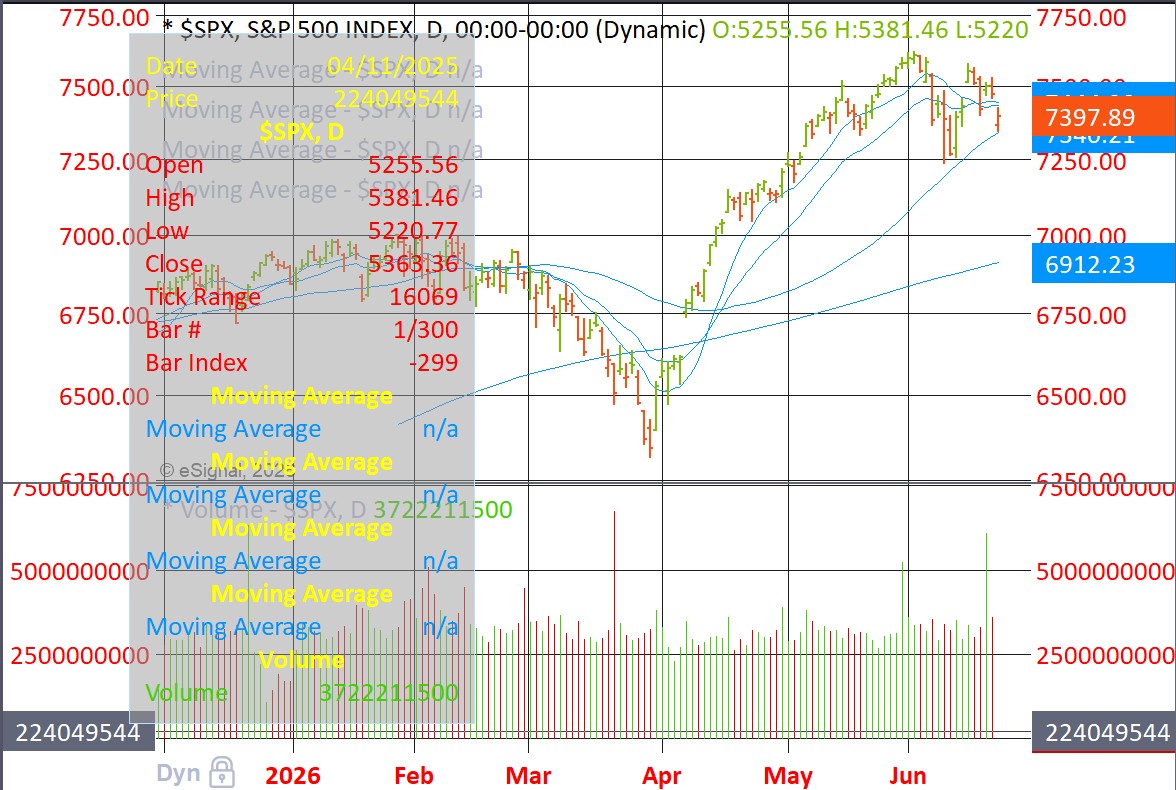

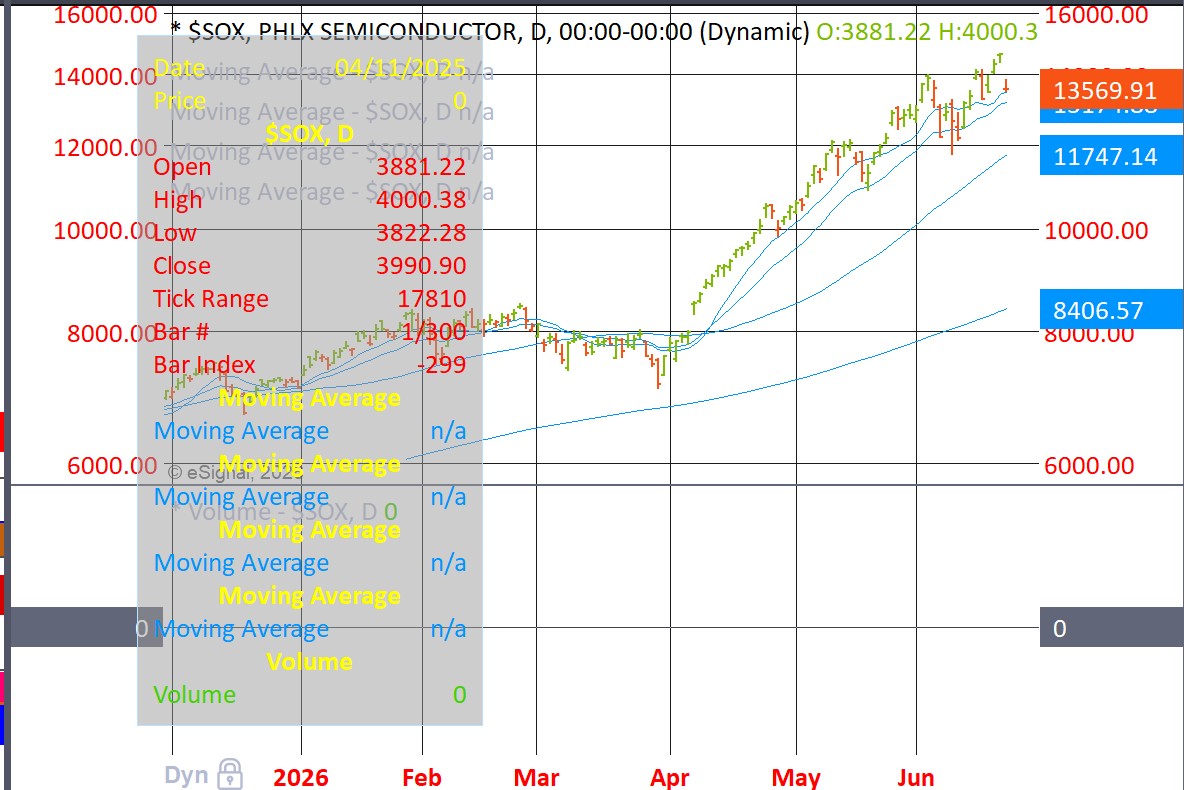

MU (Micron) reports tomorrow after the close. Odds favor a strong report which could stabilize semiconductors. That said, semiconductors are notably weak today (Tuesday, June 23, 2026)**, with the **PHLX Semiconductor Index (SOX)** down around **5.4%** intraday — a sharp session amid a broader tech-led selloff.

### Primary Drivers Today

- **Heavy selling in Korean memory giants spilling over globally**: SK Hynix and Samsung (key HBM/DRAM players) dropped **10-12%+** in South Korea, contributing to a ~10% plunge in the Kospi index. This memory-specific pressure is rippling to U.S. names (MU, SNDK, and the broader group) due to shared AI supply chain exposure.

- **Ongoing rotation and profit-taking**: Investors continue rotating out of extended, high-valuation AI/tech/semiconductor names into small-caps, value, or defensive sectors. The sector's parabolic run (massive gains YTD) left it vulnerable to digestion.

