by Dr. Chris Kacher

Sidebar:

➼ Linktree is useful. For those who don't use it yet, see for yourself: https://linktr.ee/chriskacher

➼ My latest book in 2 parts (banned by Google et al because it goes against the mainstream narrative).

Nvidia (NVDA)

Nvidia (NVDA) dropped after hours because, although it beat earnings and revenue estimates, its data center revenue, crucial for AI growth, slightly missed analyst forecasts and overall results did not provide the "blockbuster" upside that hyper-bullish investors were expecting.

Data Center Revenue Miss: Nvidia's data center segment, the heart of its AI strategy, came in below market consensus, raising concerns about whether the turbocharged pace of AI demand is slowing or simply encountering temporary challenges.

Sky-High Expectations: After a massive run-up in price and bullish sentiment, even a very strong quarter was not enough to satisfy traders who had priced in extraordinary results, leading to profit-taking.

Conservative Guidance: While Nvidia’s Q3 forecast was positive, it wasn’t far enough above consensus to reset investor expectations higher, spurring some disappointment.

Sector-Wide Reaction: Other AI and chip stocks dropped in sympathy (AMD, TSMC, Broadcom, SMCI), as investors reevaluated the pace of AI spending and chip sector momentum.

Fed's track record

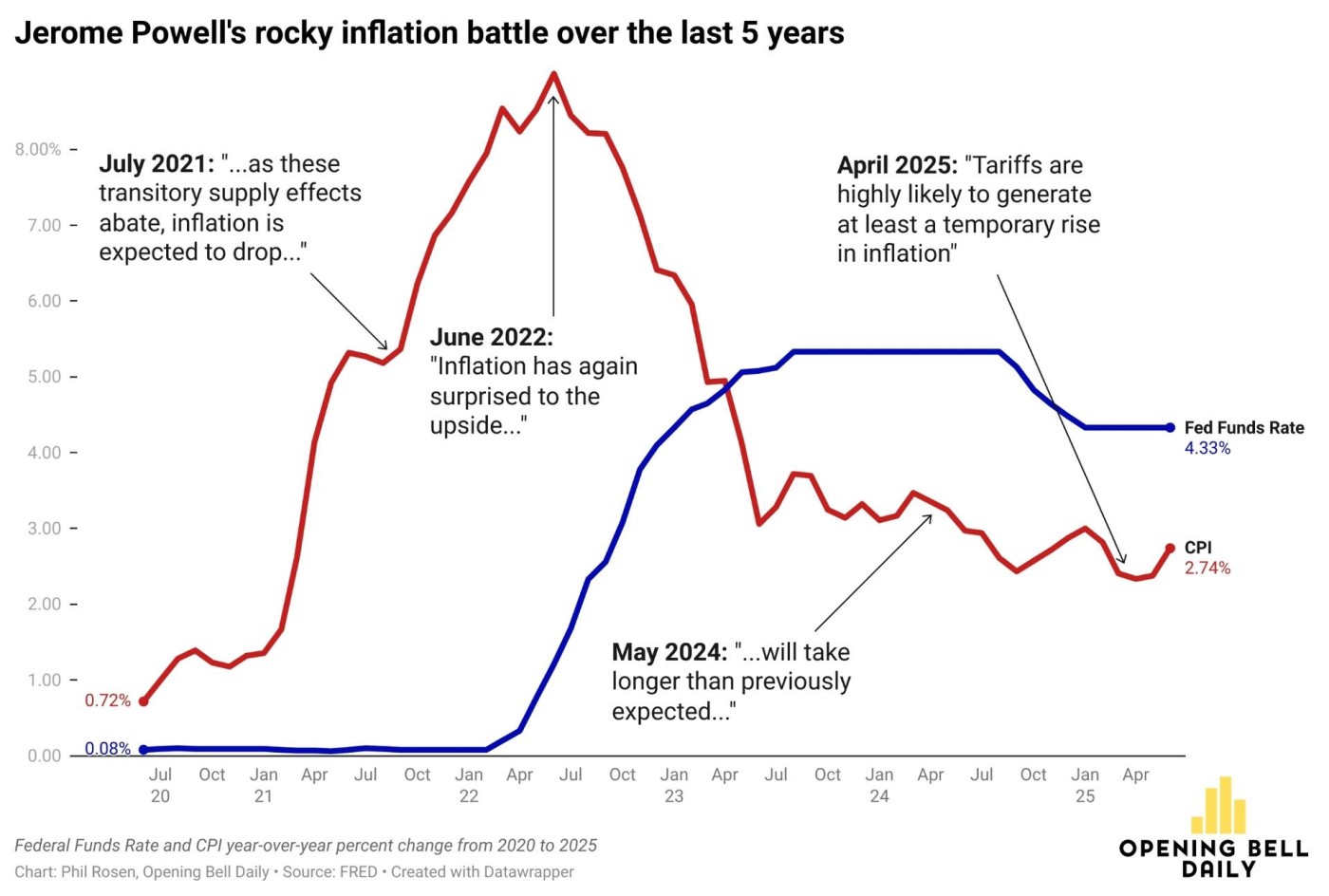

The Fed's track record on inflation has been poor.

Powell was dead wrong when he said he expected inflation to drop in July 2021 after an unprecedented amount of quantitative easing that began in March 2020 due to Covid. Then he was actually surprised in June 2022 when inflation kept coming in hot. Meanwhile, we had advised members as early as November 2021 that the Fed had changed their tune about QE so tightening lay ahead.

Two narratives clash over a rate cut, each with different takes on recent economic data. On one side, the bulls see enough signals flashing red: GDP crawling forward at just 1.2%, consumer spending losing momentum, payroll growth stalled. To them, the 4.2% unemployment rate masks real fragility. With core inflation dropping toward 2.5%, they argue the Fed is now running the risk of breaking the labor market further and locking housing affordability into crisis mode. These advocates want an immediate move, arguing it will give equities and housing some relief, with room to step back if inflation rears up again.

