Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

Bitcoin: Why This Time Is Different

We have highlighted in prior reports to members the numerous tailwinds that made bitcoin a buy on entry points near lows. This includes the buyable gap up in GBTC on July 27 in a report dated Aug 3 after bitcoin had a constructive pullback to absorb the sharp gains off major lows. This was followed by a report on Aug 7 of two pocket pivots issued by GBTC, both actionable. While my metrics have kept me on the right side of major trends bitcoin in real-time since 2013 as backtests had been successful from early 2011 based on available data, the price/volume action of BTC, ETH, and top altcoins often carry the most weight whether or not one is a macro/metric expert.

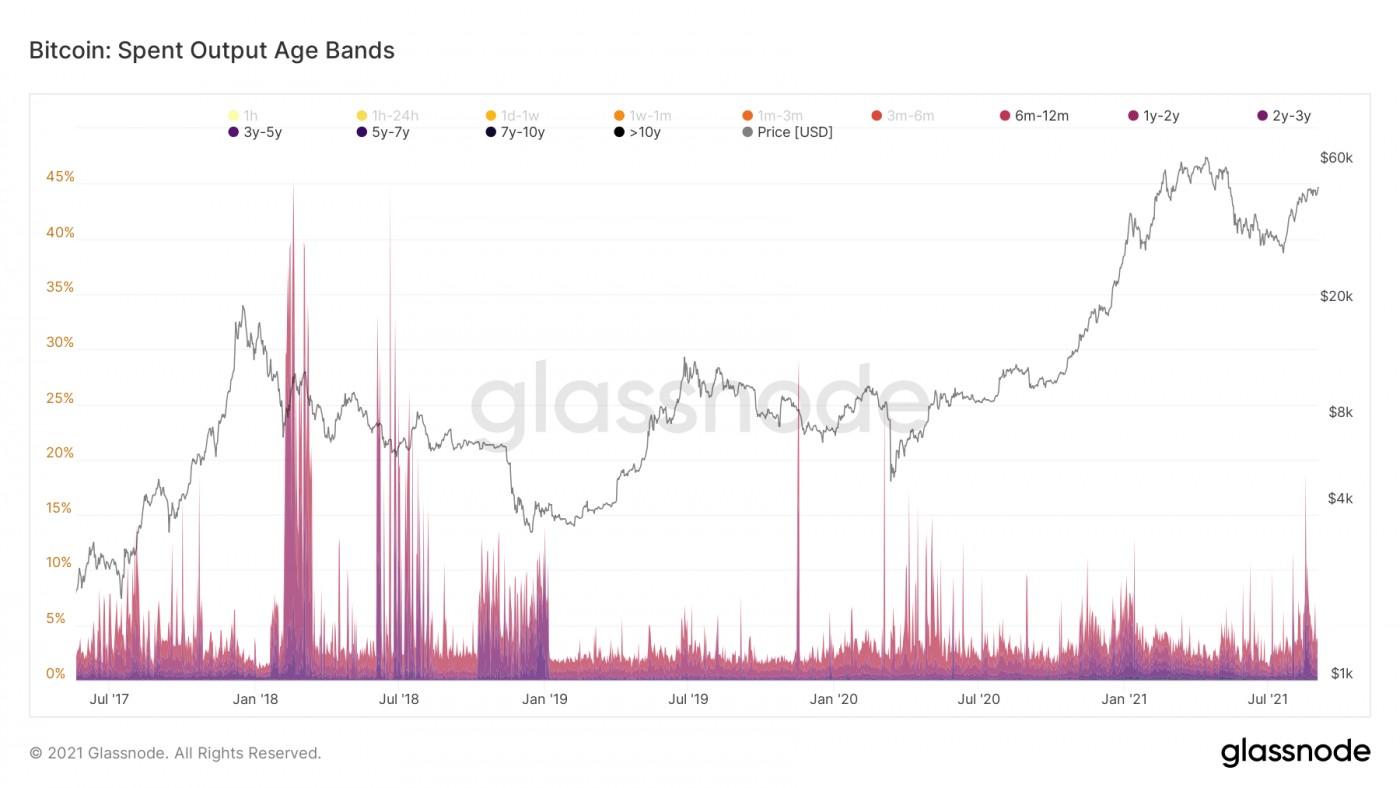

That said, one interesting metric is illiquid supply. It has clearly broken out of its historical pattern, showing levels of accumulation unseen before. Market participants are HODLing their coins stronger than ever before. 93% of bitcoin has not moved in a month while the bigger waves of institutional investment is only just beginning.

Further, notice the difference between the aggressive selling of long-term holders (LTHs) denoted by the cluster of sharp red spikes after the market top in late 2017 in bitcoin (and the Jan-2018 top in ethereum) and today. LTHs are sitting tight, not even remotely resembling behavior during the dead cat bounces in 2018.

In developing countries news, El Salvador GDP has already jumped 3% due to far fewer being gouged by remittance fees from the likes of companies such as Western Union. Other countries now following including Panama, Ukraine, and others. Bitcoin enables the two billion unbanked around the world to send and receive currencies as most of them have mobile phones.

