Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

The (R)Evolution Will Not Be Centralized™

Plunging Rates

U.S. equity markets had their worst week in 12 years and their fastest -10% loss from new highs. Markets are forward looking by several months. The economic ripple effects from the supply-chain, disrupting coronavirus are being priced into future economic reports which are being adjust downwards. On Monday, the Organization for Economic Co-operation and Development (OECD), in a best-case scenario, with only limited outbreaks outside of China, is still predicting what it called a "sharp" slowdown in world growth in the first half. Prompted by supply chain disruption, a fall in tourism and weakened confidence, economic growth is now expected to be 2.4% in 2020, down from its former prediction of 2.9% for 2020. Global growth below 2% is traditionally regarded as recessionary.

It also warned a broader contagion spreading across Asia-Pacific, Europe, and the U.S. could see global growth fall even further to just 1.5%, as some regions - including Japan and the eurozone - may slip into recession.

Should future economic reports disappoint beyond what is already expected, markets will fall and vice-versa. The counterbalance to this is central banks are stepping up. The OECD report came as the Bank of England said it was working with the Treasury and international partners "to ensure all necessary steps are taken to protect financial and monetary stability" in the face of the virus outbreak. Money markets are pricing in a 25 bps rate cut when they meet on March 26, though Goldman Sachs went on record they expect a 50 bps rate cut, saying the coronavirus outbreak is likely to push the UK economy to the brink of recession in the coming months. Other central banks including the Bank of Japan and the US Federal Reserve have also pledged to act to support the economy if necessary. On Monday February 2, the Fed slashed rates 50 basis points in a rare inter-meeting rate cut. This is the first rate cut of 50 bps since the 2008 financial crisis. All rate cuts since then have been 25 bps.

"The fundamentals of the U.S. economy remain strong," the Fed said in a statement on its website. "However, the coronavirus poses evolving risks to economic activity. In light of these risks and in support of achieving its maximum employment and price stability goals, the Federal Open Market Committee decided today to lower the target range for the federal funds rate by 1/2 percentage point, to 1 to 1‑1/4 percent."

