by Dr. Chris Kacher

Bond and stock prices are shrugging off the bond downgrade as they attempt to push higher. This is in sharp contrast to the last two downgrades where markets immediately fell precipitously in the ensuing days. On a risk basis, the model went to a sell signal just in case, but it appears the dust from any bond downgrade fallout has settled for now. Of course, bonds remain vulnerable due to other factors that we have discussed that have been present for many months thus yields on the long end remain elevated.

A Raymond James analyst said, “While the Moody’s decision could provide a fresh catalyst for another leg higher in rates as investors have become increasingly nervous about US policy more broadly, we think the bond market has been pricing in the deteriorating fiscal outlook for some time now. That is a key reason why longer-maturity yields have been rising despite weakening growth prospects.”Meanwhile on Wednesday, the 20-year Treasury notes auction saw weak demand which pushed the price of bonds and stocks lower with the yield on the 30-year hitting highs not seen since Oct-2023.

But because the Fed must keep rates lower on the long end of the yield curve due to $10 trillion in refinancing by July, the QE print machine remains alive and well which tends to push markets higher. This is why Powell talks out of the both sides of his mouth when he cites government deficits as a problem but then continues to accommodate spending by keeping yields at a politically acceptable low level due to the Fed running a printing press to suppress 10-year yields. These measures will provide printed money through various channels to replace any foreign capital that leaves as a consequence of capital controls which are designed to rebalance American trade. Global liquidity will thus continue to rise at a brisk pace, lifting markets. Markets climb that worry wall.

Meanwhile, the economy and jobs are sufficiently managing, the China tariff deal seems adequate, and the Trump administration stressed that so much waste occurred under Biden so plans to deal the issue head on to shore up the creditworthiness of US long bonds, though under Trump's first administration, the money printing did not slow but continued at a similar pace.

Trump’s tariffs aim to dismantle the Belton Road Initiative which expanded China's influence through infrastructure loans and trade partnerships. Instead, Trump's tariffs plan to make US markets less accessible to Chinese goods, forcing a rebalancing of global economic power. If successful, this is ultimately favorable to the US.

