by Dr. Chris Kacher

Inflation concerns

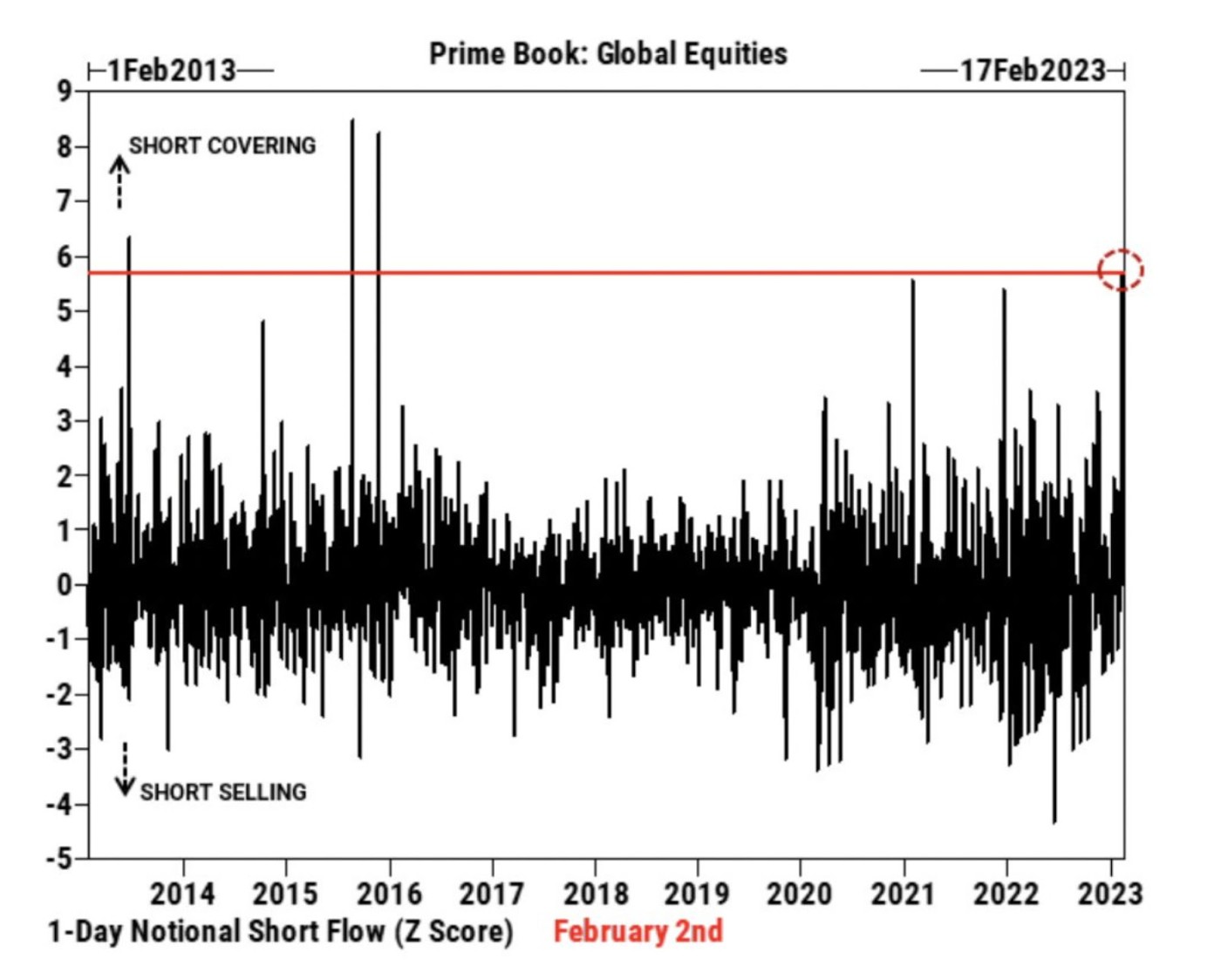

A number of Fed members have said they are not seeing signs of a quick decline in inflation. Thursday's PPI also came in hot above expectations. In consequence, the CME fed fund futures now predicts a terminal rate of 525-550 at minimum, or at least three more 25 bps rate hikes. One Fed member said the market bounce implies investors think inflation will cool faster than the Fed thinks. But upward pressure on inflation comes in part from food whose prices should remain elevated due to wheat and fertilizer shortages from supply chain issues caused by COVID and the war between Ukraine and Russia. We also have a very tight labor market. The last time unemployment was 3.4% was in 1969. Low unemployment numbers presume more Americans have more capital to spend. The bounce is also due in part to the largest short squeeze since 2015.