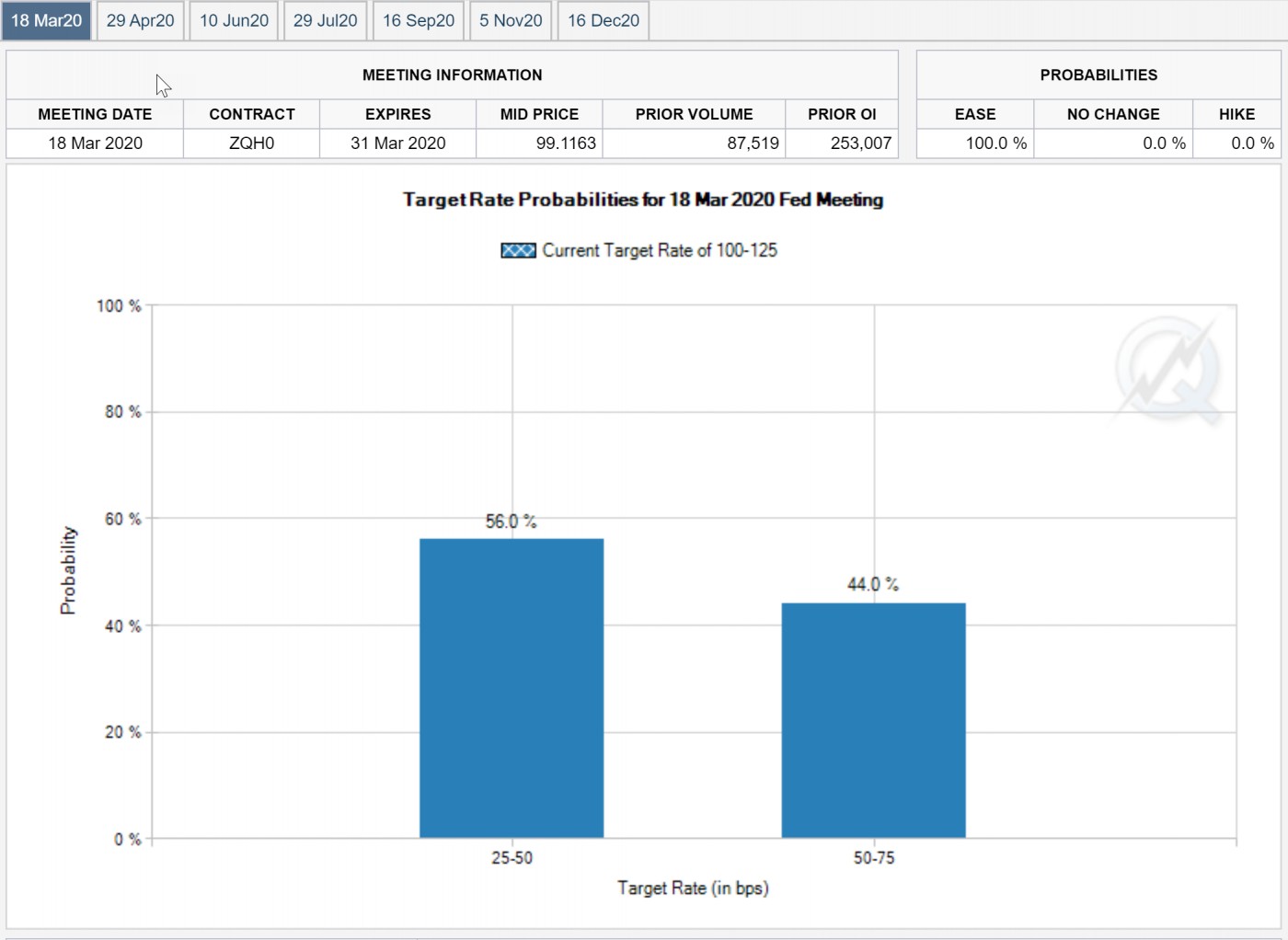

Perhaps a bit surprisingly from where things stood just yesterday when markets were pricing in a 21% chance the Fed would cut by 25 bps and a 54% chance by 50 bps at their meeting on April 29, but odds have greatly shifted to expecting the Fed to cut rates by 50 to 75 bps at the next Fed meeting on March 18 as a certainty:

The ECB is also expected to trim rates by 0.1% in April.

