Market Lab Report

by Dr. Chris Kacher

The Web3 Evolution Will Not Be Centralized™

Inflation?

The Fed will kick off a rate-cutting cycle with core PCE nowhere even close to the 2014-2019 norm. Core PCE came in 0.1% below estimates at 2.6% holding steady while the UMichigan 1 year expected inflation fell to 2.8%, the lowest since 2020. The market is betting this latest PCE is low enough to warrant a rate cut in September. This suggests that the Fed has chosen a new, higher inflation target.

Interest rate cut less important

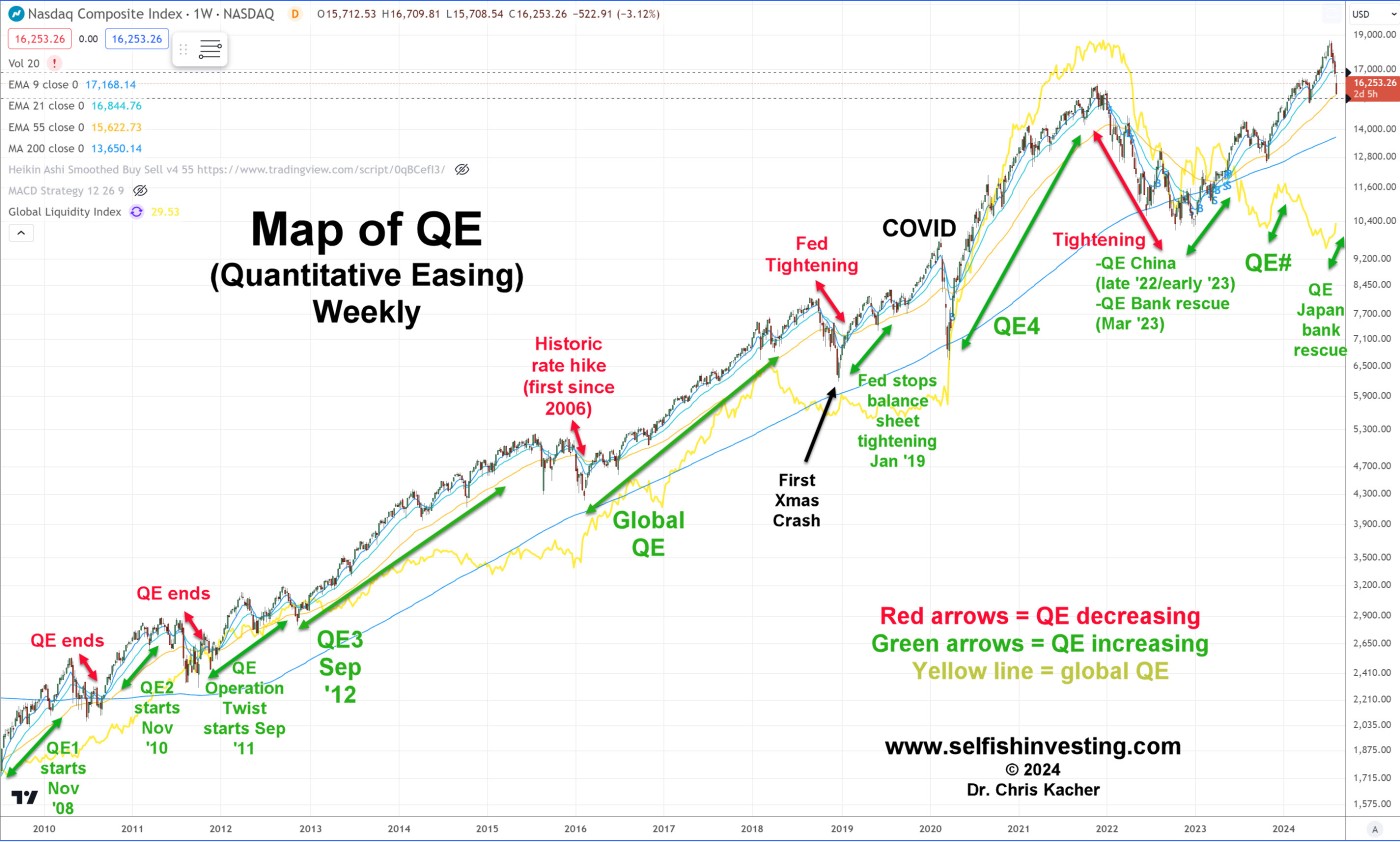

But interest rate cuts are less important that the net liquidity injections into money markets. Markets move in cycles which create the major trends. The cycles are driven by liquidity which can be measured from changes in the financial sector balance sheet. This in turn drives asset prices which are determined by the capacity of financial sector balance sheets, central bank injections of cash and by the price of government bonds, rather than by corporate profits and policy interest