NVDA earnings

A 4% beat on the top and bottom line came with a side of more good news in the form of a monster $65 billion revenue guide for the fourth quarter. That said, a slowing revenue growth rate is souring investors, regardless of how strong the demand story remains.

Nvidia’s (NVDA) most recent earnings report for Q3 2025 was indeed very strong, handily beating both revenue and profit expectations with $57 billion in quarterly revenue (62% year-over-year growth) and fourth-quarter guidance that also topped forecasts. CEO Jensen Huang emphasized extraordinary demand for AI chips and “AI factories,” and highlighted major ongoing platform and data center shifts. Analysts generally accepted the numbers as real, noting high growth in data center revenues and strong forward guidance.

However, despite initially gapping up after the report, NVDA’s share price quickly reversed and turned negative. This reversal was due to:

Skepticism about Growth Sustainability: Some investors fear the AI infrastructure boom could overheat or that current demand trends may not continue at the same explosive pace.

Profit Taking/Valuation Concerns: After a huge multi-year run, many investors may have taken profits, worried about the stock’s high valuation even after another “beat and raise.”

Broader Market Volatility: Along with NVDA, other AI and tech stocks also faded, suggesting a sector-wide risk-off move, not just company-specific doubts.

Nvidia’s CEO did talk up the strong AI demand and issued optimistic guidance, but the numbers were real and confirmed by analysts. The reversal of NVDA’s stock is due to profit-taking, valuation, and macro/sector concerns.

On rates

Also, the Fed is effectively entering another interest rate decision with an economic data blackout. The October report will not be reported in full due to a lack of data due to the shutdown. Markets do not like information asymmetry which puts investors even more on edge in this market. When a sudden decline begins, investors rush to the exit because the "bubble is popping." When stocks surge, the rally accelerates quickly as capital rotates back into AI stocks, because "AI is the next big thing." Any headline can drive trillions of dollars of market cap in a matter of minutes in either direction for one sole reason: Sentiment between popping bubbles and AI transforming the planet is more polarized than ever. So we had a gap up at the open among major averages and AI stocks on the strong NVDA earnings report then forced selling on high volume as the bears wrest control away from the bulls as bubble fears on overvaluations set in as NVDA's revenue rate slowed despite firing on all cylinders.

Jobs dataThe jobs report also came in with strong jobs creation but higher than expected unemployment at 4.4%, a mixed signal for the Fed. Odds of a December rate cut on Polymarket rose from 22% to 34% but still far below from where the odds of a rate cut stood a few weeks ago.

Correction in stocks and bitcoin

Besides the above, a number of events has triggered the latest sell-off in stocks and bitcoin:

Global liquidity can become retrained at times which can result in market corrections within the context of the bull market. Such has been the case for the last few weeks with rising bond market volatility and a recovering US dollar weighing on liquidity expansion. The liquidity cycle (the process of governments/central banks pumping fresh cash into the global economy which drives prices) appears to have been delayed, and is only just now looking like it’s about to pick up once again from various central banks.

Jerome Powell dashed hopes for a guaranteed December rate cut, stating it is "not a foregone conclusion" amid differing views within the Federal Reserve and uncertainties from inflation risks and a softening labor market.

The U.S. government shutdown became the longest on record surpassing the previous 35-day shutdown. This stalemate has left many federal workers unpaid and disrupted services, with limited signs of imminent resolution.

The economic data blackout caused by the shutdown had a growing impact on markets, as vital government economic reports are delayed or omitted.

Regional banks are coming off a bout of fraud and bankruptcy issues.

Government shutdowns and balance sheet constraints mean there is limited fresh money flowing into the market. Emergency lending and repo operations show strains in short-term liquidity markets, similar to patterns seen in 2018-2019.

Retail investors currently lack the liquidity and economic optimism to drive price increases, especially with interest rates still relatively high and economic indicators weak.

Bubble (?)

Earnings say no bubble as they have beat expectations by 10.5% on average over recent weeks, which marks the best margin in four years and is also higher than the 8.2% beat in the second quarter.