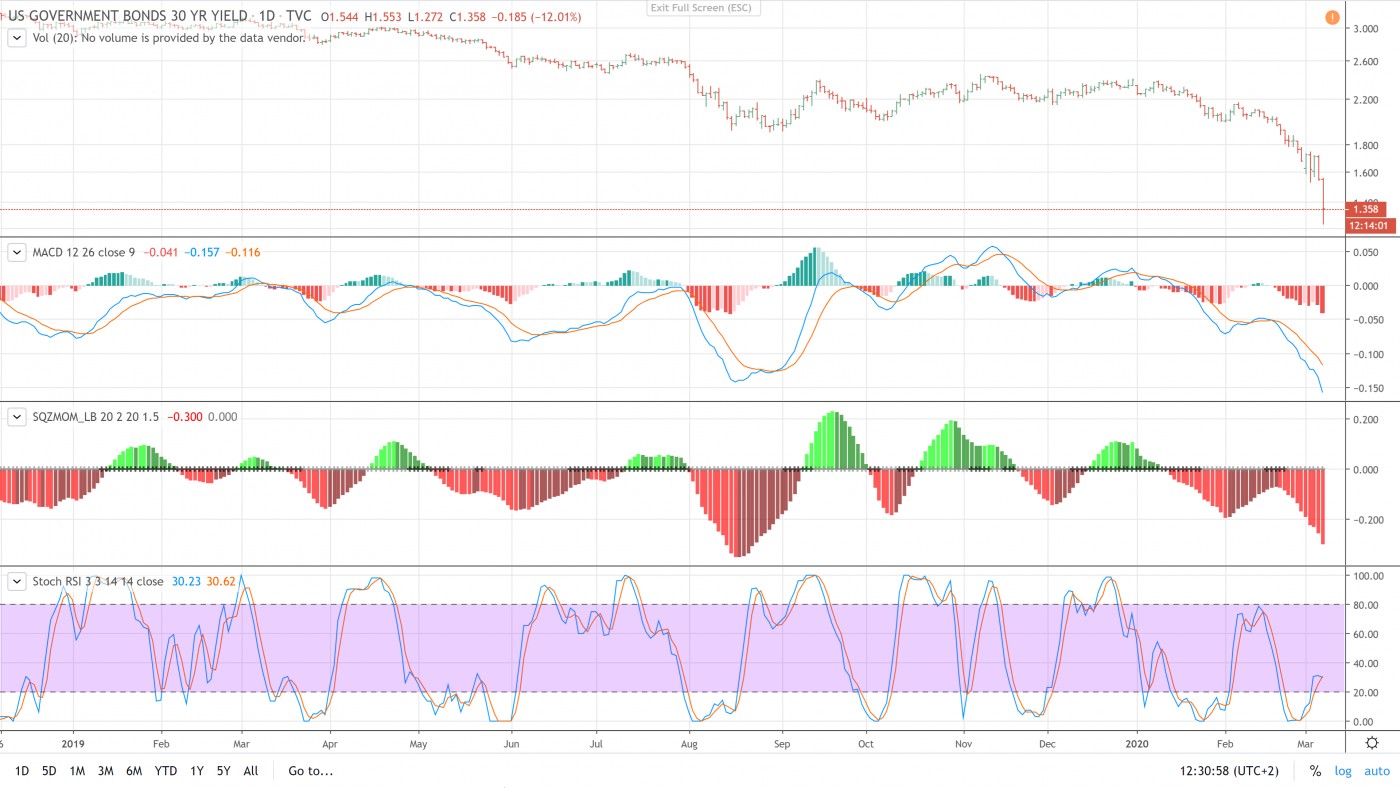

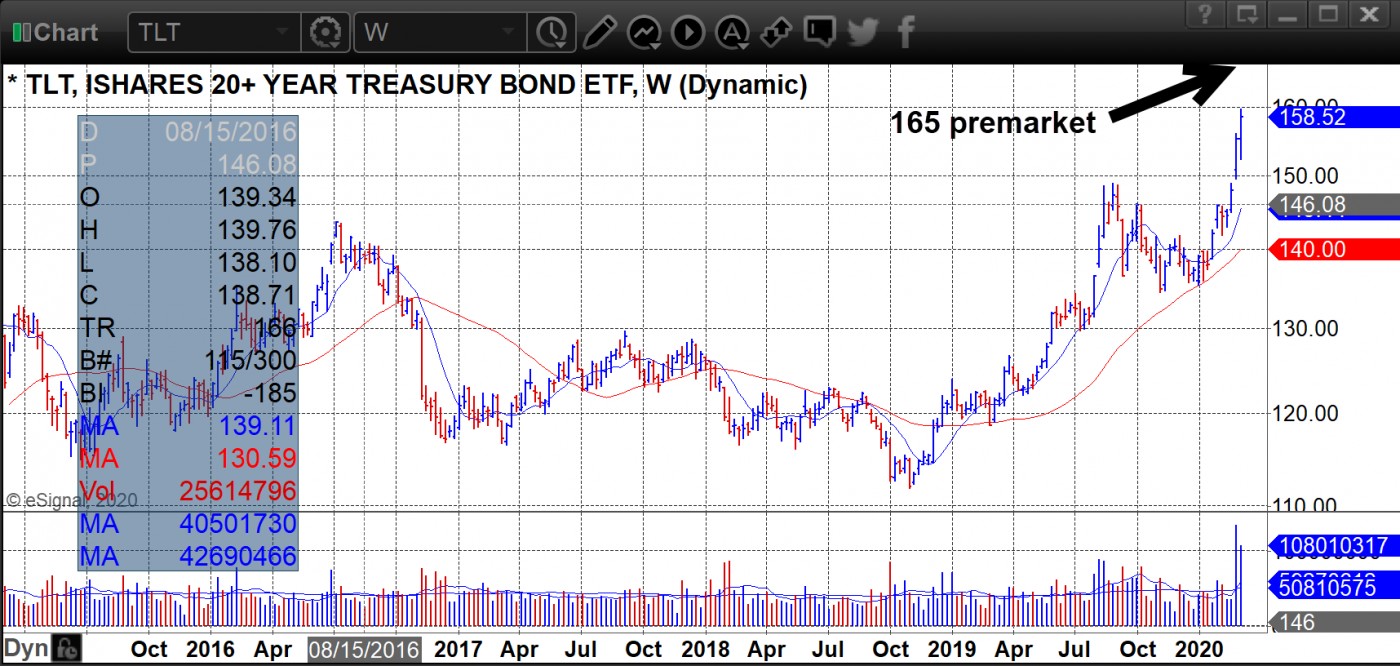

Meanwhile, on Tuesday February 3, the United States 10-Year yield fell below 1% for the first time ever, forcing banking stocks even deeper into the red, while the 20+ year Treasury bond ETF TLT spiked higher. TLT is at 165 at the time of this writing.

The Bounce

All that said, markets finally had their bounce last Monday with the Dow Industrials up over 5%, or 1293 points, despite the release of dismal data out of China. China’s official manufacturing PMI, released over the weekend, slumped to 35.7 in February from 50.0 in January, marking its worst level on record. Meanwhile, the non-manufacturing PMI printed at 29.6, down from 54.1. That is a serious clobber to their economy. This should also lambaste other economies in a domino effect of sorts which explains the overnight plunge in bond yields and certainty of the Fed cutting rates at least 50 bps on March 18 at their next meeting.

Rates can continue to fall and, in those parts of the world where rates are already negative, go more negative. Investors continue to buy bonds not for the negative yields but for the speculative hope that rates will move even lower thus pushing their prices higher. It's important to keep in mind that while official and market rates sit below the rate of inflation, the 1970s brought a similar situation when inflation ran into double digits.Volatility remains in play, however, as new cases of corona surface in the U.S. and other countries. Further, the head of a money management firm, Alan Lancz, remarked, "I think it spooked investors after the strong rebound, because it was made right away and it was 50 basis points. So it was larger than people (were expecting), and some may be thinking, 'Are things worse than we think?'"

The Era of Digital Assets