The bears, meanwhile, aren’t buying it. They warn any easing could spark a rebound in inflation, pointing to July’s jump in producer prices and sticky services costs. While job growth appears limp, they say the labor market still looks robust by historical standards, and slower growth isn’t synonymous with weakness. Instead, they highlight structural risks the Fed can’t ignore: persistent fiscal deficits, inflated asset prices, and questionable valuations. For them, higher rates are the anchor against instability. Cut rates too soon, and they see a replay of past mistakes: stoking bubbles, undermining credibility, and risking another bout of runaway inflation.

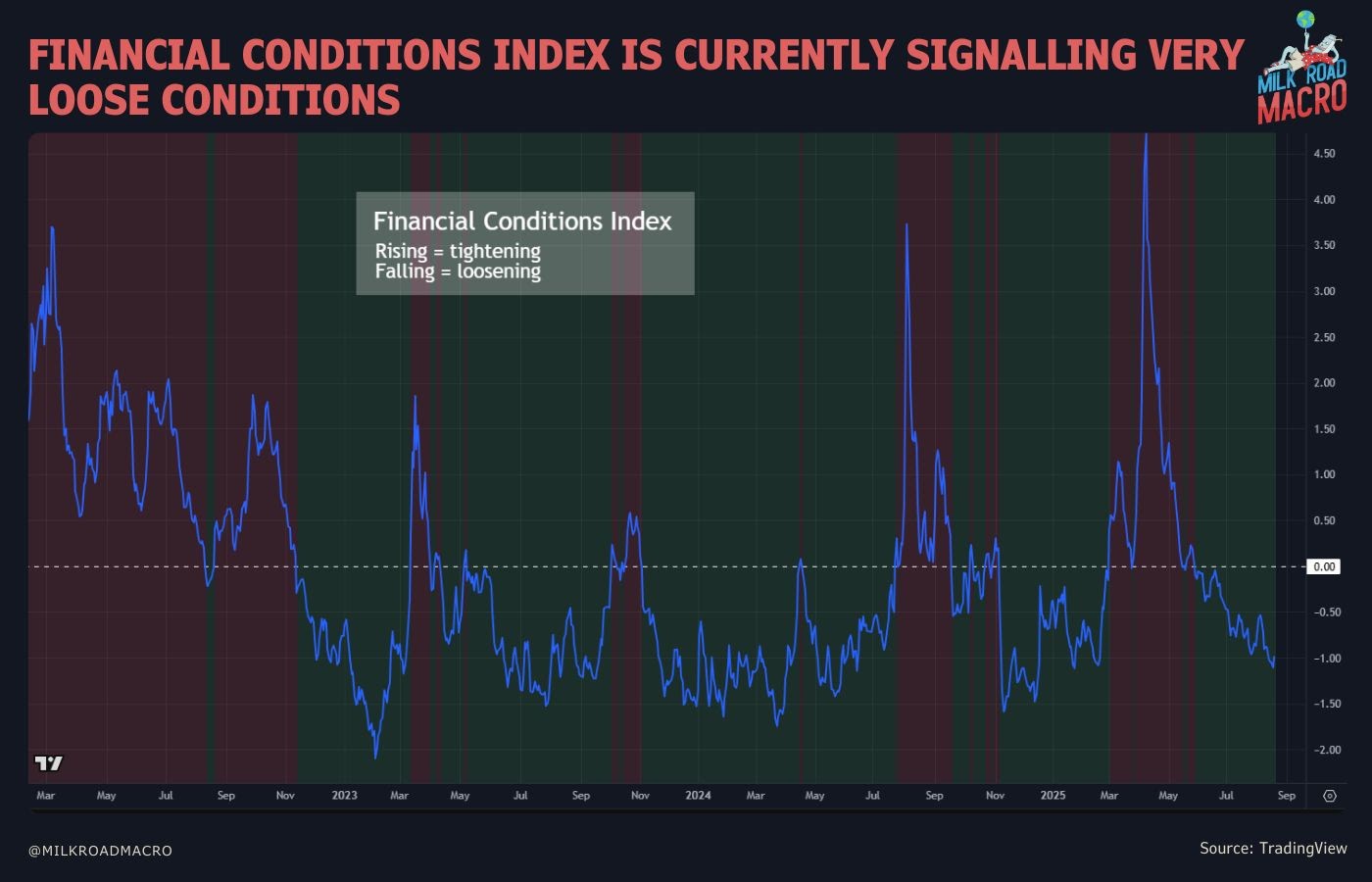

One key metric favors the bulls: global liquidity. With US and China pumping QE into the ecosystem, markets should continue to head higher overall with the occasional 3 steps forward, 2 steps back. For example, after Trump shocked markets in early April with far steeper tariff proposals, markets mini-crashed but then quickly shot to new highs over the ensuing weeks. Global liquidity played the major role.Global liquidity