So while mainstream media thinks we may get a soft landing, many recessions looked like a soft-landing at first such as in 2008. Low unemployment and low wage price pressure typically look favorable shortly before a major recession. But these data points can turn on a dime into exponential increases over several months once things begin to unravel if past recessions are any guide. Further, the UK is already in recession with the EU soon to follow. Economies correlate so it's only a matter of time before recession hits the US, likely sometime later this year.

Treasury yields and the dollar are also on the rise. Interest rates tend to follow Treasury yields, especially on the 2-yr and 3-mo.

Unemployment paradox

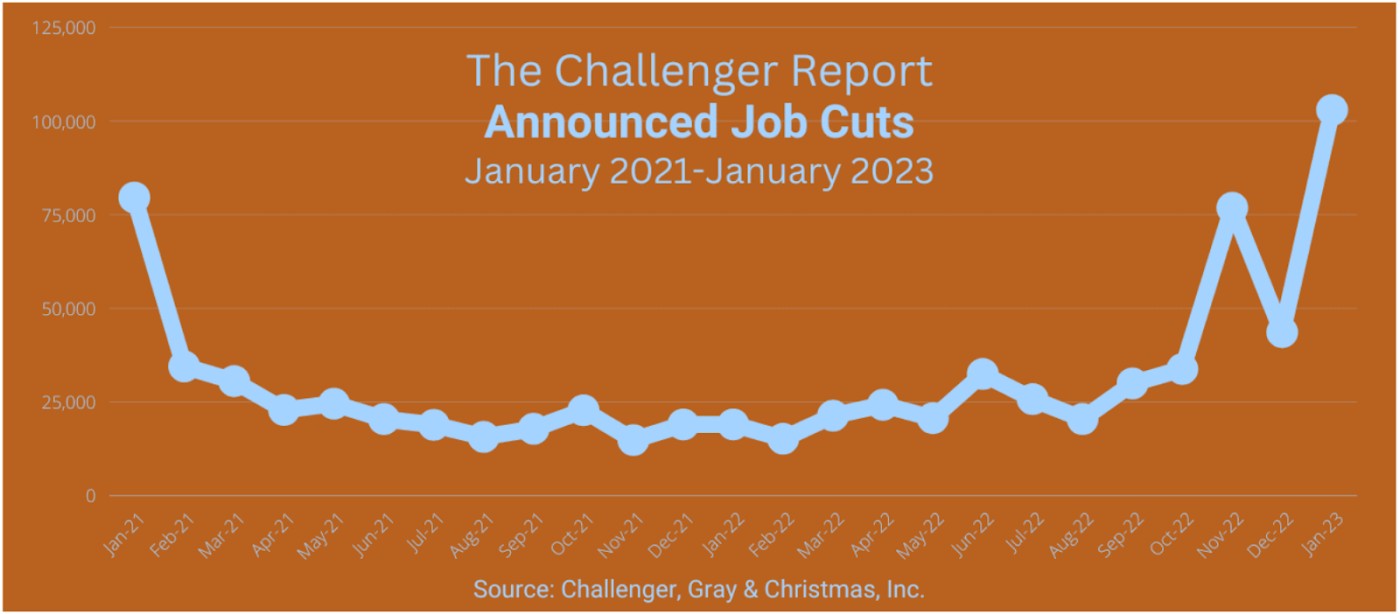

Layoffs are rising steeply as there were 57% more layoffs announced in the month of January than the entire 4th quarter of 2022. 84% of the companies cited economic conditions.

So how can layoffs increase so dramatically while we’re also seeing lower unemployment and initial jobless claims?

Three reasons:

1) Newly laid off individuals aren’t seeing the need to file for unemployment because they believe they can find new jobs quickly.2) Approximately 8 mil Americans are working more than one job so losing one job does not mean one becomes unemployed.

3) The unemployment rate is a lagging indicator while the Challenger Report measures the announcements of layoffs rather than the layoffs when they occur. There is typically a two to three month time lag before an employee leaves the company after the announcement is made due to various regulatory rules.