Fed's tools at the ready

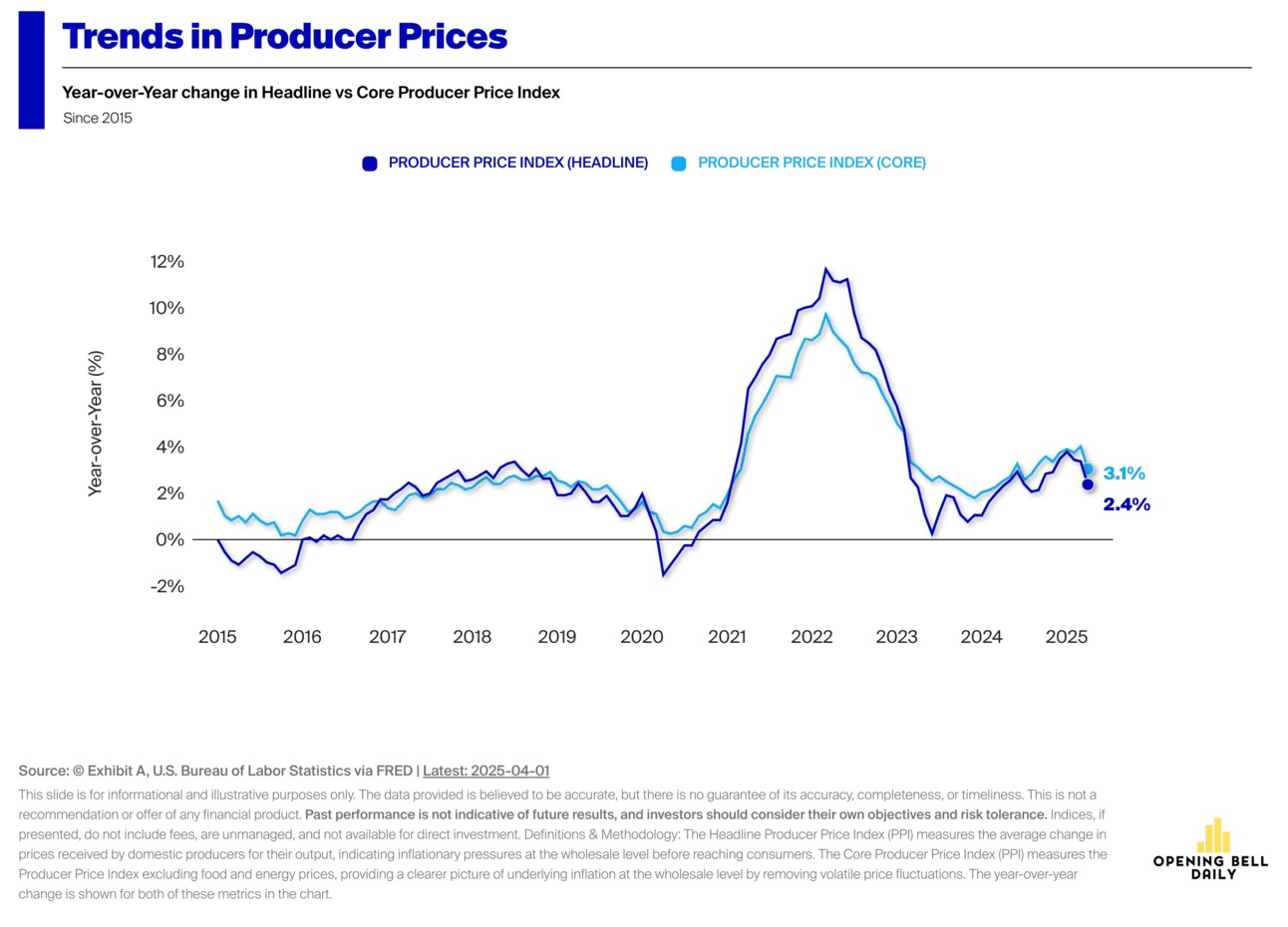

Despite lower CPI and PPI data that came in below estimates, trade deals being made, and economic uncertainty, the 30Y bond yield is back around 5%. The US bond downgrade and the weak 20-year bond auction spurred this rise in yield. But stocks are still showing resilience despite this downgrade compared to the prior two downgrades where markets immediately fell precipitously in the ensuing days.

Powell will nevertheless continue to maintain his higher for longer view on rates. This could spark deeper concern in Trump and Bessent, but the Fed has many tools in its toolbox. The Fed is already doing what Trump and Bessent require behind the scenes. The Fed can stop QT on both mortgage-backed securities (MBS) and treasuries. They can restart QE for both MBS and treasuries which will boost housing prices because mortgage rates will fall. They can exempt MBS and treasuries from the supplemental leverage ratio (SLR). At the same time, the Treasury can increase the amount of treasury buybacks each quarter while continuing to issue a large amount of bills (<1yr maturity) over bonds (>10yr maturity).