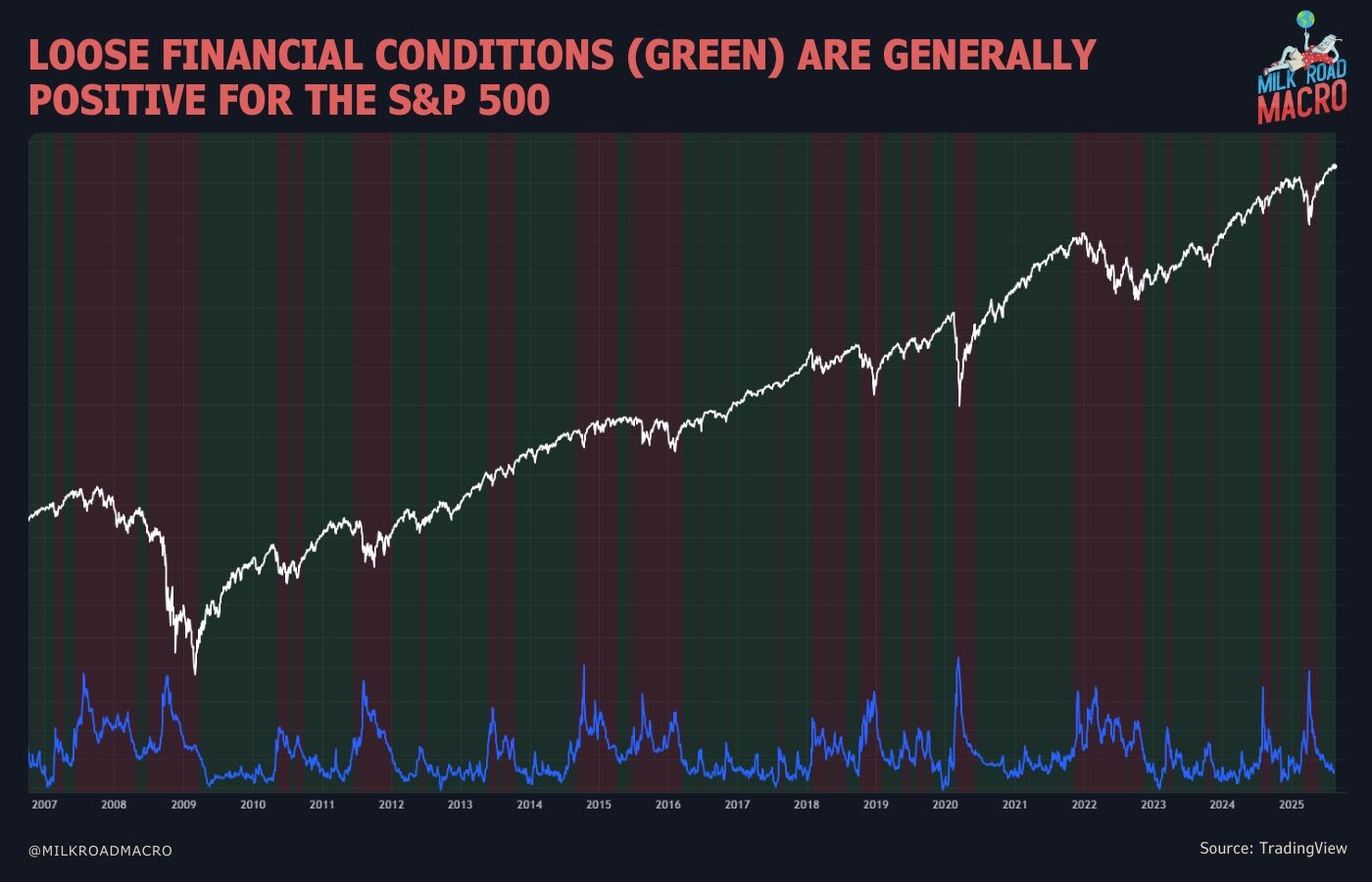

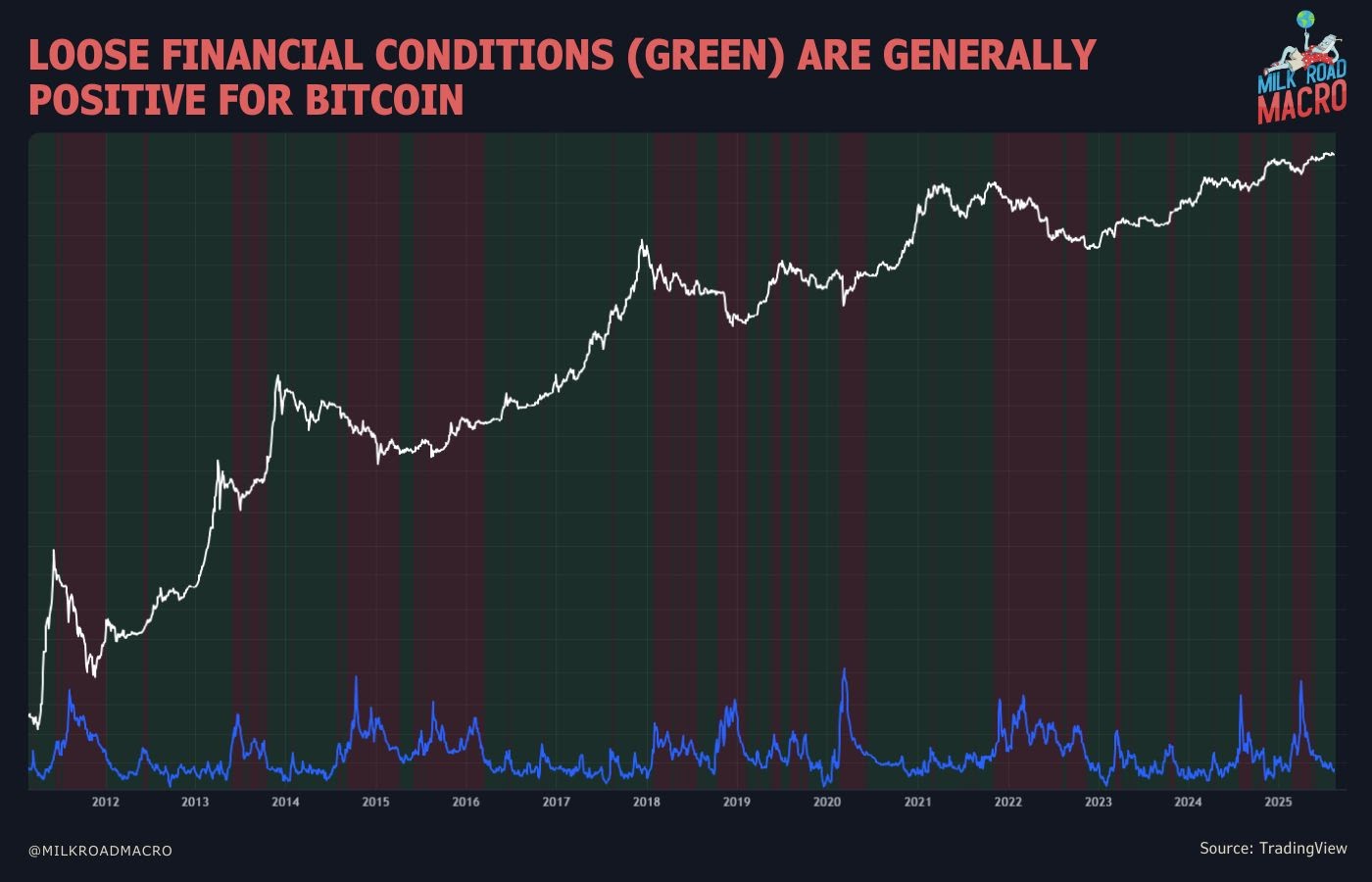

Financial Conditions Index measures M2 money supply, central bank operations, bond yields, commodity prices, and institutional capital flows which indirectly measures the global liquidity. It is currently showing loose conditions.

It correlates well with the S&P 500 and Bitcoin.

