Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

The Evolution Will Not Be Centralized™

NVDA earnings bullish or bearish?

As I wrote in an earlier report, NVDA traded lower after earnings due to its data center revenue, crucial for AI growth, slightly missing analyst forecasts. Further, guidance did not provide the "blockbuster" upside that hyper-bullish investors were expecting. Nevertheless, CEO Huang noted demand is “extraordinary” for Nvidia’s new Blackwell chips. “Blackwell is the AI platform the world has been waiting for, delivering an exceptional generational leap — production of Blackwell Ultra is ramping at full speed,” he said in a statement.

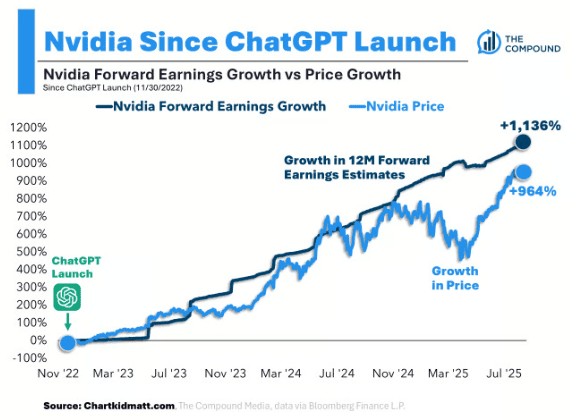

While some commentators have warned of froth, NVDA's returns haven’t actually kept up with its 12-month forward earnings estimates.

Here’s how Wedbush analyst Dan Ives put it: “With AI infrastructure investments continuing to grow with the company expecting between $3 trillion to $4 trillion in total AI infrastructure spend by the end of the decade, the chip landscape remains NVDA’s world with everybody else paying rent as more sovereigns and enterprises wait in line for the most advanced chips in the world.”

Nevertheless, we put out a report on NVDA as a short-sale possibility since it broke its 50dma. When it comes to trading, it's all about the set-ups, fundamentals be damned.

Golden central banking

Foreign central banks now own more gold than US Treasuries for the first time since 1996, marking a major global shift away from paper-based assets and toward hard assets like gold and, potentially, Bitcoin. Dollar debasement is the key reason especially since the dollar has been debased at a faster rate since 2020.

There are also geopolitical risks given aggressive US sanctions against adversaries which increases the risk that Treasuries can be frozen or confiscated.

The rise of Bitcoin alongside gold reinforces the shift toward assets not easily manipulated or printed, offering protection against inflation and central bank policies. Gold nor Bitcoin can be printed at will nor seized as easily. Meanwhile, Treasuries increasingly pay negative real returns when adjusted for inflation.

As confidence in traditional currencies declines, hard assets become more valuable. This trend reflects deep concerns about the global monetary order, and it’s likely to accelerate with gold and Bitcoin poised as preferred reserve assets moving forward.

Problematic bond yields

Nevertheless, expect turbulence ahead due to ongoing updates with President Trump’s tariffs and Japan’s bond market flashing warning signs with its 30-year at new highs.

This surge points to structural stress, policy uncertainty, and growing global risks, especially as Japan exits decades of ultra-loose monetary policy. Carry trades may unwind as Japanese yields become increasingly attractive compared to US and global counterparts which could trigger capital flight out of US Treasuries spurring higher yields on the longer end of the curve. These are yields not seen since 2008.

Interest rates are rising on the long end of the curve as the Fed prepares to cut rates later this month. The anomaly is due to deficit spending which is out of control. Another $200 billion of bonds was issued in just 5 weeks. US Treasuries require higher yields due to heightened perceived risk in holding them, classically symptomatic of the long-term debt cycle being in its late stages. With the recent purchase of Intel, US and other governments are now increasingly taking control of businesses and the economy. The part of the cycle that we are in is most analogous to the late 1920s but material gains from AI did not exist then, plus the Fed killed the markets by not utilizing QE until mid-1932, the point at which the Dow Industrials had lost 90% of its value, then New Deal laws further stifled productivity in the 1930s. Meanwhile, the labor market is weakening into rising inflation. This is further reason why gold continues to hit new highs.

It is a tug-o-war between weakening economies, inflation, interest rates, and global liquidity which tends to influence markets on a weekly to quarterly basis more than the first three metrics if history is any guide.