPUs. To satisfy the demand for data centers, Elon Musk plans to eventually produce solar-powered AI satellites on the moon. He says, "100 TW/year is possible from a lunar base producing solar-powered AI satellites locally, and accelerating them to escape velocity with a mass driver.” Perspective: 100 TW/year is roughly 29 times the entire global annual electricity consumption.

Indeed, the structural dynamics of markets have materially changed. Investors are increasingly pricing companies based on AI’s capability to disrupt entire industries, create new business models, and dominate future digital infrastructure rather than current earnings. This elevates growth, innovation, and market share over traditional profitability metrics.

AI’s transformative power depends on ecosystems involving big tech, innovative startups, cloud infrastructure, and data center operators, creating interlinked valuations and cooperative competition. This network-driven value creation greatly differs from product-centric valuations. This new era rewards companies heavily investing in AI technology and infrastructure, even at a financial loss initially, due to the anticipated paradigm shift in almost all sectors. Market volatility around valuation debates are natural as investors balance near-term profitability concerns with long-term growth.

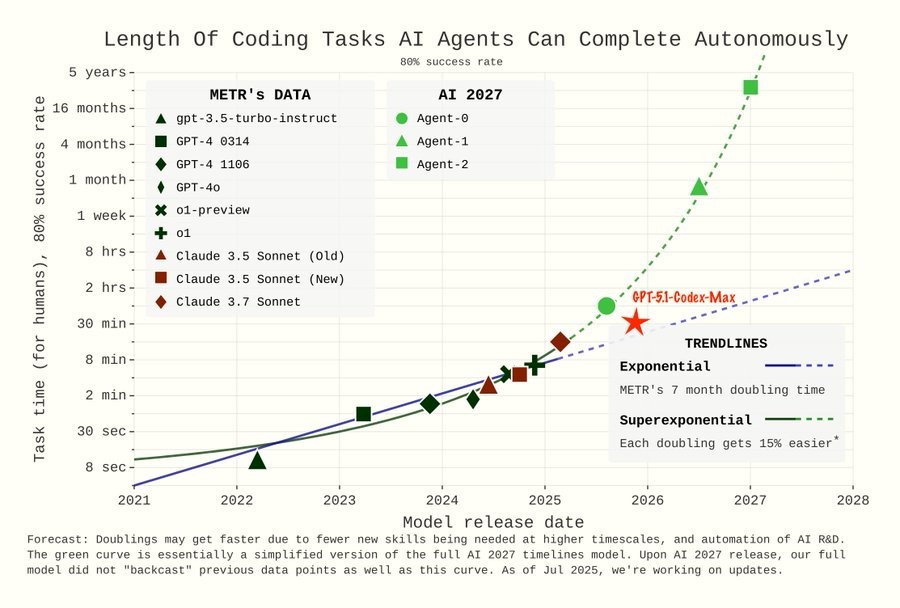

One last graphic on coding tasks is pretty insane. Reminder: It's a log plot. A straight line here already means exponential progress. Coding shows a parabolic line on a log plot. This says the growth is turning potentially superexponential.

Key points from the graphic:

The blue dashed line shows regular exponential progress, with a 7-month doubling time in the length of tasks completed.

The green curve shows "superexponential" progress: every doubling in task length becomes 15% easier, speeding up development.

Recent models (GPT-4, Claude variants, O1, etc.) and projections through 2027 (Agent-0/1/2) suggest that by 2027, AI agents could autonomously complete coding tasks that take humans up to 5 years.

A parabolic curve on a logarithmic scale means not just exponential acceleration, but an acceleration on top of acceleration—the progress is compounding and speeding up beyond even Moore's Law-type expectations.

This kind of superexponential trajectory in AI coding autonomy is rare in historical technology curves, reinforcing that the scale of acceleration could outpace past paradigms, with profound implications for productivity and software development.