Given the quickening pace of the debasement of fiat, bitcoin remains in its general uptrend. The recent weakness is a buying opportunity. MACD, RSI, and Squeeze Momentum all show it is still not too late to buy the Grayscale ETN GBTC which tracks the price of bitcoin.

In the future, the tokenization of hard assets will be tradeable sooner than later to retail and institutional investors. It will enable retail investors to push their debasing fiat which sits in savings accounts into higher yielding investments which provide a yield of at least a few to several percent with minimal risk. Conservative investors and savers will find solace in the availability of such tokenized securities as a superior alternative to near zero to negative yielding bonds and savings accounts. Indeed, with rates heading lower, Germans and other saver nations are set to move some of their trillions in savings into more positive yielding investments.

2008 Redux?

Interestingly and perhaps not surprisingly, as mainstream media preyed upon the corona-induced fears across the planet, on Friday February 28, everything including gold nosedived. Equity markets, precious metals, and even bitcoin gapped lower. Only the price of bonds gapped higher as yields gapped lower on rate cut news. This was reminiscent of October 2008 when everything jackknifed lower over a series of days, though this came after a few months of prior weakness so did not start from all-time highs. In today's markets, however, with markets used to central banks stepping up, all the rate cut intentions made by central banks across the board helped markets bounce. Still, expect additional waves of negative corona-related news as the number of cases continues to climb.

So the burning question is whether the major U.S. stock market averages have seen the worst of things.