rates. This is why the rate of liquidity growth is key. As the rate slows as it did in 2018 and 2022, markets fell. Interest rates were kept steady for much of 2019 but markets rose because the rate of liquidity growth increased. We are witnessing similar effects today where rates have been kept steady at 5.25-5.50% since July 26, 2023 yet the major market averages have been trending higher overall since then.

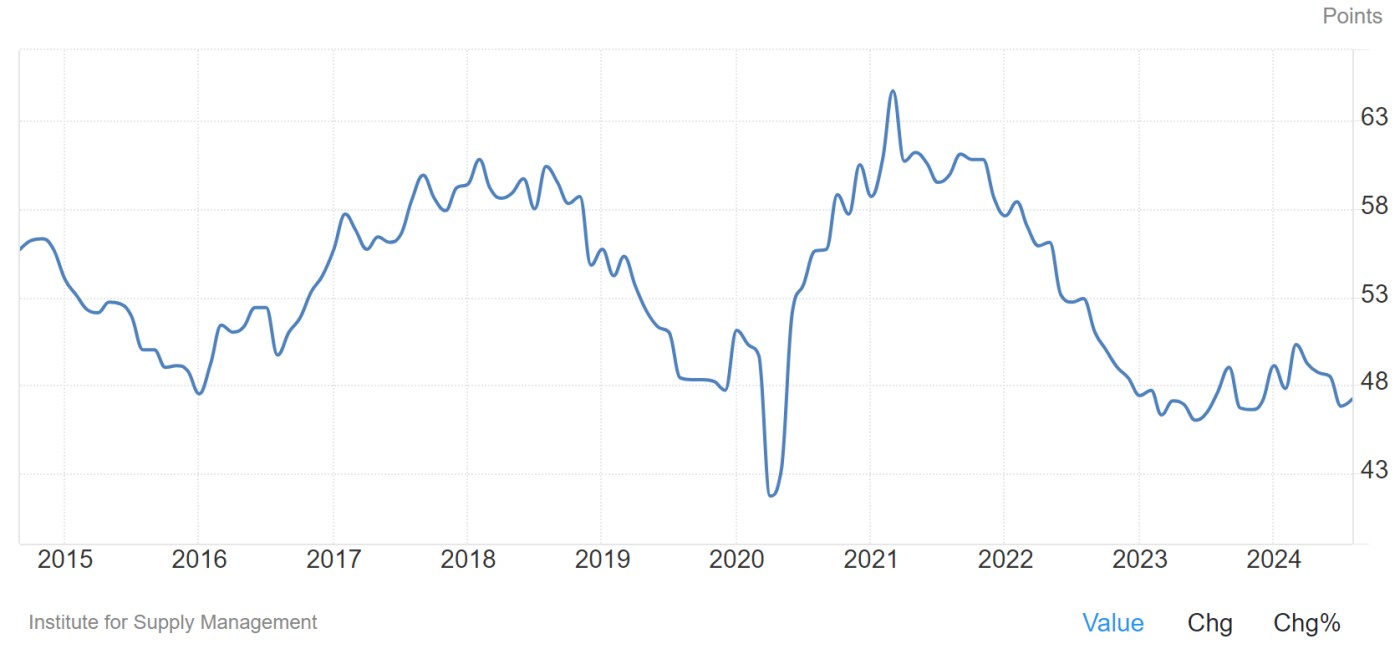

Institute for Supply Management’s (ISM) manufacturing PMI came in at 47.2 on Tuesday, slightly under 47.5 estimates, but up from 46.8 recorded in July. Under 50 is contraction which has been the case since late 2022 but while still in contraction territory, "US manufacturing activity contracted slower compared to last month," said Timothy R. Fiore, Chair of the Institute for Supply Management (ISM) Manufacturing Business Survey Committee, but demand continues to be weak. This was unsettling to markets which remain highly news driven thus sold off on Tuesday as fears of recession flared up.

