Market Lab Report

by Dr. Chris Kacher

The Web3 Evolution Will Not Be Centralized™

Markets

The CBOE total put/call ratio spiked last week, sentiment has been notably bearish for both retail and institutional investors as discussed in our recent VoSI Focus List Review, and liquidity has been on the rise in both China and in the US. Further, long bond yields and the dollar have been soaring so the short-term pullback in both we are seeing is not surprising. In consequence, markets had a relief rally last Friday spurred in part by short covering. Friday's volume was greater than the prior day on both the NASDAQ Composite and S&P 500. Nothing goes down in a straight line so as we had been saying, the current bounce is no surprise in the major averages. Depending on the magnitude and length of the bounce, new short selling opportunities in stocks and cryptocurrencies could emerge.

The PPI came in hot at 0.5% vs. est 0.3% MoM and 2.2% vs. est 1.6% YoY. As we have been saying, sticky inflation remains an issue. Some Fed members don't think their 2% rate of inflation target will be hit until sometime in 2025. That's problematic since it implies rates will be kept at elevated levels for a prolonged period of time. We have already seen some institutions deeply impaired from high rates. Regional banks were one area where some collapsed like a house of cards. Pensions and IRAs could be next.

Interest rates

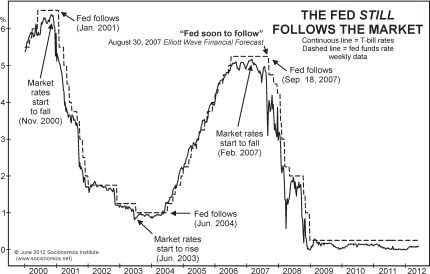

The Fed follows T-bill rates of interest, so expect aggressive rate cuts sometime in late 2024 as recession could be expected to hit by then but of course this depends on how fast the economy slows.

With recession, inflation will naturally fall as well thus the Fed's 2% mandate would likely be hit during such time. Wild cards are the gig economy which creates many part-time jobs as well as exponentially growing technologies such as generative AI which could add to GDP thus postpone recession for longer than expected.

Last Friday's jobs report showed a surprising print of 336,000 new jobs in the prior month but this was because 1.127 million part-time jobs were added while 850,000 full-time jobs were lost. A strong jobs report gave belief the economy will remain strong. But this strength is somewhat illusory because part-time jobs should not be equal to full-time jobs despite being counted as such in the unemployment figure. Note that the unemployment figure is further tainted because workers who have given up actively seeking a job are not counted in the unemployment rates, nor are freelancers or gig workers who recently lost clients. Even with all of this, the unemployment rate came in 0.1% above expectations at 3.8%. This could be the start of higher unemployment figures to come. Nevertheless, because the economy appears to be resilient based on the doctored data, some Fed members think the 2% target won't be hit until sometime in 2025.

Arthur Hayes points out the importance of focusing on real rates in comparison to the rapid growth of the US economy, rather than obsessing over nominal Fed rates. The real yield is the yield on US treasuries minus inflation. He says that due to significant government spending and robust GDP growth, real yields on government bonds have turned negative which is bullish for Bitcoin. But with yields soaring as of late, real yields have risen which should be bearish for Bitcoin and explains its hesitant uptrend over the last few weeks as shown in the chart below.

That said, the short-term bullish case for stocks and Bitcoin as cited above has been the recent boost in liquidity and a potential bounce from oversold or overbought levels, depending on the instrument. This has enabled the major averages and Bitcoin to stand relatively strong in the face of higher bond yields and a stronger dollar. But this uptrend in liquidity may be coming to an end as PBoC Liquidity Injections may be diminishing (yellow bars at the bottom).