Here are reasons why the market will not drop well below major lows made on February 28 though certainly could retest lows which sit several percent away from where major averages are trading at the time of this writing, given the nature and tone of the mainstream media:

1) A vaccine is created ahead of schedule or at least an announcement is made that a vaccination will come sooner than later. While the number of cases will certainly accelerate in newly infected countries, the rate of infections should peak ahead of the all-too-often dire predictions reported by mainstream news. Some reports were placing a vaccination 12 months out which seems absurd based on AI-based methods being employed in the creation of a vaccine. So while the rate of infections remains exponential, this curve should flatten then fall in the months ahead. That said, the damage done to the global economy by the virus is serious even were a vaccine to be created sooner than expected.

2) The number of cases peaks in reliable countries such as South Korea as an example for what other countries can expect. China already claims the number of cases have peaked though it's clear they under-reported the number of cases by at least an order of magnitude, so their claims remain suspect. Accusations that the U.S. is slow to act is born of the leftist mainstream media wanting to make President Donald Trump look as bad as possible despite $8.3 billion earmarked in spending to contain and treat the coronavirus in the U.S. Such perceptions further stokes fear and panic.

Indeed, in today's world, mainstream media has brainwashed the masses into believing things are far worse off today than ever, while hard data shows the complete opposite. Voices of reason from the likes of Raymond Kurzweil of MIT, Peter Diamandis, and others come armed with proof of how much better things are today overall for each 25 year tranche going back 200 years. This extends to literacy rates, infant mortality, working conditions, working hours, life expectancy, freedom of choice, and a host of other metrics. Moreover, the Law of Accelerating Returns was put forth by Kurzweil which says the rate of progress in any evolutionary learning environment which includes deep and machine learning increases exponentially. In other words, as a system evolves through iterative learning, the faster it evolves. Just as ideas beget ideas, evolution begets evolution. More than a century ago, two-thirds of the working force worked on farms or in factories. By 2015, these statistics dropped to one-tenth of the working force. But since those jobs are created as needed, politicians and mainstream media capitalize on the present moment to stoke fears that technologies that spur automation will lead to lost jobs. Sure, in the short run this is true. Truck drivers will no longer be needed due to the emergence of self-driving vehicles. But ultimately, more new jobs will be created than jobs lost due to technology as has always been the case. The renowned Naval Ravikant said 90% of jobs on Wall Street will be gone in several years due to blockchain's ability to eliminate middle men via its trustless technology. And as we go forward in time, jobs are becoming increasingly creative and unconventional as more free time lends itself to a deeper appreciation of the creative arts. But I digress.

3) The coronavirus's impact on the global economy on the already substantially reduced growth estimates turns out to be less damaging than expected. Given the initial pessimistic tone on controlling the virus and finding a vaccine, the revised estimates in global GDP have been substantial. Certainly, quarantines of parts of populations and supply chain disruptions will certainly impact global GDP. But as the initial reports reflecting the spike in fear and panic without proportional attention paid to more sober, realistic analysis fade, clearer heads should prevail which should provide a counterbalance to the often extreme positions taken by mainstream news sources. My research going back to 1891 (the data available at the time I did the study) showed all acute crises including pandemics have caused only short lived corrections. Equity markets in the U.S. typically recovered all losses within weeks to a few months.

4) Central banks continue to cut rates. It appears that all central banks have stepped up to do what it takes to prevent the global economy from slipping into recession.

Now flip any of those four reasons and you have a situation where markets will at least undercut major lows made on February 28. Negative news spurring panic in the coming days will go head-to-head against the reality of an impending vaccination, further rate cuts, actual damage done to the global economy, and a peak in the number of cases. Expect levels of volatility to remain elevated. Also expect the mainstream media to do what it does best- stoke the fears of investors, retail and institutional alike. Since the primary driver in price is always determined by supply/demand, should selling pressure intensify due to mistakenly held beliefs spurred on by mainstream media, it will nevertheless cause U.S. equity markets to at least retest lows which sit several percent away from where the majors closed on March 5. This also means the majors are only off about -10% from all-time highs. Price/volume of the majors seems to indicate that institutions are taking a risk-off approach as there are a growing number of down days on higher volume accompanied by up days on lower volume.