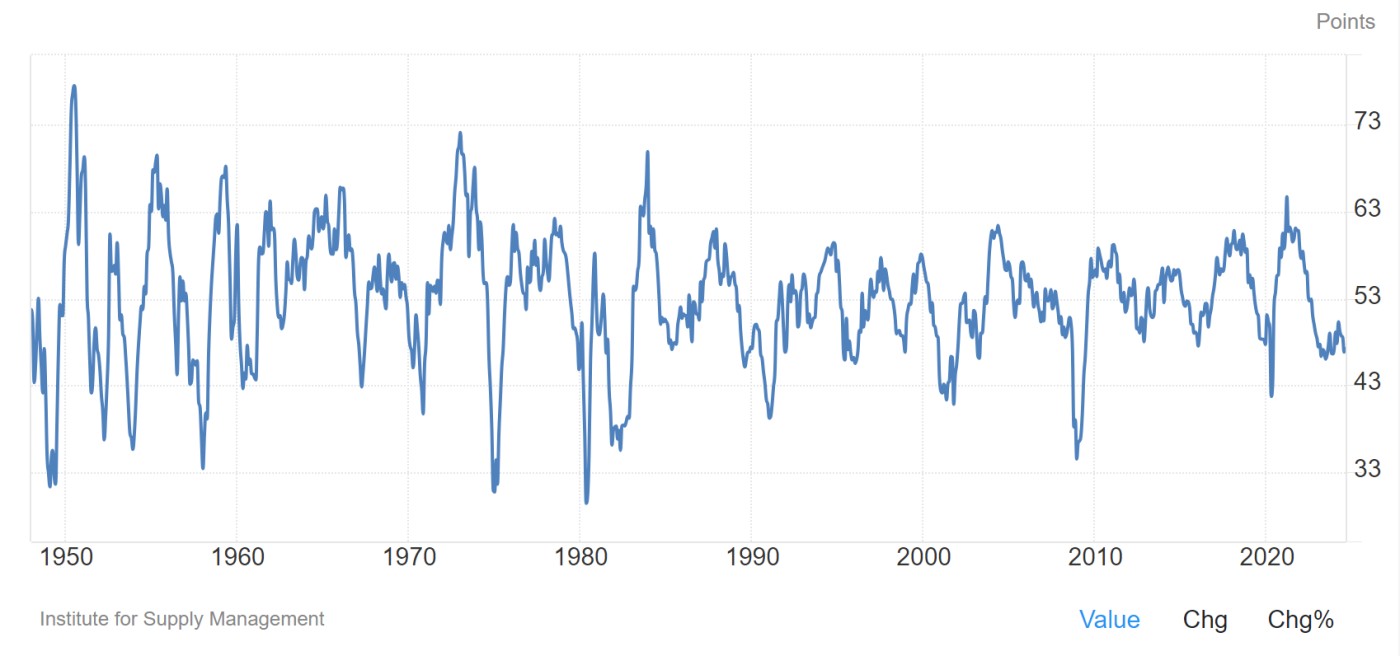

That said, except for a steep decline in the early 1950s, a drop below 43.5 has signalled a US recession every single time for seven decades, but we remain above this critical level.

Raoul Pal has studied the ISM in depth as it is a significant contributor to his riding the major market trends. He noticed that liquidity drives major cycles as well as helps to push the ISM higher, so believes that due to the accelerating levels of currency debasement triggered by fresh global liquidity, the ISM will trend higher. He is a macro investor so trades on major cycles aiming to catch major trends, not the wiggles.

That said, September has historically been a tough month for markets. Bond market volatility, possibly because of the US fiscal year-end, is typically high which can temporarily dent global liquidity. Nevertheless, the latest data shows global liquidity just hit US$176.8 trillion. It is now 17% up at an annualized rate over three-months so it is accelerating.

