**A More Balanced Market**

The AI bull market is unfolding with a textbook list of narrative violations.

In 2026, the losers are winning and the former darlings are getting punished. After years of extreme concentration, this reversal isn’t a warning sign — it’s one of the more reassuring developments we’ve seen for the longevity of the bull market.

Small-caps are outperforming large-caps. The equal-weight S&P 500 is beating the cap-weighted index. And the S&P 493 are running circles around the Magnificent 7 year-to-date.

This is a direct unwind of the narrow leadership trade that dominated the last three years. Mega-cap tech is no longer carrying the market — it’s actually dragging it. That’s healthy.

Look at these YTD numbers that would have sounded insane six months ago:

- Russell 2000: +22%

- Equal-weight S&P 500: +10.7%

- S&P 493: +13.7%

- Magnificent 7: -6%

Even more telling: small-caps are trading near 20x earnings while the S&P 500 sits at 26x. The market is finally rewarding valuation instead of momentum and size. That’s a regime shift.

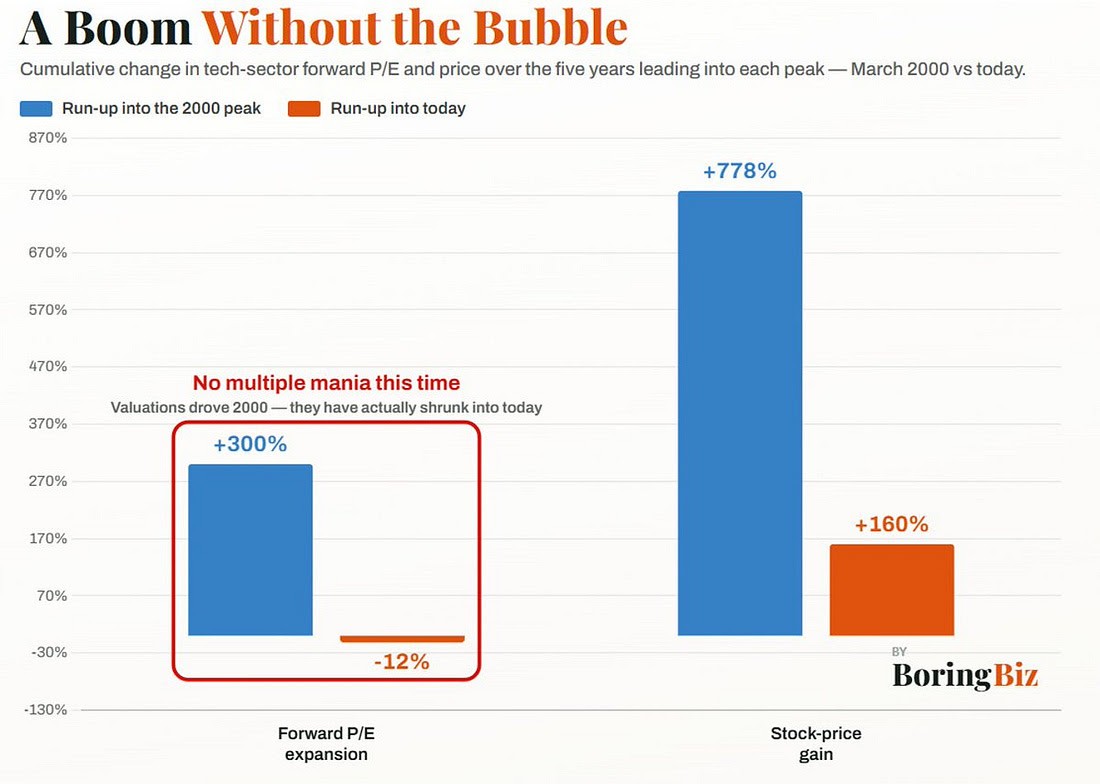

Nevertheless, a lot of people continue to compare the AI cycle with the dot-com bubble, without realizing that the run-up has been driven by fundamental earnings growth, while the 2000s was mostly just hopes and dreams.

Forward P/E multiples in tech have contracted even as stock prices have gone up this time around compared to the run-up into the year 2000 where P/E multiples expanded by 300%. The change in price over the five years leading into the March 2000 peak 778% gains vs. gains today of 160% so far.

Further, the S&P 500 advance-decline line just hit an all-time high — even as the cap-weighted index had a losing week. Breadth is leading price. In macro terms, that’s the kind of internal improvement that tends to extend cycles, not end them.

From a bigger picture standpoint, this makes sense. After years of massive liquidity injections and zero-rate policy that disproportionately benefited the largest, most visible growth names, we’re now in a period where capital is rotating toward more normal valuations and broader participation. The Fed’s higher-for-longer stance (whether they admit it or not) is exposing the weakest parts of the old leadership while giving oxygen to neglected areas of the market.

Bottom line: Today’s setup is far less top-heavy than it was a year ago. Bull markets rarely die from becoming *less* concentrated — they usually die from the opposite.

So while the hot chip stocks like Micron and Sandisk grab the headlines, the rest of the market is doing the real work: catching up on valuation, improving breadth, and letting the former leaders consolidate.

If it still walks like a bull and talks like a bull… the cycle probably has more room to run. But if it is a defensive move that leads to further correction due to bottlenecks, capex guidance getting cut or slowed dramatically, or data centers that can’t get enough reliable power due to grid delays, regulatory blocks, or skyrocketing electricity costs, then profit margins would contract leading to further downside.

**The Electricity Lag: Why AI’s Real Impact Is Still Years Away**

AI is exploding, yet it still makes up just 0.42% of GDP. Research historiam Azeem Azhar is right — the real economic payoff comes later and much bigger than the early numbers show.

History agrees.

Electricity started transforming factories in the 1880s–1890s. But it barely registered in productivity and GDP data for **40 to 50 years**. The full boom didn’t hit until the 1930s–1940s, after grids were built, factories were redesigned, and old capital was scrapped.

We’re in that same messy stage with AI right now.

The hype is loud. The capex is massive. The narrative is everywhere. But the broad productivity gains that actually move the economy are still ahead — probably deep into the 2030s. That's why Elon Musk's prediction of supply-side delfation within the next year or two is probably too optimistic. That said, AI isn’t just another technology — it can accelerate the development of other technologies (robotics, energy, manufacturing). This feedback loop could shorten the historical lag dramatically. Also, cost curves in solar, batteries, computing power, and certain AI applications are falling fast. If these spill over into broader goods and services quicker than expected, supply-side deflation could surprise to the upside.

At any rate, the current rotation out of the Mag 7 into small-caps and value stocks is healthy. Markets are finally pricing in a longer, broader cycle instead of just worshipping the usual suspects.

Bottom line: Real technological revolutions don’t show up neatly in the numbers on Wall Street’s schedule. They take time.

The electricity lag is a brutal but useful reminder: patience usually beats hype in these cycles.