When Will QE End? #BubblesBursting

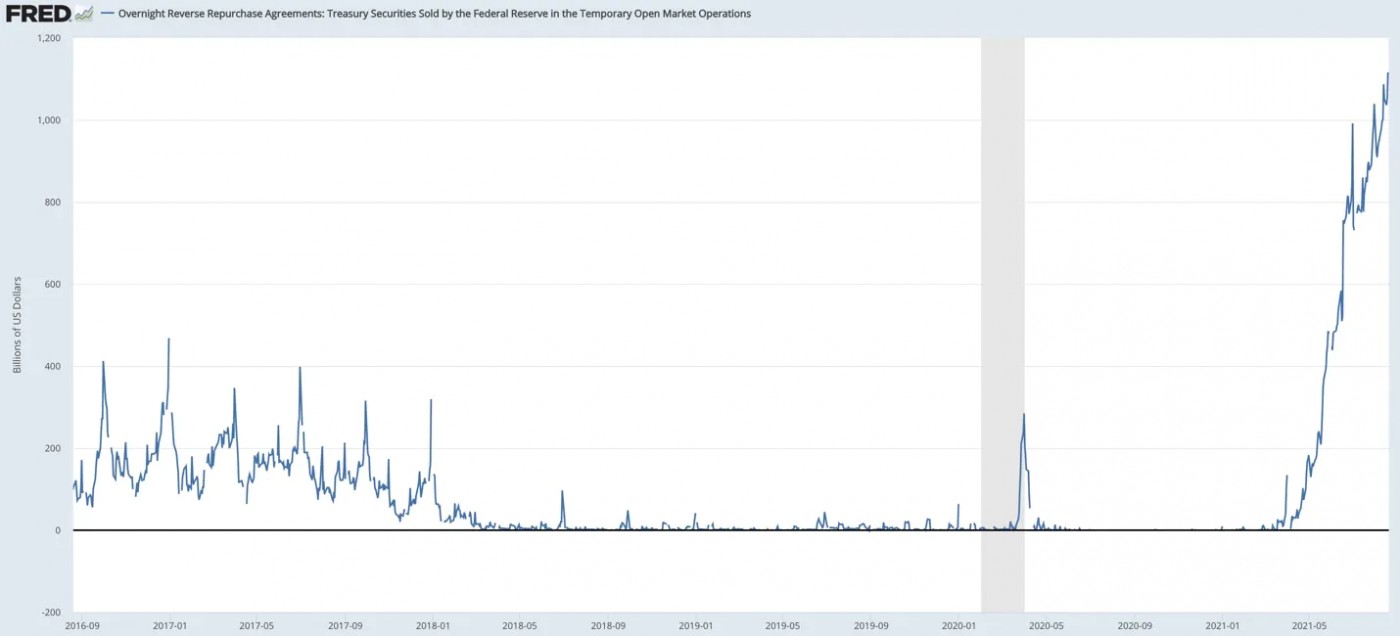

QE is a quiet effective way for the government to transfer resources from the bottom 50% to the top 5%. Post-COVID, the ratio has shifted to even more populist extremes. Likewise, inflation is a quiet but effective way for the government to transfer resources from the people to itself, without raising taxes; Inflation continues to accelerate. When you couple this with the Overnight Reverse Repurchase Agreements (reverse repos) exceeding an unprecedented $1 Trillion dollars, the U.S. Federal Reserve may want to start hiking rates sooner than expected. But wanting is a far cry from doing. As we have said over the years, the Fed was painting and now has painted themselves into a corner. The question is how much longer can they continue to print before the system breaks down? If history is any guide, money printing can continue for much longer than people expect. The market also continues to show that inflation fears, as it relates to the continuation of the bull market, are likely still overblown. Most importantly, history shows us that some of the best market gains in a bull market occur in the final innings. We may only be in the 6th or 7th inning thus this market still has a lot of room to run where various pullbacks remain buying opportunities.

A reverse repo is an agreement to purchase securities from an authorized institution in order to sell them back at a slightly higher price. Reverse repos are used for short-term borrowing and lending so institutions can meet deposits and reserve requirements. A greater number of these institutions have reached their limit on the reserves they can absorb, thus fewer institutions bid on the offerings which causes the issues we are now seeing. Money supply together with a decrease in the velocity of money due to banks unwilling to make loans which has kept economic growth at bay has led to the reverse repo anomalies since banks have a limit to the amount of money they can legally hold, so we have an oversupply in the system, ie, too much liquidity.

This has been sparking inflation. As we get closer to herd immunity, C19 will be muted, people will start to spend, and inflation will push higher. But history and the stock market at present suggests even if inflation is not transitory, the best part of the bull market is closer to the end of the cycle. An inverted yield curve has preceded every recession since 1956. But the market top which typically ended in a strong run to new highs typically came 1.5 to 2 years after the yield curve inverted. The only exception was the recession in the first half of 2020 when the yield curve inverted in May of 2019, or less than a year, due to unprecedented levels of QE flooding into the system due to C19.

The yield curve is currently showing a healthy slope as of this writing but once it inverts, the clock starts ticking. Historical odds suggests a strong market finish 1.5 to 2 years after inversion, but we could also have a market such as in 2008 which gradually deteriorated before the financial crash. Price/volume rules all.