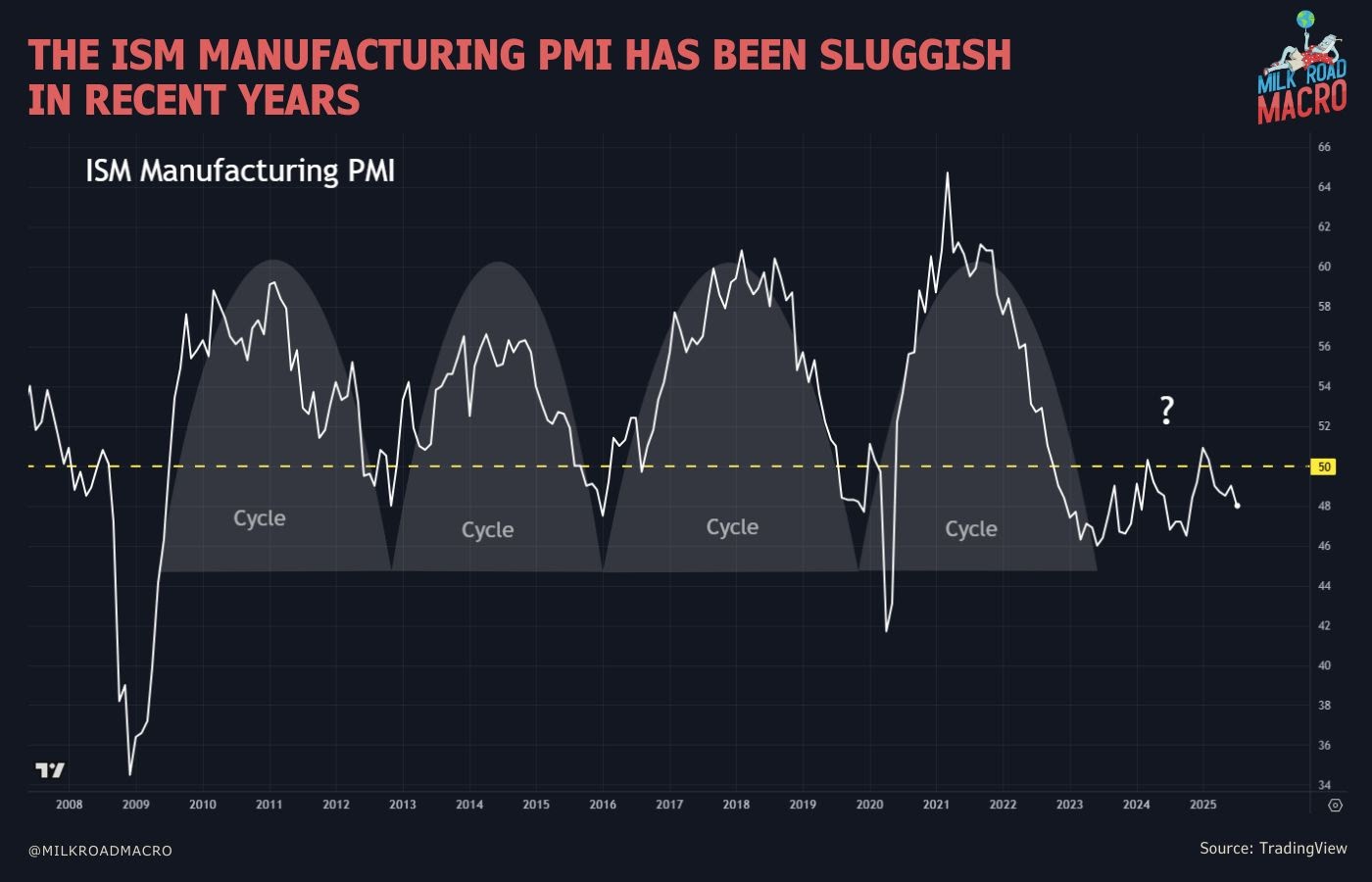

The ISM Manufacturing PMI (Purchasing Managers Index) is not showing the cleaner cycles that we have seen in previous years, making it difficult to assess exactly where we are in the business cycle. This continued in its most recent print with a disappointing 48 meaning the manufacturing sector is still in “contraction” since it is below 50.