- **Pre-Micron earnings caution**: MU reports after the close tomorrow (June 24). Sky-high expectations around HBM pricing, supply, and AI demand create an overhang — many traders are de-risking ahead of the print rather than buying the dip.

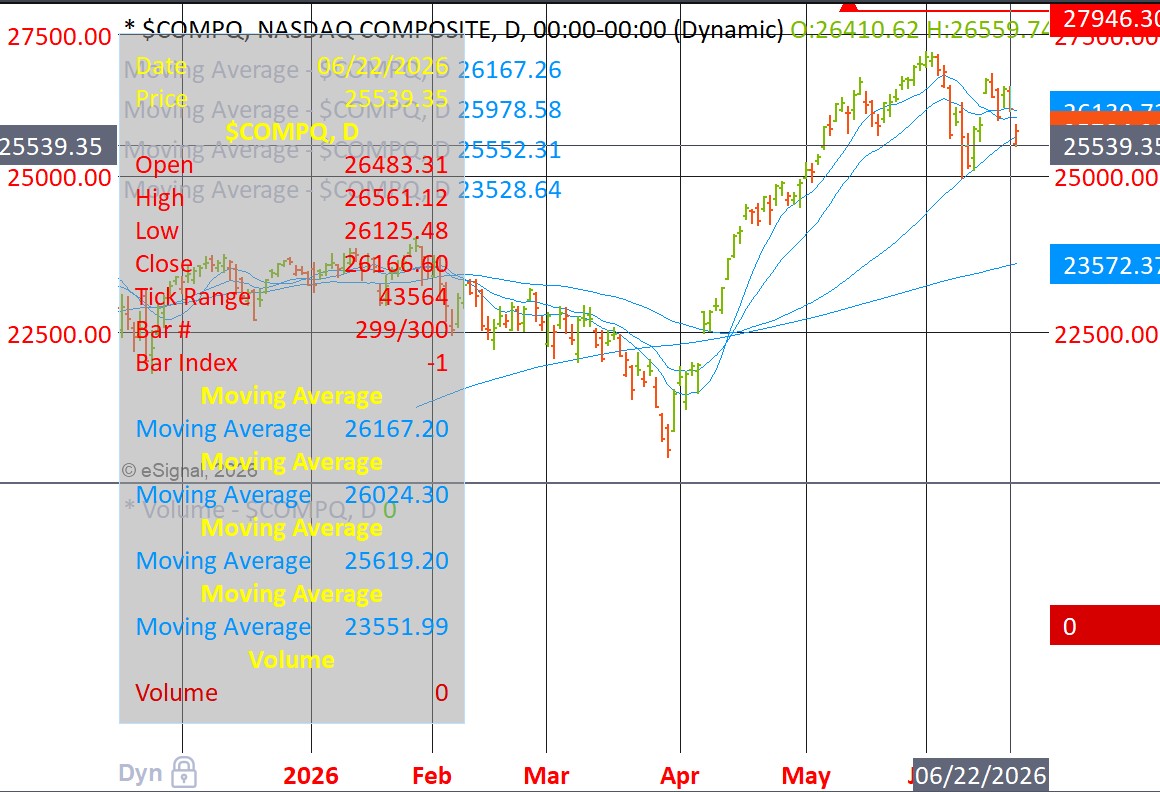

- **Broader tech momentum**: Continuation from Monday's weakness (hyperscaler capex/dilution fears, talent news at Google, SpaceX multi-day slide). No single new macro shock, but light volume and positioning ahead of PCE inflation data amplify the move.

### Context

This is **sentiment-driven digestion** in a concentrated AI cycle — not a fundamental breakdown. AI memory demand remains strong (HBM largely sold out), but questions around pacing, valuations, and potential supply signals are triggering selective selling. Memory plays (pure NAND/DRAM) like SNDK and MU have been especially volatile.

A strong MU beat + bullish guidance tomorrow could stabilize or reverse parts of the sector; any caution could extend the weakness short-term.

This fits the pattern we've discussed: periodic pullbacks in an otherwise transformative but extended trend.