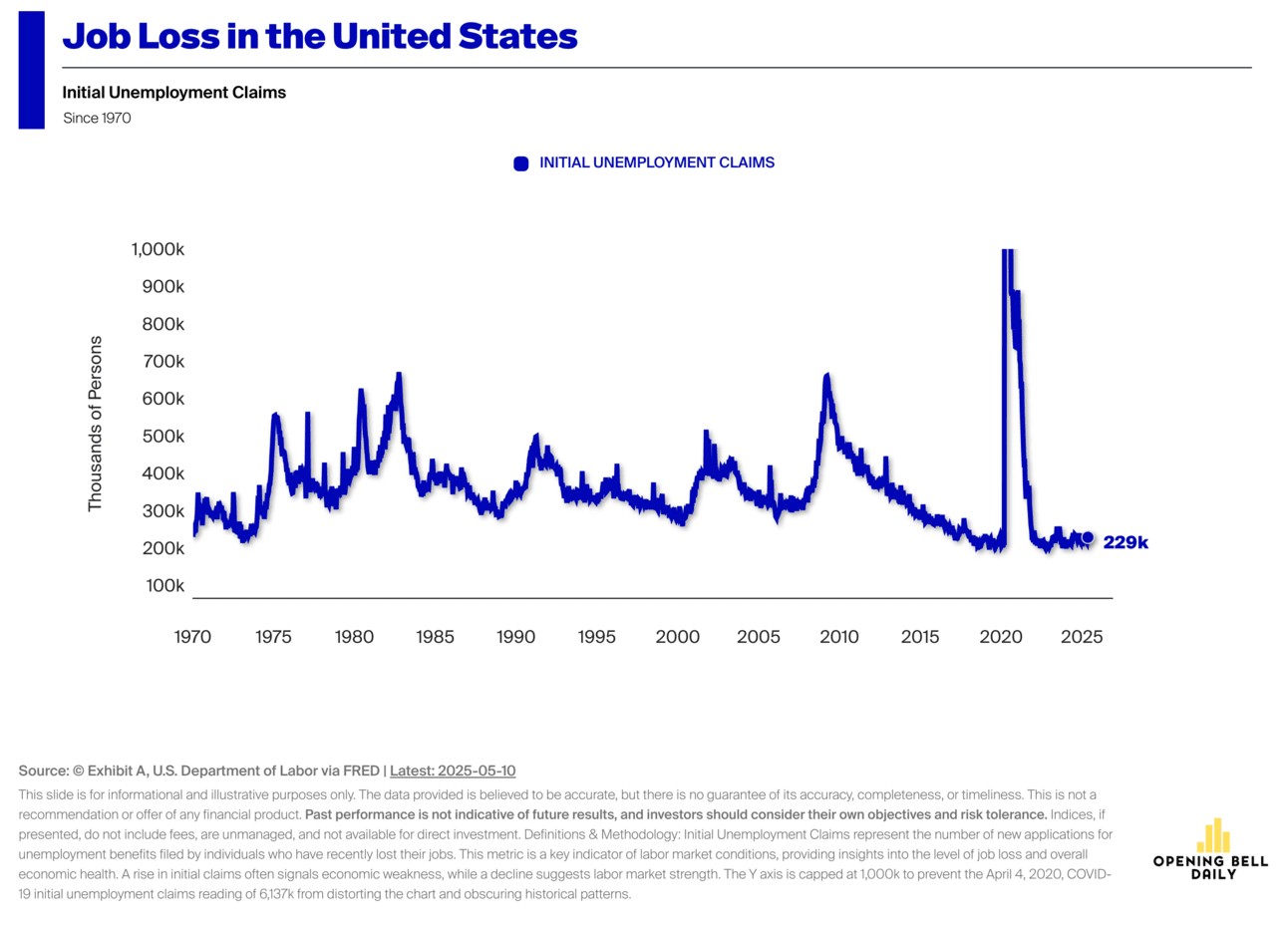

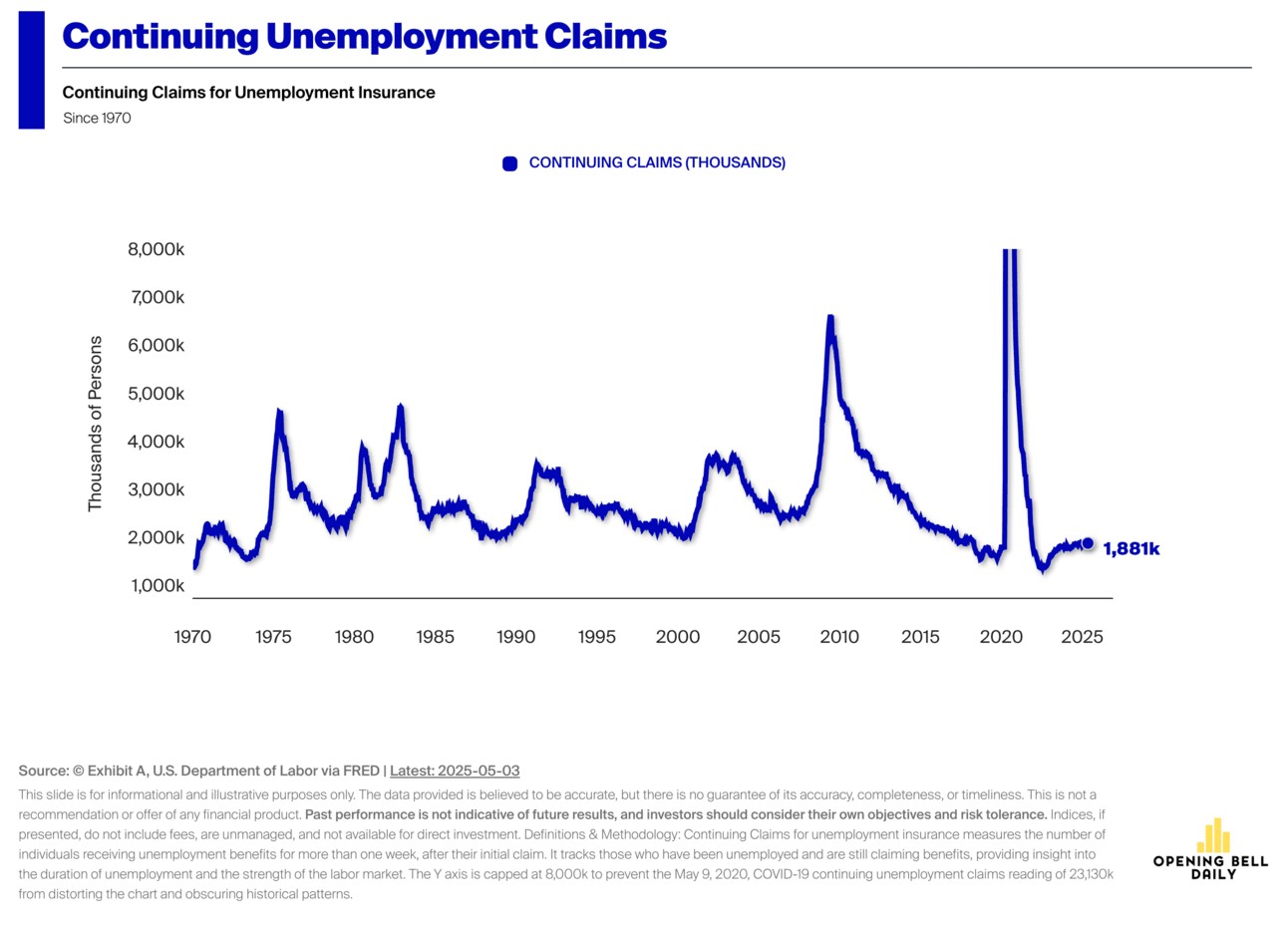

Meanwhile, the latest jobless claims data for the week ending May 10 showed no material uptick in either initial or continuing claims, suggesting layoffs remain low and employment is stable.