Earnings have grown at a double-digit rate over five of the last six quarters

Q3 is the ninth straight quarter of positive year-over-year earnings growth

10 of the 11 S&P 500 sectors have seen rising earnings so far this quarter

Stocks rarely fall simply because valuations are high. Instead, declines are more likely when corporate profit growth disappoints.

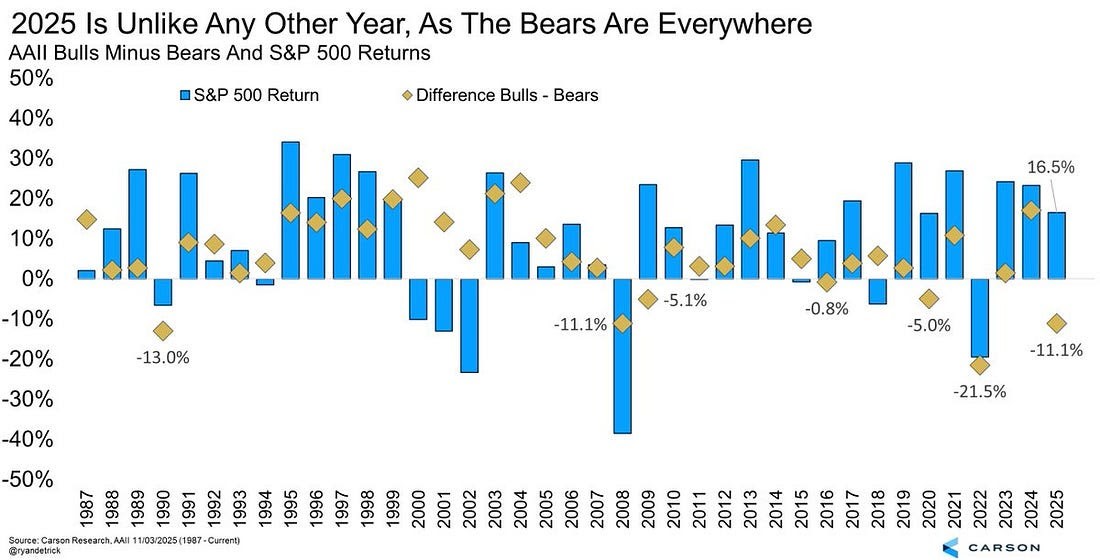

2025 is unlike other years as bears are dominant. AAII bulls minus bears is -11.1% in 2025. Only 3 other times has this ever been -10% and all happened in bear markets (1990, 2008, and 2022) making this time different.

The economy is booming with a questionable job market. A survey from the University of Michigan revealed recently that consumer sentiment has neared its lowest level ever. The data comes just a day after firm Challenger, Gray & Christmas reported that layoff announcements in October reached their highest level for the month in 22 years.

The drop in stocks was exacerbated by data reflecting job cuts for October hit the highest level for the month in more than two decades, making 2025 the worst year for layoffs since 2009. Stock indices had been at or near new highs overall with their occasional correction, yet sentiment is in the tank.The obvious culprits are AI and interest rate cuts which help companies do more with fewer employees allowing for increased layoffs while asset owners gain from rising prices in stocks, real estate, and precious metals. This comes at the expense of the average citizen who has little to no investment assets. Thus the difference between the haves and have-nots is near all-time highs.

QEpidemic

Making this worse is QEndless. When it comes to QE, this time is different because the Fed is easing into a financial bubble. This is not to be confused with the potential AI bubble which has been discussed in prior reports. Rather, QE is now effectively monetizing government debt rather than re-liquifying the private system. Ray Dalio discusses how this is typical in late stage economic long term life cycles, thus his deep concern this will not end well. The hope is AI growth with its tailwinds by way of looseness in fiscal, monetary, and regulatory policies will help us grow out of the record levels of debt as we did post World War 2.

The world has never seen such massive change from a technology. Comparisons between the dot-com boom of the 1990s and today underscore this point.

Nevertheless, one growth misstep could topple everything. So far, demand is beyond expectations especially when it comes to data centers. Growth limits to hardware may become the prevailing issue but not for another 1-2 years as discussed in prior reports. In the meantime, AI can help spur growth beyond even lofty estimates.