Variances

As Ray Dalio of Bridgewater has said, we are at a 75 year tipping point on a long term debt cycle. The coronavirus could be the straw that broke the proverbial camel's back, pushing the planet into recession that ends up being far worse than expected due to more than a decade of sovereign debt via QE. A mild recession is also within the realm of possibility as exponential growth technologies together with easy money help mend the damage.

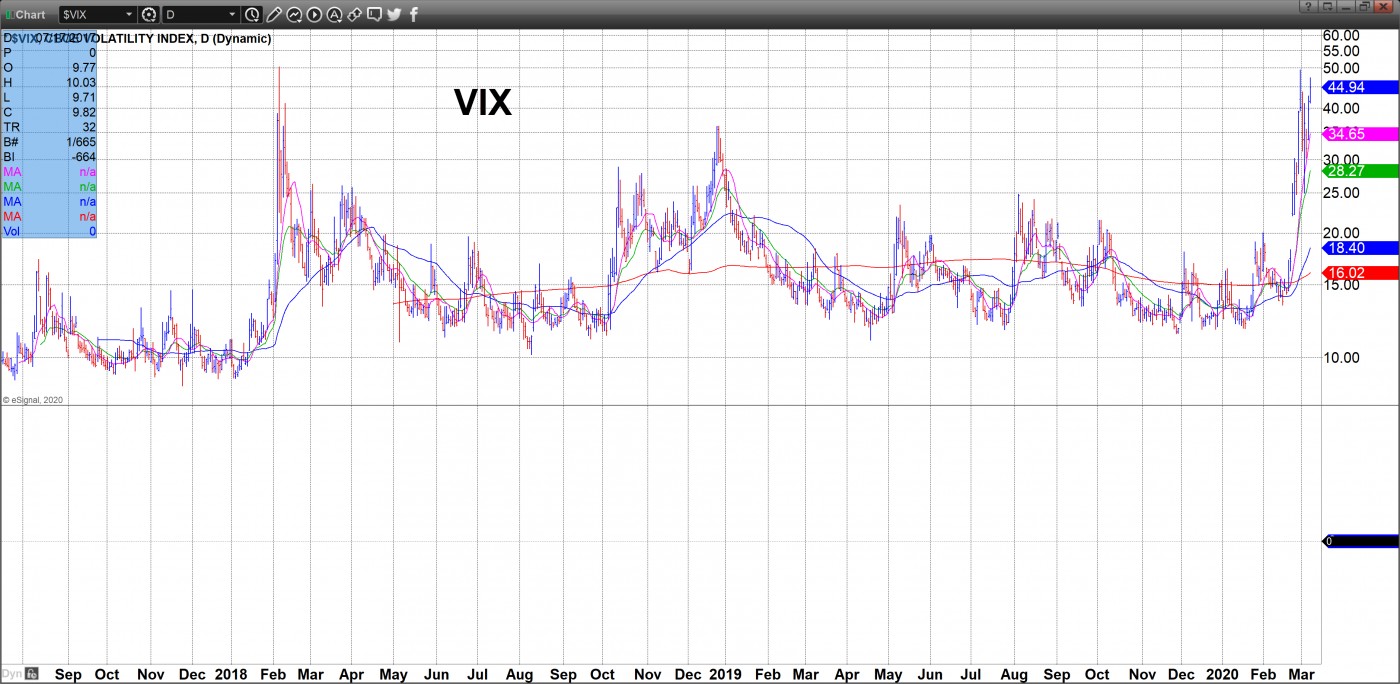

The VIX is spiking again as I type. The market is pricing in even steeper rate cuts, both pending and realized. It may not have properly priced in things getting worse before they get better concerning the number of coronavirus cases which would cause a more serious correction as it would imply more damage to the fragile global economy. On the other hand, a vaccination is also not priced in yet. Stay tuned.

(͡:B ͜ʖ ͡:B)