Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

Bringing Billions to Blockchain via Quantum Poodles™

A Nice Pair

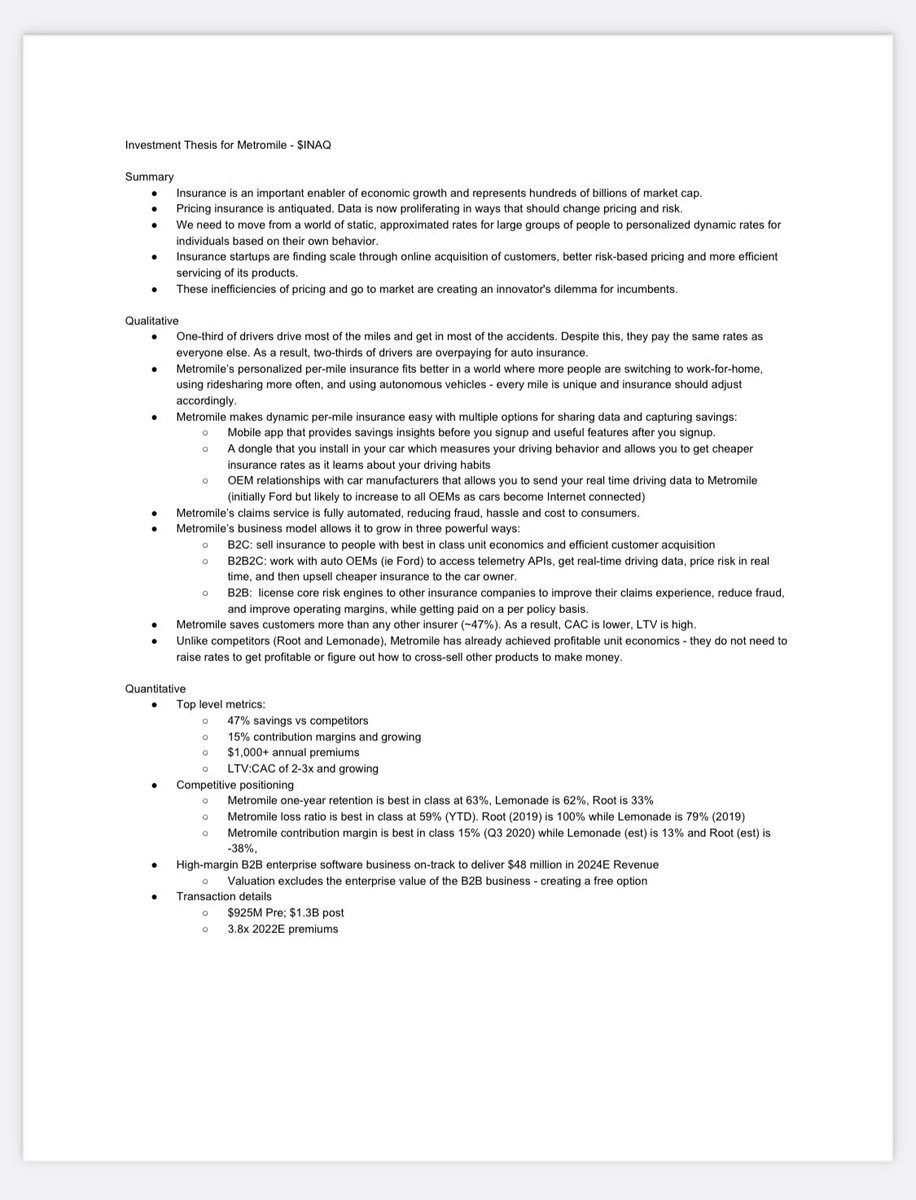

Billionaire entrepreneur Chamath Palihapitiya who has the golden touch when it comes to startups just launched INAQ which disrupts car insurance. Watch for buyable gap ups and low risk pocket pivots. It is a small company at present, valued at around $350 million, so assume elevated volatility.

Its one-pager:

He is also behind the merger between MP Materials (ticker: MP) and FVAC. The merger creates the largest source of rare earth metals outside of China. Rare earths are a critical input into critical climate change and battery technologies. MP has received multiple grants from the DoD so they can start making and refining magnets. The U.S. will not allow China to monopolize the rare earths market, so they will be highly supportive of MP, perhaps 9-figure grants in the coming months. MP's net income increased 4.2x YoY to $14.6 M while adjusted EBITDA grew 159% YoY to $11.6 M. MP has gapped higher pushing it to the upper range of small cap but due to its smaller size remains volatile. Handle with care.

The Cryptofront

The race to adopt bitcoin among institutions has begun. They are slowly starting to realize bitcoin will eventually reach new highs far higher than old highs so the new waves of buying pressure are on their way. This does not mean bitcoin will go up in a straight line but when it drops in price, there is more pressure to buy.