In prior bouts of QE, inflation was low or falling, the economy was very weak, and asset valuations were not overvalued, so QE was stimulus into a depression.

Today, asset valuations are high and rising, the economy is relatively strong with real growth averaging 2% over the last year and unemployment at only 4.4%, inflation is above target at a bit over 3%, and credit is abundant with spreads near lows. So today, QE is stimulus into a financial bubble.

The tipping point will be whether growth from AI is sufficient to materially reduce debt to avoid a financial collapse that Dalio points out has always come to pass based on centuries of history. Dalio provided possible solutions in the way of mild tax hikes, reduction of fiscal spending, and lower interest rates known as the "3 percent solution" which aims to reduce the annual budget deficit-to-GDP ratio from around 7% to about 3%. This is seen as a pragmatic and historically proven target, last sustained in the U.S. during the 1990s. The question is whether the administration would reduce its fiscal spending or hike taxes. These two items remain doubtful if history is any guide. So with lower rates, government debt gets monetized and the financial bubble grows ever larger. Will AI be able to temper it?

The bottom line is as always price/volume action of major indices and leading stocks. So far, selling pressure outweighs buying pressure overall so continue to look for shorting opportunities as well as possible long opportunities in leadings sectors such as AI data center names. But keep stops tight as volatility remains elevated. And NVDA's gap higher at the open has reversed into a loss on volume at the time of this writing raising the odds of a major top in the markets.That said, global liquidity since 2008 has always come in to put major floors in markets as long as we dont have a tightening situation such as in 2018 and 2022 or the ending of various QE programs. Markets then marched to new highs every time. But also notice the V bottoms thus fear can create forced selling which offers entry opportunities for the nimble who have stayed on the sidelines or covered their shorts.

- Central banks have zero political willingness to let a smaller drawdown become a 50% crash when unemployment is still 4.4 % and the wealth effect keeps consumers spending.

- Every time markets wobble hard (March 2020, Nov 2022, Apr 2025 mini-crash, etc.), the reflex is the same via liquidity in all its forms.

- Result: Nominal prices get rescued again.

Bitcoin to $150k–$250k, S&P to 7,000–8,000, gold $3,500–$5,000+ are all on the table in the next leg if they open the taps.

2. Medium-term: The same medicine now feeds three very different beasts

| Cycle | 2009–2024 QE | Next Round (2025–202?) |

|---|---|---|

| Starting valuations | Cheap to fair | Nosebleed (S&P CAPE ~38, Bitcoin 7× its 2021 ATH, etc.) |

| Inflation backdrop | Deflation scare → 1–2 % CPI | 3–6 % entrenched + wage pressure |

| Growth backdrop | Depression or weak recovery | 2–3 % real GDP, full employment |

| Effect of new liquidity | Mostly asset reflation with tame goods inflation | Asset inflation + goods/services inflation at the same time |

| Currency impact | Dollar strong or stable | Dollar under periodic pressure (foreign holders diversify) |

- Inflation stayed low → Fed could shrink balance sheet slowly.

- Growth was weak → no political backlash to bailouts.

This time neither condition exists.

- If they let asset prices crack 30-40%, unemployment shoots up fast (wealth effect reversal + margin debt).

- If they rescue with massive QE again, CPI probably re-accelerates to 5–8 %+ quickly.

- Either path risks a 1970s-style stagflationary bust or a rapid loss of confidence in the dollar/reserve system.

That’s exactly Dalio’s point: the promises are now so large that the only two realistic endgames are: A) Controlled inflation (they let CPI run hot for years to erode the real debt burden) → great for Bitcoin/gold, bad for cash and bonds. B) Disorderly breakdown (they fail to control it) → currency crisis + wealth confiscation/revolution risk. Bottom line you can trade/invest with 2025–2027 (or whenever the next big liquidity wave hits):

- Yes → new nominal highs in risk assets and hard assets.

Bitcoin $200k+, gold $4,000+, S&P 8,000+ are plausible under another QE blitz.

- The party either ends in a monster inflationary blow-off (best case for Bitcoin/gold/stock holders)

or - A chaotic reset if they lose control of the dollar or politics fractures.