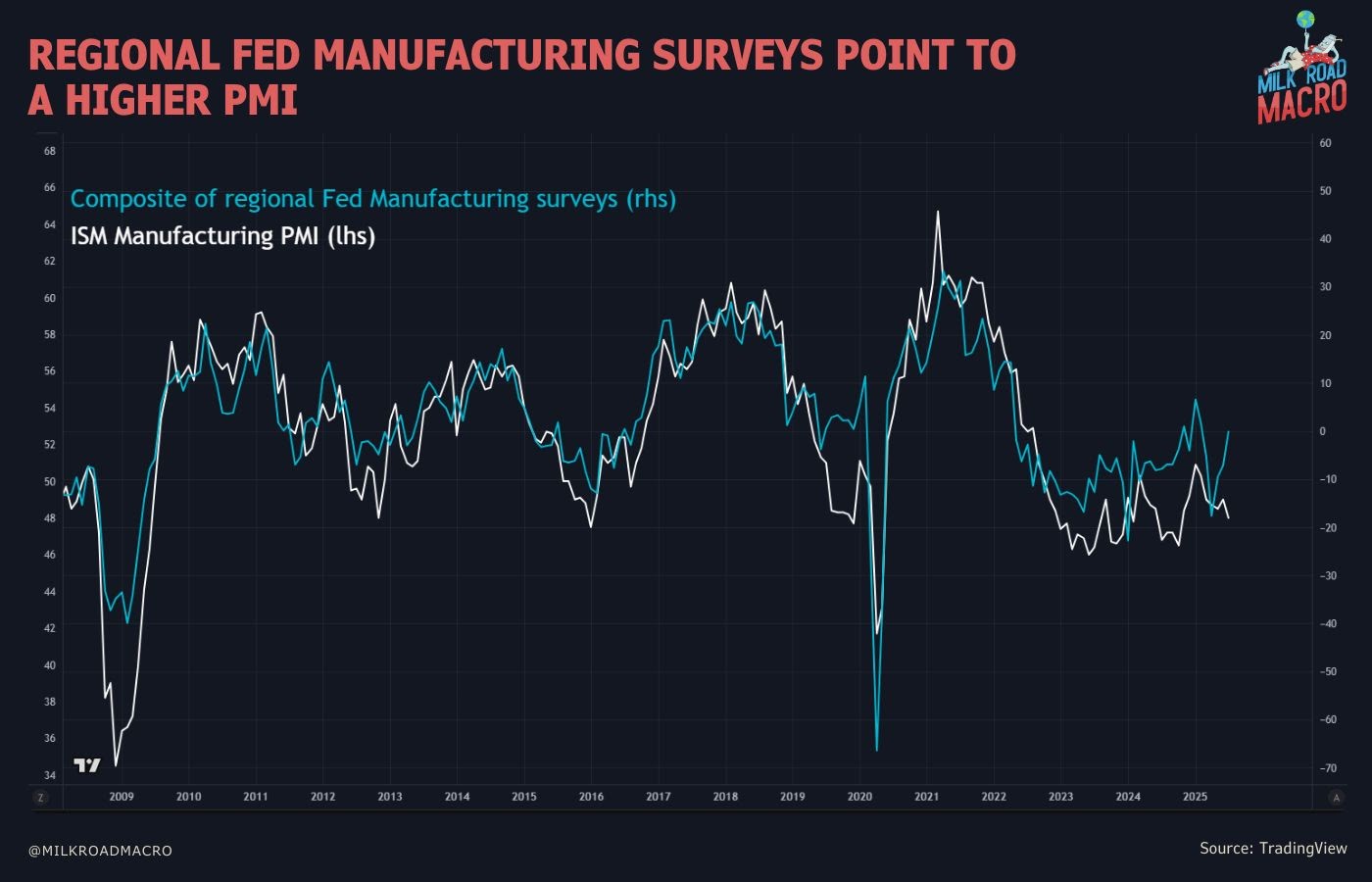

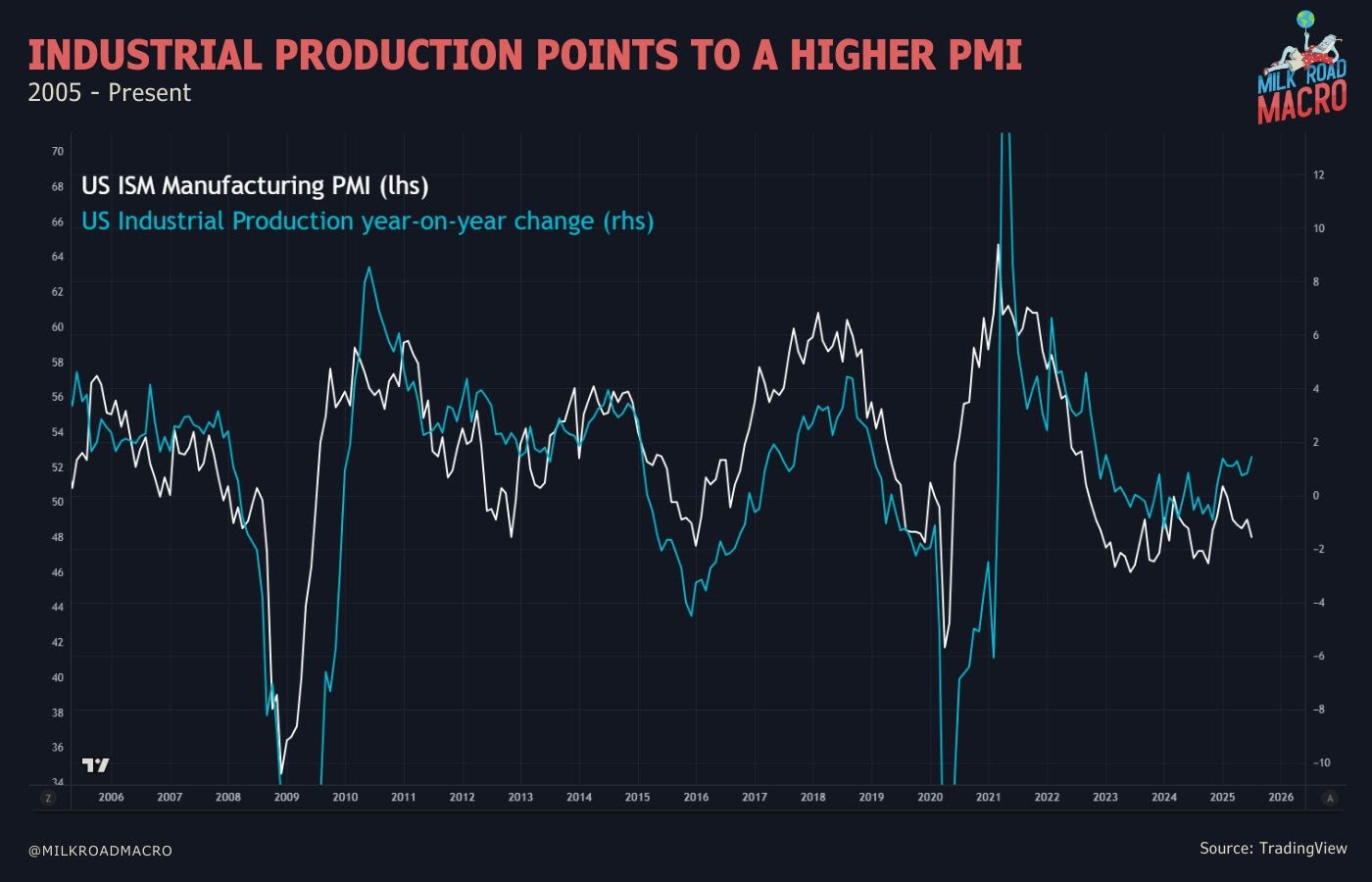

But regional fed manufacturing surveys and industrial production both suggest a higher ISM ahead.

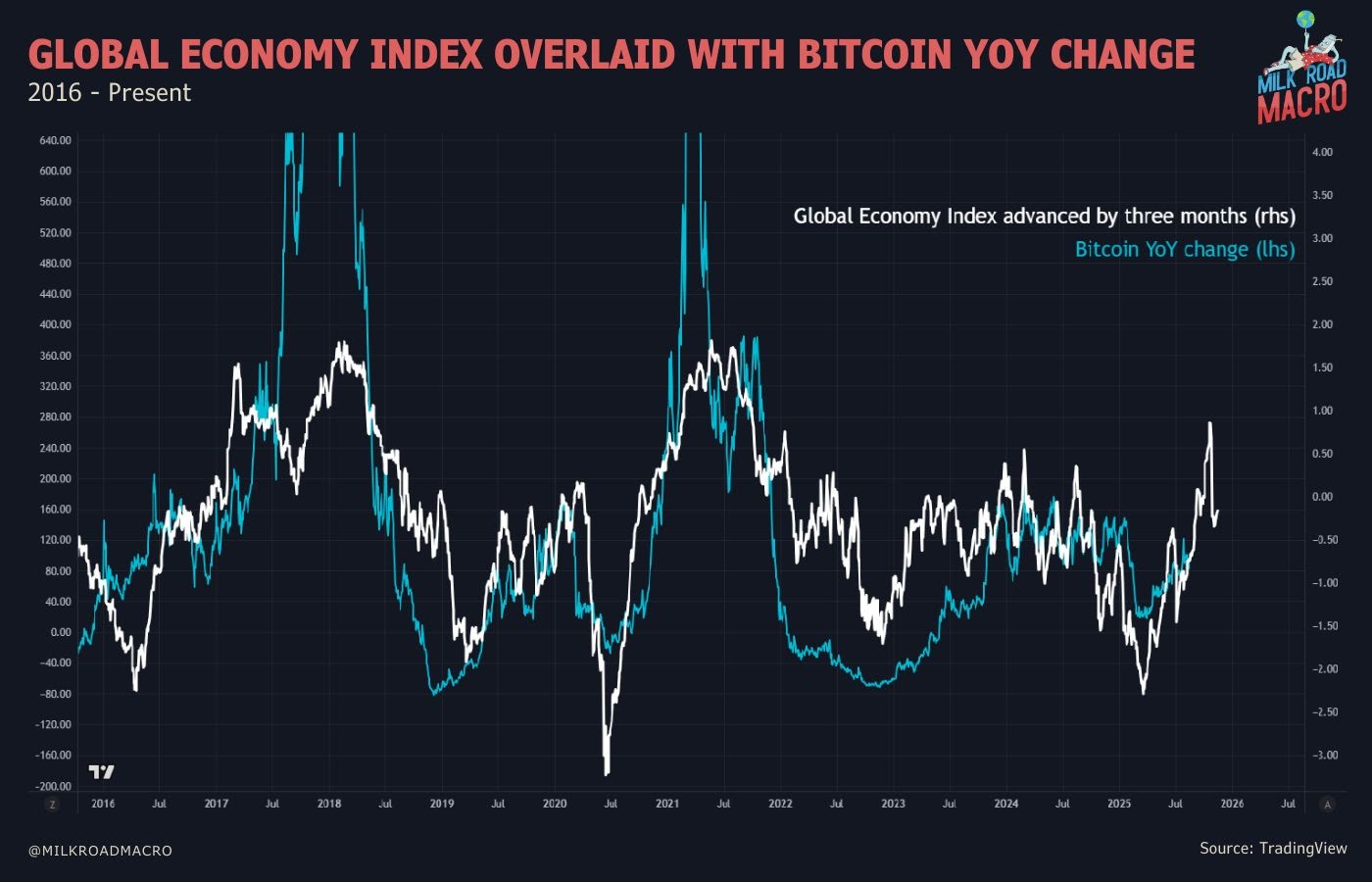

The Global Economy Index (GEI) which tracks currencies, bond yields, commodity prices and freight rates (shipping costs) is also showing continued strength in Bitcoin and thus likely stocks.