Lie after lie

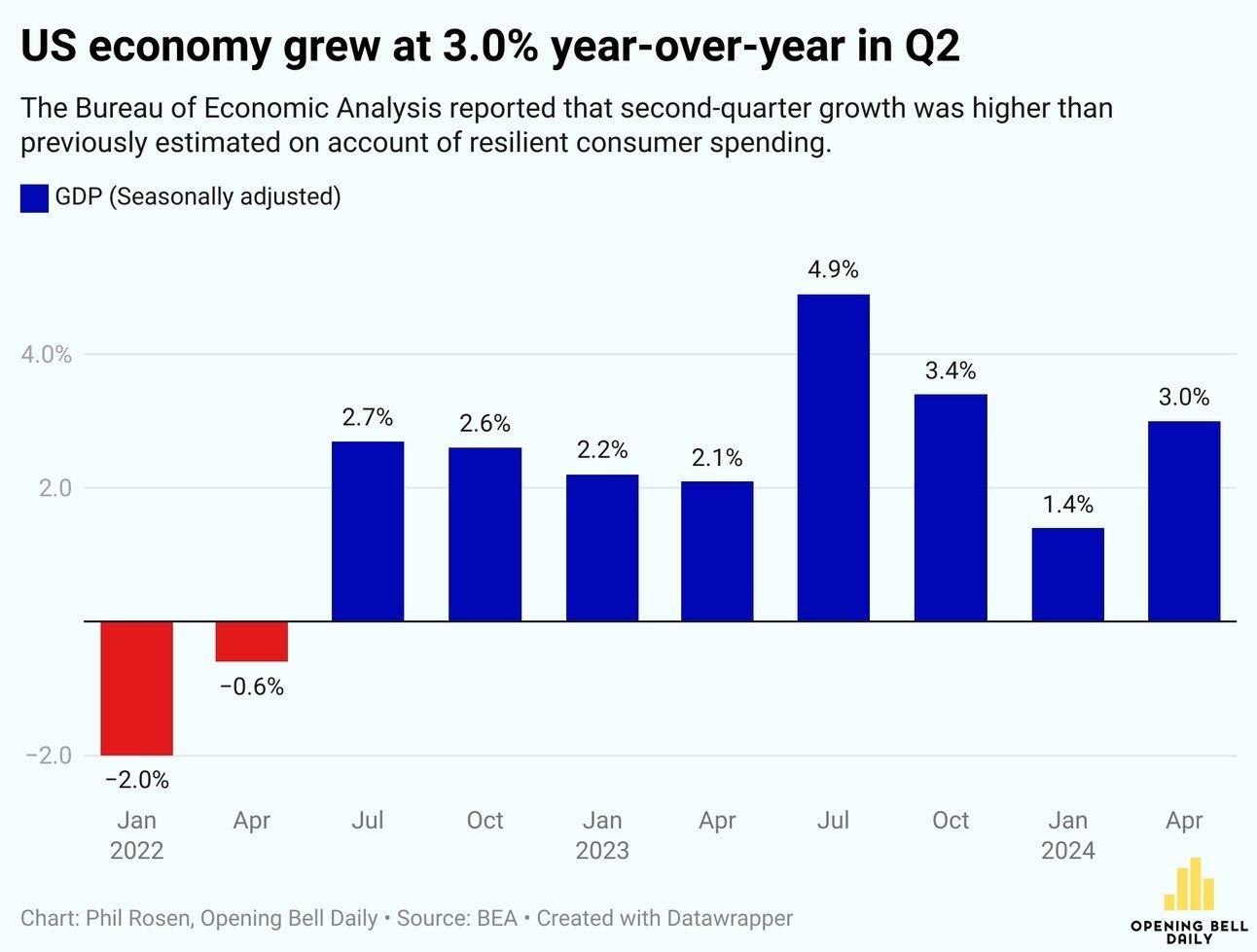

As for truth telling, we know numbers such as measures of inflation and growth are manipulated. The Bureau of Economic Analysis reported that US GDP rose at 3.0% annualized in the second quarter, revised from the previous estimate of 2.8%. According to the government, robust consumer spending contributed to the higher revision. The initial 2.3% print for consumer spending was revised higher to 2.9%. This suggests the vast majority who live paycheck-to-paycheck are digging themselves deeper into debt. Indeed, credit card debt is at all-time highs.