One of a number of past examples occurred in Q3 2000 when the number of layoffs moved higher while the unemployment rate moved lower. The unemployment rate then began climbing in Q1 2001 which is when the recession officially started. I had published a report back in the middle of 2000 about the inevitably oncoming recession despite very low unemployment since history was on my side. But Wall Street is often about sales and never using the 'R' word so the report was ridiculed. It taught me that there are larger forces at work that override the unending search for truth when it comes to trading.History shows that when layoffs cross above 250,000, recession comes within months. Over the last three decades, whenever layoffs crossed from below 200,000 to above 250,000 within 2 quarters, recession also occurred within months. This happened in 2001, 2008, and 2020. We are highly likely to exceed 250,000 in the second quarter of 2023, so expect recession to come sometime in the third or fourth quarter of 2023.

A counterforce?

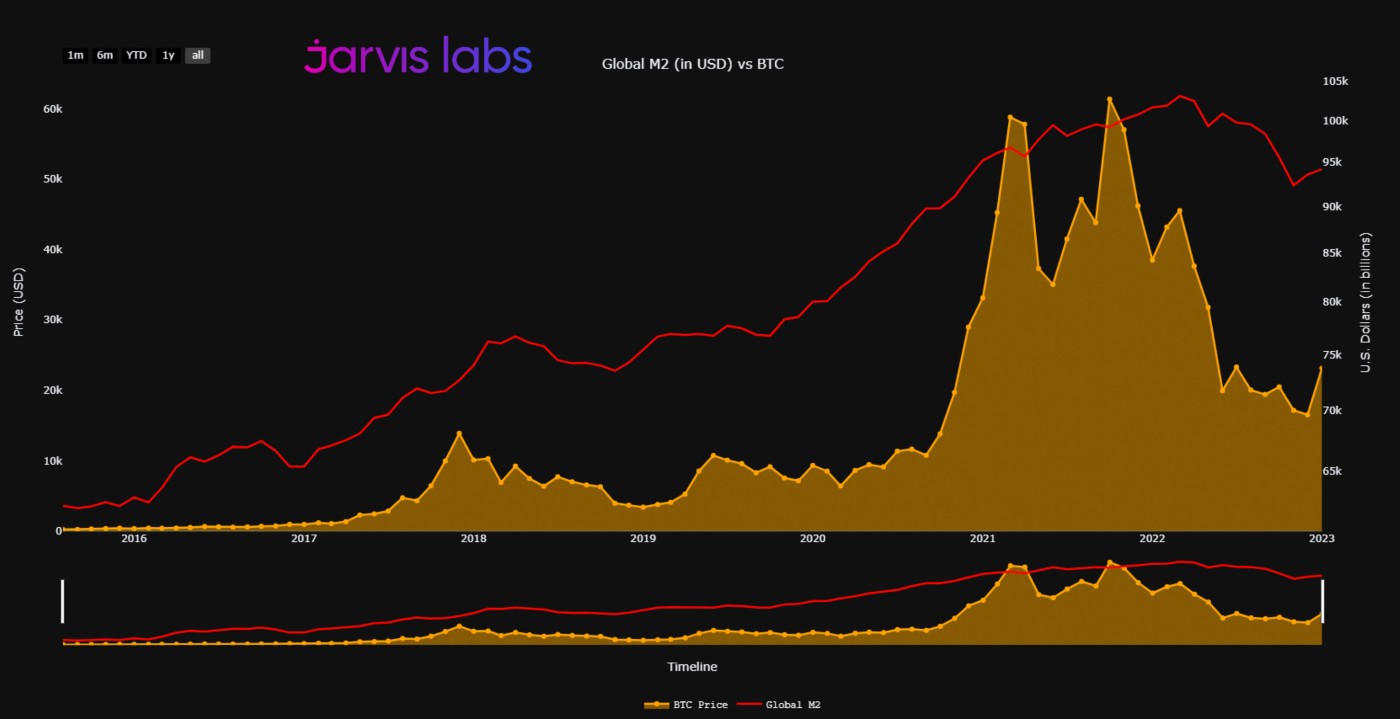

In terms of overall market direction, one issue that throws a spanner into the above reasoning is global M2 continues to increase due to money printing out of juggernauts China, Japan, India, and Russia among others. So while tightening is occurring in the US, UK, and EU, is it not enough to offset the amount of M2 being created by the rest of the world. Further, the Fed's $2 trillion repo market enables them to add liquidity when needed to service interest payments on record levels of debt without impacting M2. That said, while global M2 dropped for much of 2018, the US stock market continued to trend higher all the way up until the last quarter of 2018, so the correlation can lag by several months. The cryptocurrency market however has had a stronger correlation with global M2 over the years.