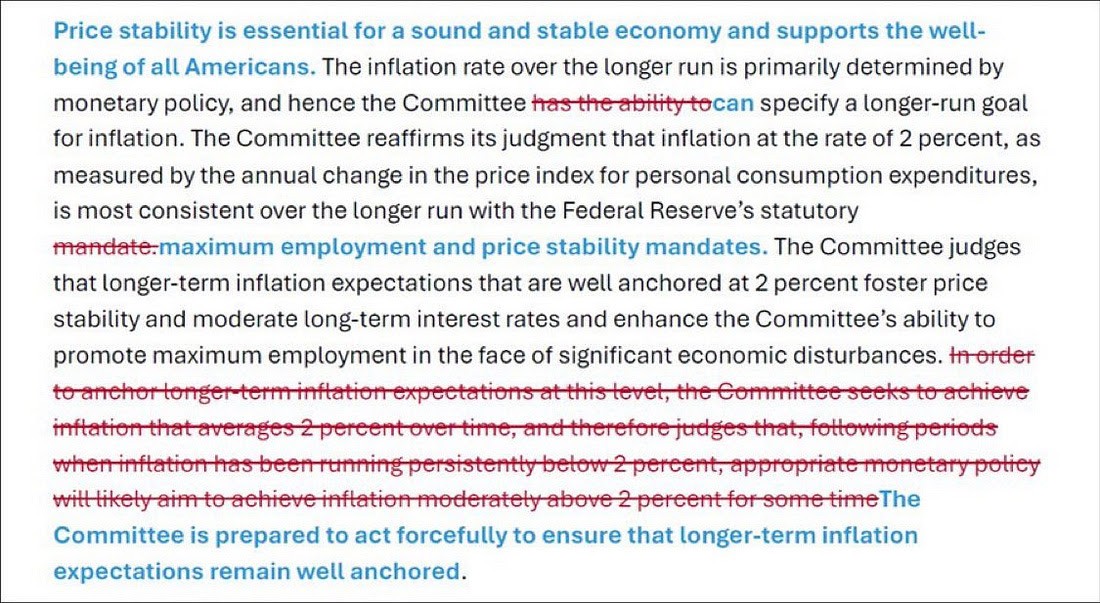

And lower rates are coming given the text replacement in the recent Fed statement where they removed the 2% rate of inflation target and replaced it with "The Committee is prepared to act forcefully to ensure that longer-term inflation expectations remain well anchored."

Bitcoin bull over?