Further, the Fed is nearing the end of its hiking cycle but where inflation heads is less certain. If inflation continues to fall, the Fed is still likely to keep rates at current levels for a prolonged period. 2% is still far off. In such a case, the real yield would rise which is bearish for stocks and crypto. Further, once the real yield starts to fall due to the Fed pivoting and lowering rates, history suggests this is the start of a more significant market correction because the economy has weakened to the point that forces the Fed to lower rates. The Fed follows the T-bill market which, during times when T-bill rates nosedive, creates nasty bear markets such as in 1930-32, the 1970s, and 2000-02. With debt still near all-time highs despite rising rates, persistently high rates of inflation in food, some commodities, as well as in regulatorily captured industries such as healthcare and education, expect a hard landing at best.

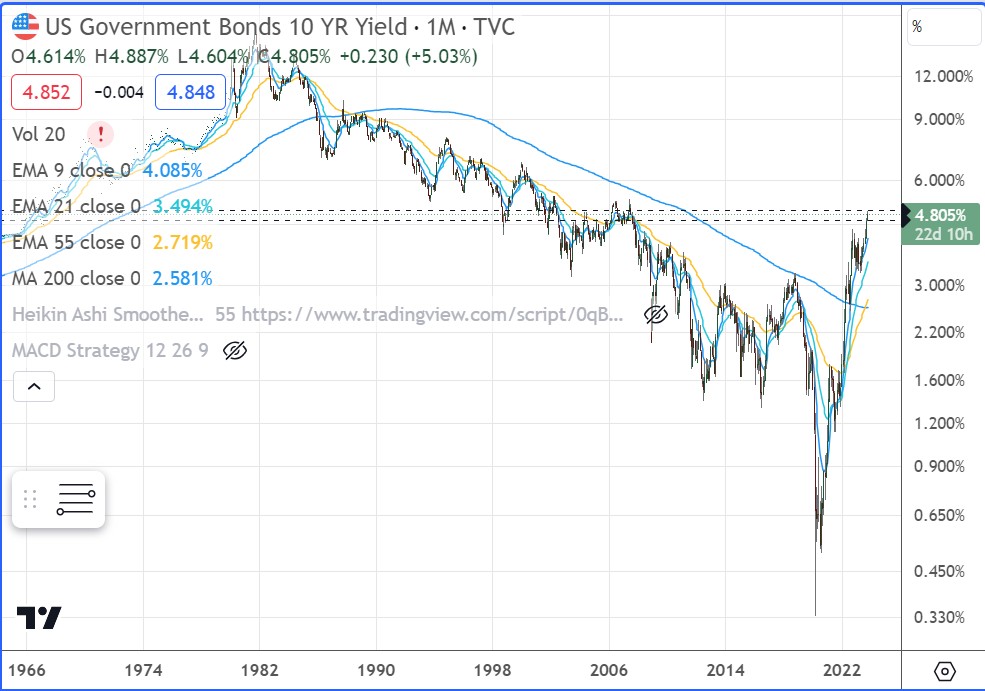

Long bond yields remain on an overall sharp rise. This was the fastest rate hike in history from record low interest rates. The exponential y-axis underscores how rate hikes when rates are low are far more impactful than when rates are already high as they were in the late 1970s. Further, the increase in rates in the late 1970s to the early 80s to record levels occurred when the US had far less debt so interest payments were not onerous. Today, the US does not have that luxury.

Long bond yields remain on an overall sharp rise. This was the fastest rate hike in history from record low interest rates. The exponential y-axis underscores how rate hikes when rates are low are far more impactful than when rates are already high as they were in the late 1970s. Further, the increase in rates in the late 1970s to the early 80s to record levels occurred when the US had far less debt so interest payments were not onerous. Today, the US does not have that luxury.

Moreover, Ray Dalio cites how geopolitical tensions, social unrest, and civil wars bring us closer to another black swan as we are in the eleventh hour of the long term debt cycle. In consequence, this would create more supply chain disruptions which would push inflation even higher. This would make the job of the Fed harder as they may be forced to at least keep rates elevated for longer to contain inflation.