Oil-induced inflation

February producer prices PPI came in at 0.7% month-over-month, more than double what economists expected and the sharpest jump since August 2023. This was logged before the Iran war began. The next PPI is likely to be even more elevated. Underscoring this, Truflation shows its inflation gauge has more than doubled, climbing from 0.68% on February 8 to 1.52% as of March 18.

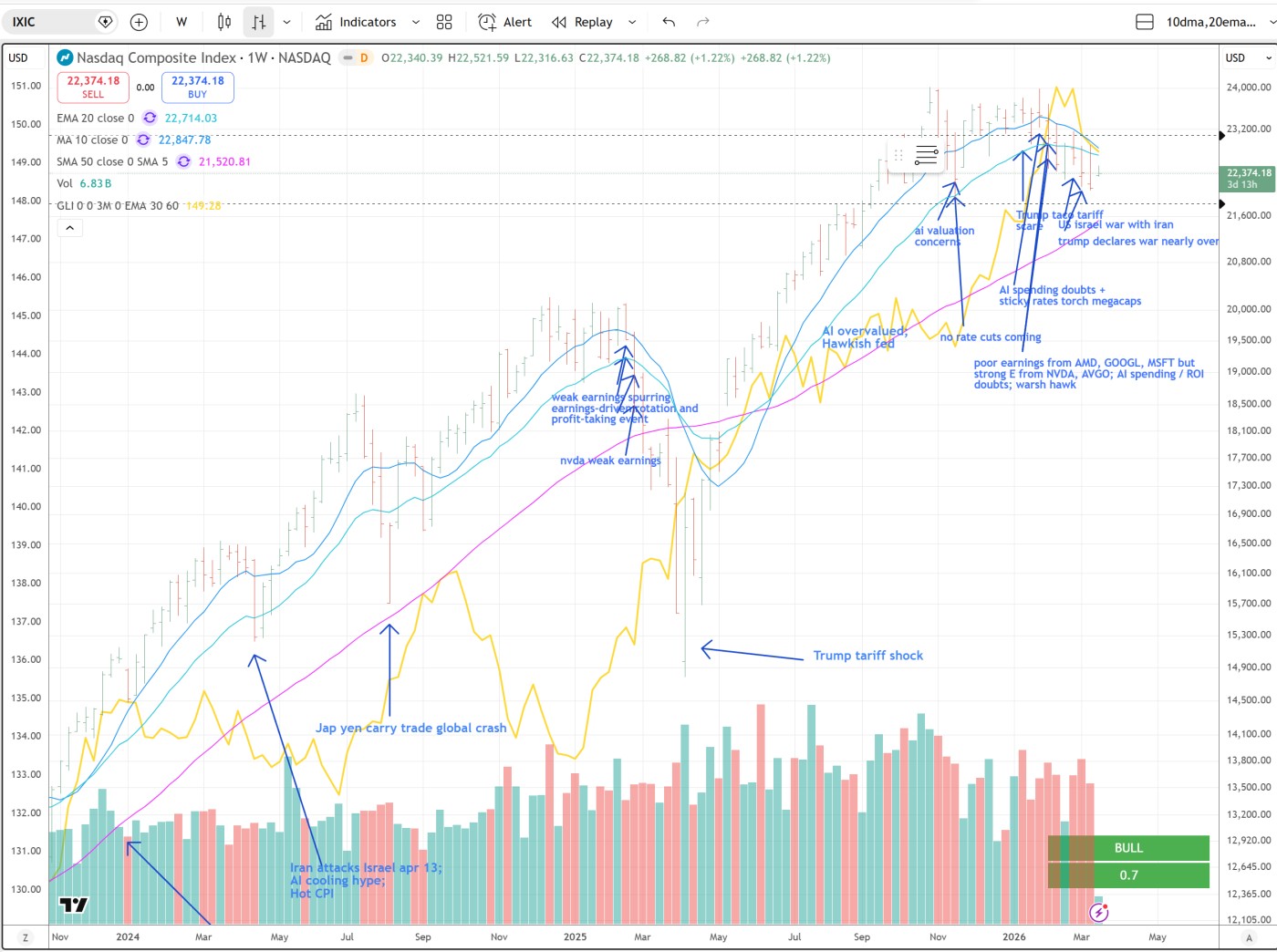

But this is not the 1970s. Productivity from the AI boom may continue to push GDP beyond expectations while supply-side deflation may give central banks headroom to cut rates further.