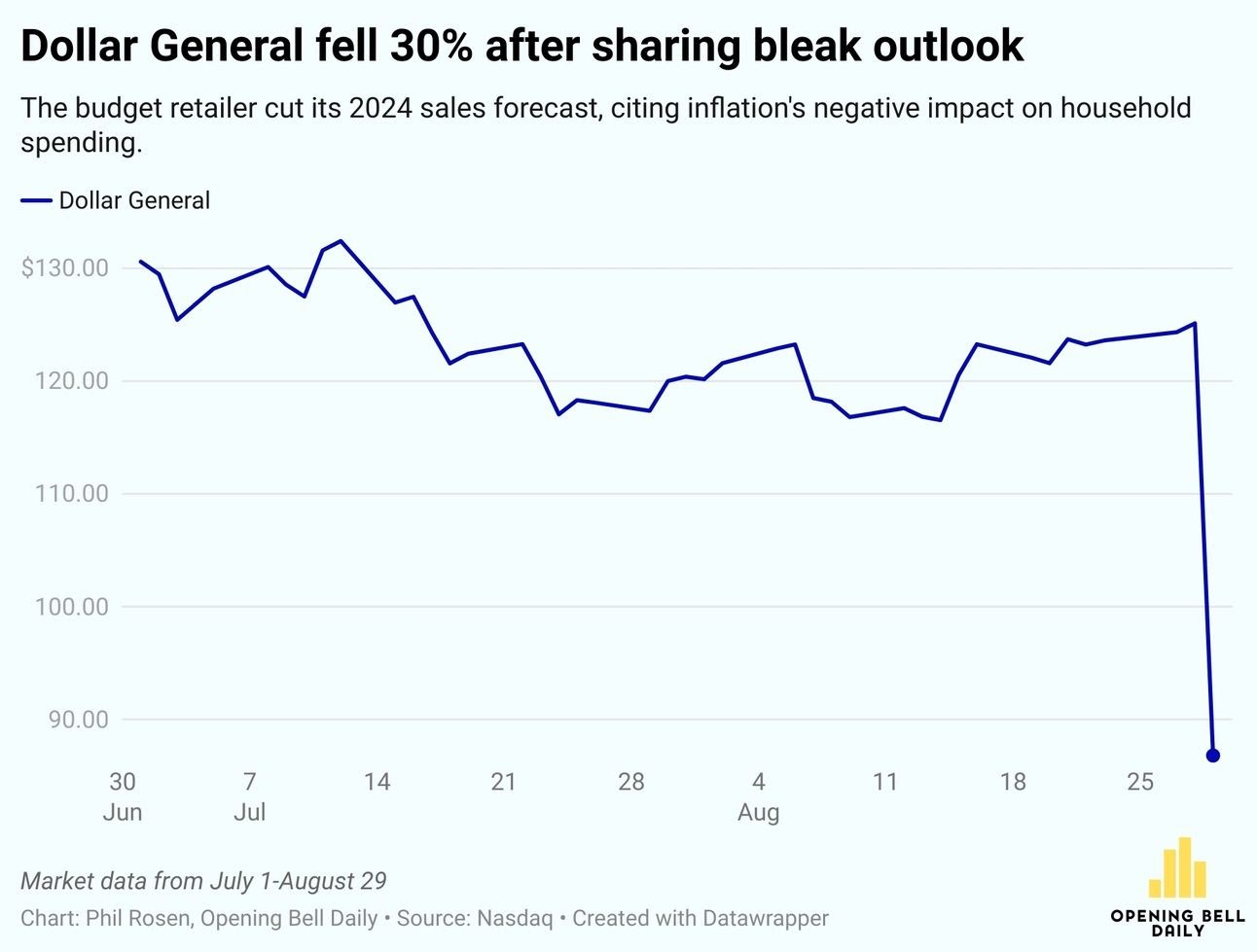

Despite the robust GDP print, Dollar General’s stock kicked off its worst day ever. Shares plunged 32% for its largest drop since its 2009 IPO. It highlights the disparity between the official and anecdotal, as well as public and private.