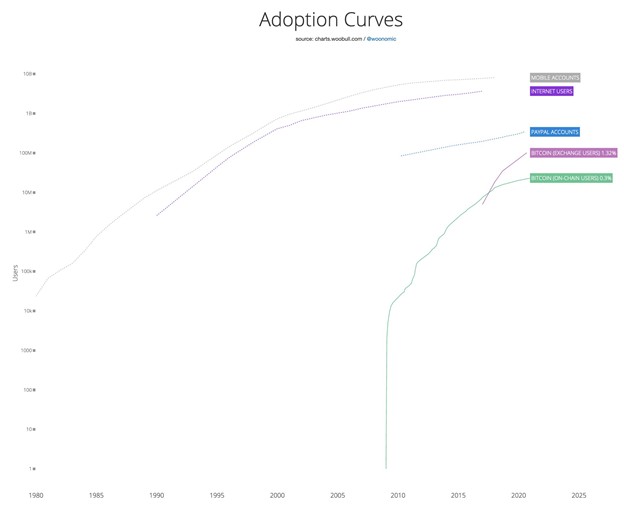

In recent cryptospace news, the S&P will launch cryptocurrency indices. We also have an adoption curve for bitcoin that well outpaces any other technology before it.

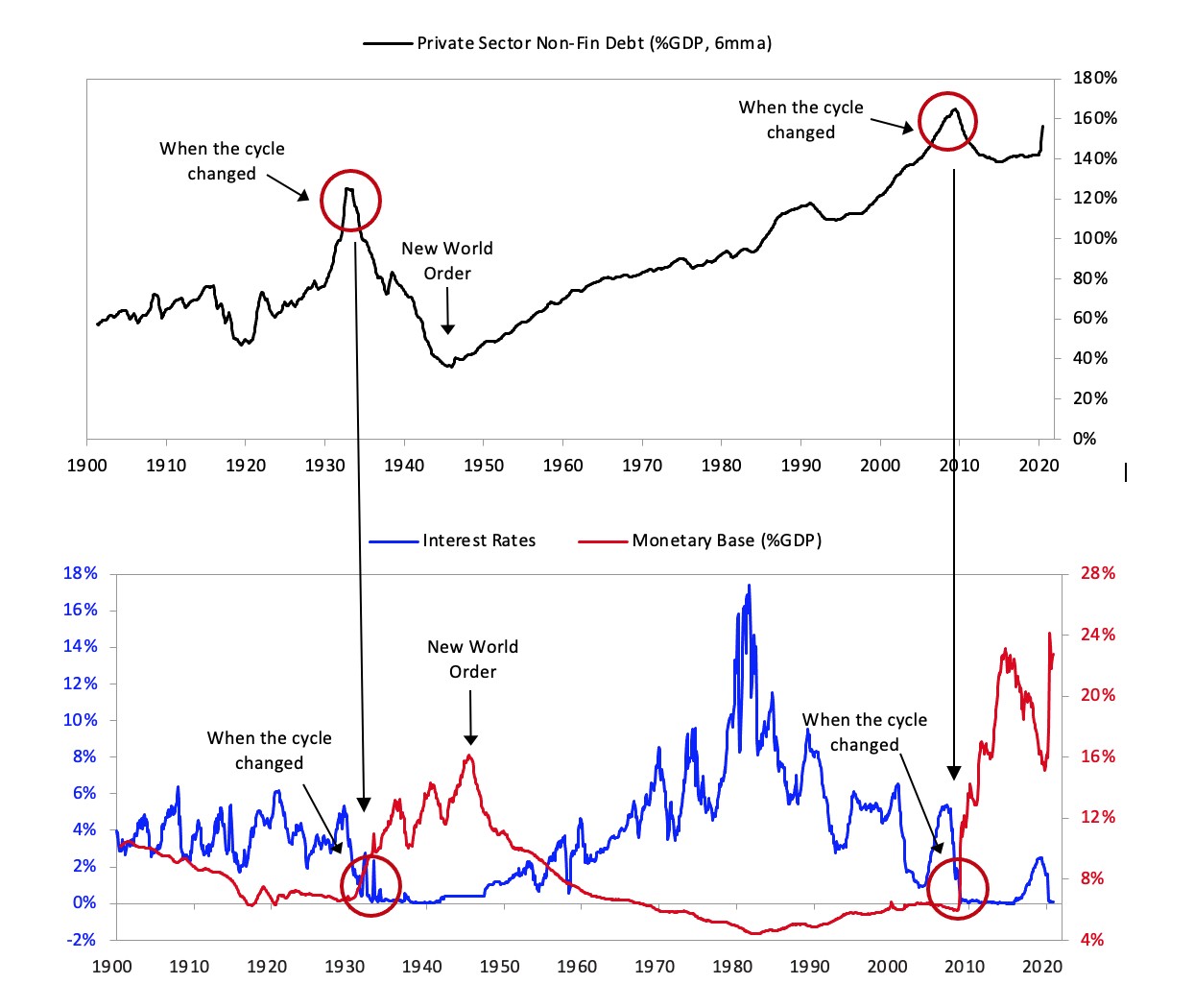

The world is on the tipping point of a major transformation. In the cycle change of the 1930s when the world sank deeply into debt and record low interest rates, it only took 13 years to reach a new world order culminating at the end of World War II. So far, this cycle change has run 12 years since the financial collapse of 2008. If the wealth created by technologies experiencing exponential growth is sufficient, the historically repetitive norm of revolution and global war can be averted.