No AI capex bubble

Some analysts have said that infrastructure spending over 3 percent of GDP always crashes the economy for a decade. Over the last century, railroads, electrification grids, and highways prove it. But after the crash, those assets lasted generations.

AI data centers are different. GPUs and servers are obsolete in three to four years. Spending hits around 2 percent of US GDP in 2026 and could reach 5 percent by 2029. No financial model has ever survived the constant refresh costs and weak monetization. In consequence, some predict a huge meltdown in 2029. But this cycle is different:

Hyperscalers are spending from their own massive cash flows, not speculation.

Unlike older models, they can adjust capex quickly if returns drop.

AI-based buildings, power, and cooling have 15–30 year lifespans and can be repurposed easily.

Hardware improves two to three times per generation, extending real returns.

At Jensen Huang's benchmark of 10 billion annual revenue per gigawatt, payback arrives in four to six years with 70 percent plus margins, better economics than railroads ever managed.

AI already adds meaningful GDP growth and will drive far more through productivity gains. Recent quarters show it driving 0.3 percentage points or more of US GDP expansion through capex and related effects. Forecasts peg it at 30 to 40 percent of 2026 growth. Productivity gains from automation, scientific acceleration, and new business formation expand the GDP base itself, rewriting the denominator.

Energy constraints ease with solar and storage scaling rapidly.

Demand for compute outstrips supply today, and the buildout creates its own flywheel: cheaper intelligence unlocks more usage, more applications, more revenue.

Nvidia AI monopoly

Jensen Huang, CEO of NVDA, also just buried doubts about AI spending peaking. He told 30,000 attendees NVDA sees at least $1 trillion in demand through 2027 for Blackwell and Vera Rubin, double the $500 billion he cited last year for those platforms through 2026. Demand exploded overnight. When the world's most valuable company signals that, betting against the AI buildout gets hard. He went further: "We are going to be short. Computing demand will be much higher than that." He dismissed bears claiming hyperscaler capex would fade. Vera Rubin ships second half this year, fueling agentic AI and massive inference. So while the Magnificent 7 lost over $2 trillion from peaks and sit 14% below records, they've tripled in three years and still hold $20 trillion in market cap combined. Nothing goes up in a straight line.

Even the dot-com boom had steep corrections in late 1998 then chopped sideways in the second and third quarters of 1999 as sharp gains needed to be digested.

Jensen is positioning NVDA as the operating system for everything: robotaxis, humanoid robots, orbital data centers, and yes, even physical AI systems running in space. This is Microsoft in the PC era, Google in the search era, but a hundred times bigger. NVIDIA inside everything.

CaveatsBurnout warnings assume linear extrapolation from today's economics, but AI's core engine is intelligence compounding on itself with recursivity at the helm. Each breakthrough unlocks cheaper/faster training, better data efficiency, new architectures, and applications that create their own demand flywheel (abundance deflation, productivity explosions, new industries). Musk and Andreessen's "jaw drops every day" isn't hype; it's firsthand witness to the curve steepening in ways spreadsheets can't capture yet. Past cycles (internet, mobile) had similar "over" moments before the real explosion; this one looks bigger because intelligence itself scales. AI infrastructure isn't slowing. It's accelerating, and Huang just gave the market the number that underscores it.

Critics say it isn’t quite as simple as it sounds. That trillion-dollar NVDA revenue figure represents bookings spread across two years, and NVIDIA’s real bottleneck is not demand – it’s TSMC’s ability to manufacture chips. They’ve already locked up 70% of TSMC’s 3-nanometer capacity. But Elon Musk's new Terafab facility will address this need. If Tesla can actually scale independent semiconductor production in the US, Elon is single-handedly de-risking World War III. A Chinese invasion of Taiwan becomes far less catastrophic if we’re not completely dependent on TSMC for advanced chips.