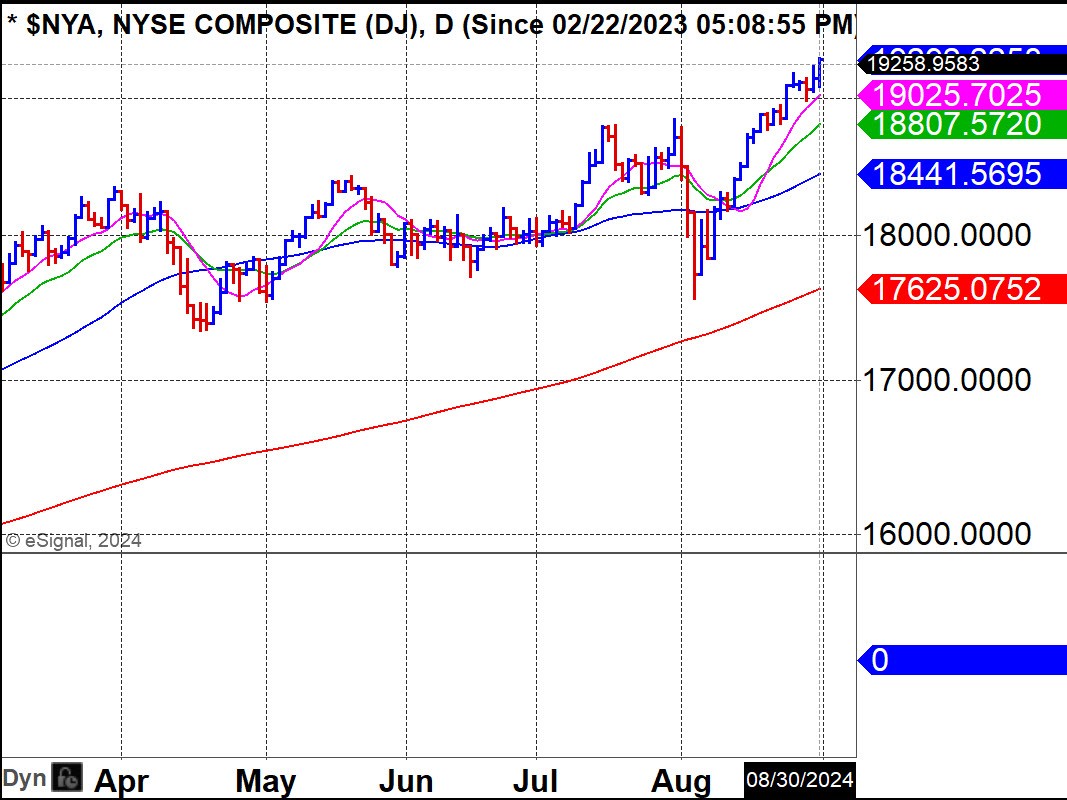

The official record paves lie after lie with its distorted numbers. Nevertheless, markets trade on the official data which is why major averages have been trading at or near all-time highs for most of this year. This is true even for the NYSE Composite which is recognized for its broad array of assets compared to other well-known indexes such as the S&P 500 which focus on fewer companies, are top heavy when it comes to big tech stocks, and offer less diversification.

But it doesn't take a rocket scientist to see that all is far from well when it comes to the average person. At least three-quarters of those in the US and UK live paycheck-to-paycheck. Most of the middle class has been destroyed. Many are now lower class, and many that started in the lower class rank now live in poverty or are homeless. Only a few, about 1 in 8 families, are now considered millionaires because the home they bought perhaps decades ago is now worth over $1 million. Indeed, the average home price in the US skyrocketed by 40% since COVID. This is a one-off event created by all the money printing since COVID. Of course, home price appreciation has accelerated around the world since QE was first launched in late 2008. Given the actions from Powell and Yellen, this form of liquidity is looking to accelerate due to the Japan yen carry trade debacle as well as ongoing liabilities including the ludicrous amount of debt interest.

Given the deep distortions in GDP and CPI, it is likely the US has been deep in recession territory over the last few quarters. But the Fed pretends once again just as they did when they tried to paint a false picture that inflation was transitory prior to launching the fastest rate hikes in history in 2022.

All that said, price/volume charts are where the rubber meets the road which is always our focus. The macro picture provides an important backdrop so when markets selloff, one can start looking for buy spots as long as global liquidity/QE remain strong. In every case since QE was launched in late 2008, major market averages had brief corrections then would shoot to new highs as long as the rate of liquidity from QE in all its forms, global and otherwise, was increasing. Each time the rate of liquidity paused or slowed, markets corrected.