Why ETHE is a Top Risk/Reward

Such technologies include first and foremost ETH and BTC. BTC recently hit new all-time highs. Going forward, ETH may outperform BTC if history is any guide. This suggests Grayscale ETN ETHE may outperform GBTC. If Bitcoin is the collateral, Ethereum is like a decentralized version of bonds. The biggest problem central banks are trying to solve is the crashing velocity of money which stands at 1. QE is not solving this issue. The QE road is a mobius strip which explains why the can gets kicked down a seemingly endless road. Meanwhile, the recent report on stablecoins that exist within the Ethereum ecosystem show their money velocity is closer to 20, and even higher for the more decentralized coins. So while the Fed is printing trillions of dollars but cant get circulation of money in the economy, it's the Ethereum platform is more than an order of magnitude more effective.

Enter decentralized finance (DeFi). Its intention was to vastly improve on the inefficiencies and high costs of the legacy banking system. In a nutshell, with banks, no velocity; without banks, huge velocity. The answer is clear. And things are just starting. Now we have regulated charter banks in the U.S. allowing custody of cryptocurrencies as well as a regulated bank in Lichtenstein accepting the stablecoin USDC as a method of deposit. Crypto is starting to chip away at the legacy banking system.

The Ethereum rails whether its stablecoins, Tether, or USDC is an order of magnitude better than the SWIFT network. Connecting the legacy systems of banks with the Ethereum rail will dramatically improve the end user experience. No longer waiting up to a couple days for money to arrive. Inevitably, as more options emerge, more banks will onboard this new system.

So while banks are getting into crypto, crypto is getting into banking. Existing transfer speeds of the legacy banking system is a joke. DeFi is a fast growing space while traditional banking is losing market share. We will have a mix of players such as centralized exchanges Binance and Coinbase becoming neo banks which are global along with DEXs (decentralized exchanges) like Uniswap, Synthetix, and wallets as part of this spectrum for payment rails used for investing and trading where you can change any of these coins with any other even with your mobile phone.

We have had two decades of slow fintech progress because, rather than overhaul the legacy infrastructure, fintech has tried to overlay new ideas on the existing structure. In consequence, such fintech companies have been hampered. As one example, Transferwise tries to avoid international payments by matching local payments. It's far better to use Ethereum, a vastly superior infrastructure, than try to build on the old legacy system. Stablecoins allow us to connect to that legacy infrastructure. Ethereum allows building without constraints.

Threat to DeFi

So the recent bill on requiring KYC/AML on all stablecoin transactions is foolhardy and potentially crippling. Once crypto matures, it would be like requiring each person who transacts in fiat to provide KYC/AML each time. Imagine going to buy groceries and having to do KYC/AML each time.

One of the largest U.S. crypto exchanges, Coinbase, is saying the U.S. government may not allow customers to withdraw coins to their own private wallets unless they do KYC, otherwise they must keep them on Coinbase. Such a sweeping interpretation of FATF guidance has already been applied in Switzerland and the Netherlands. Some think this can affect DeFi greatly, but the technology would just migrate to other countries that dont require this. The problem can also be solved by creating a decentralized on-chain KYC identity for non-custodial crypto wallets so centralized exchanges such as Coinbase can identify you.

Enterprise Ethereum

Regardless, Ethereum 2.0 will open much opportunity for enterprise adoption. Zero knowledge proofs enable private transactions on Ethereum while reducing costs. Baseline protocol fits well with such private transactions. When money gets deposited into a checking account, it has to go through 12 different systems. Ethereum eliminates these silos. You can have one ledger that has the truth in it, and within that, you can build business logic around it then send it to different areas of your bank or company without having to go through different system types and message formats. Ethereum standardizes banking procedures so it is known who owns what and when. This would eliminate the extraordinary duplication of effort within banks. With a total of 22 different banking systems, Ethereum is an obvious use case.

Inevitably, banks will start to adopt this technology. Smaller banks are over because they have these legacy costs so cant compete. But juggernauts such as JP Morgan are embracing this because they understand how to and have the capacity to drive margin. At present, most of the big banks are just waiting to decide when to make the big move. Big change ahead, stay tuned.

(͡:B ͜ʖ ͡:B)