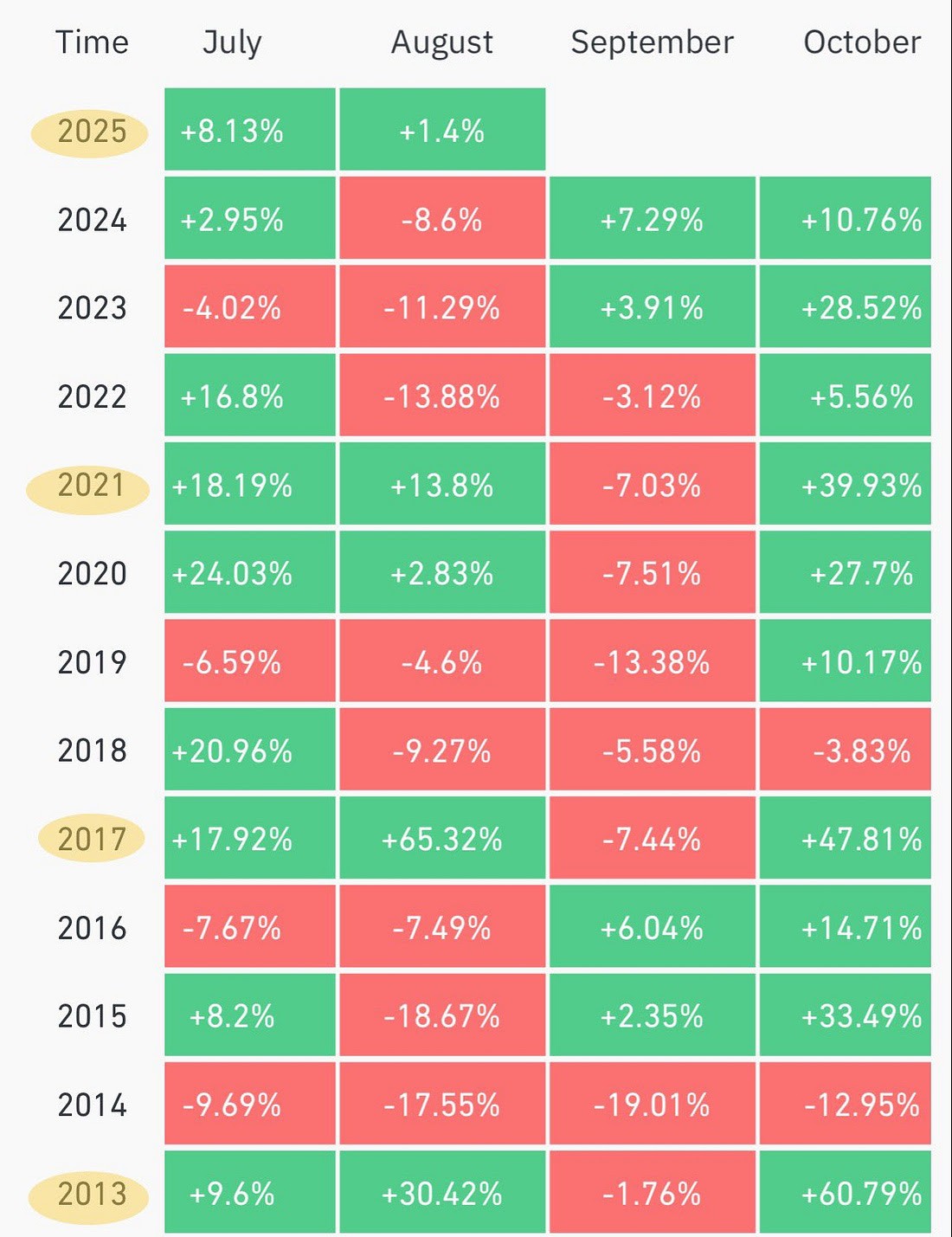

Given the above, Bitcoin's bull still has a bit to go before it tops. Keep in mind that August and September tend to be the weakest months for Bitcoin with October being one of the strongest.

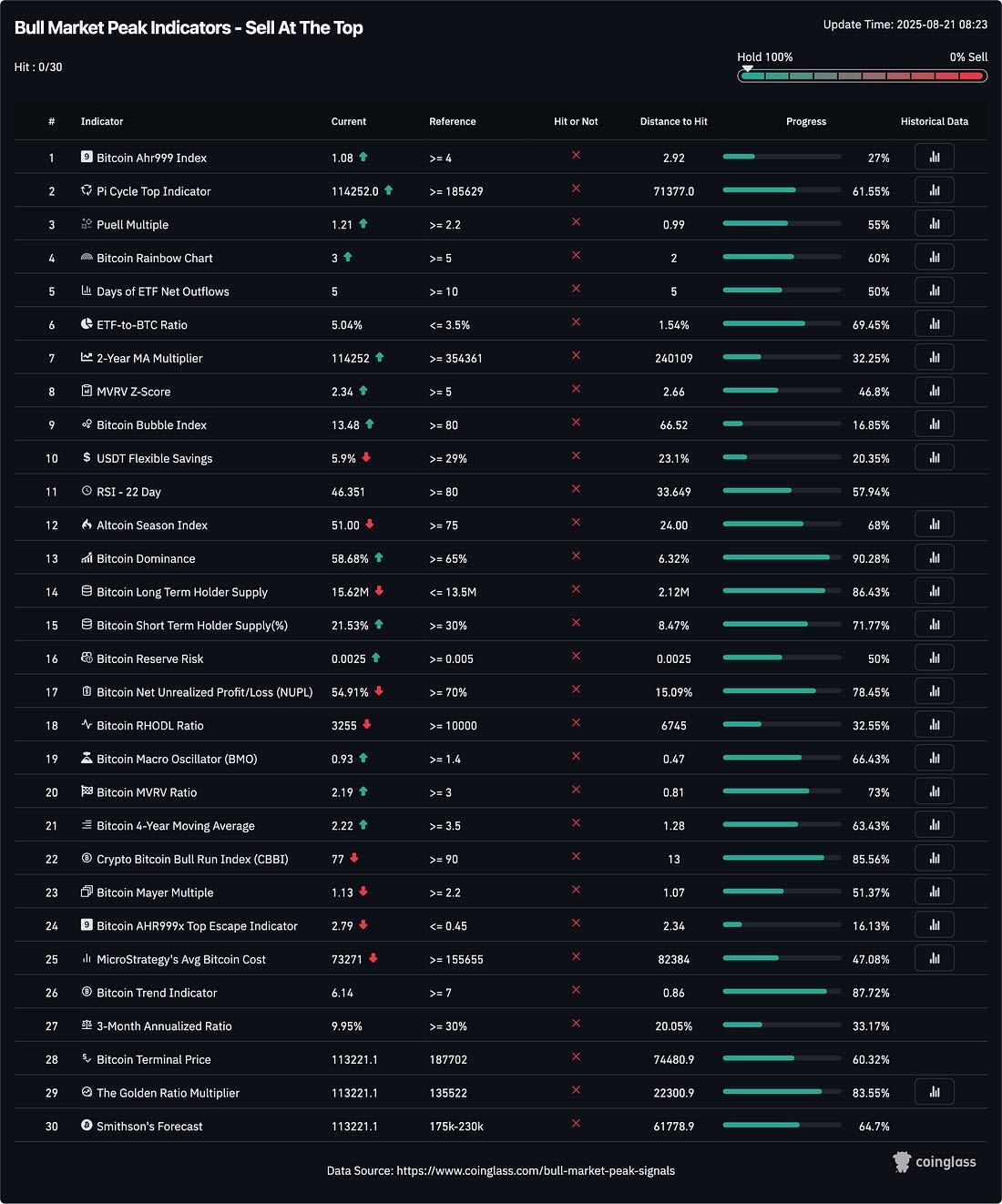

Plus, it is hard for the bull market in Bitcoin to be over given that none of its 30 market peak indicators have been hit.

Further, a significant shift happened in Bitcoin’s ecosystem post-2024 halving. For the first time, the amount of BTC held for 10+ years is growing faster than new coins are mined. An average of 566 BTC per day are moving into this long-term category, compared to 450 new BTC issued daily. This signals strong conviction from these long-term holders.

Bitcoin was created specifically to function without reliance on central authorities or government control, using cryptography and peer-to-peer technology to maintain a censorship-resistant, borderless monetary system. While regulated products like spot ETFs, these simply offer greater market access and validation, not fundamental changes to the protocol or its purpose. I think the government's buying of Bitcoin recalls to mind the saying, "If you cant beat 'em, join'em."

Shorter term, Bitcoin remains in a correction and September is traditionally a weaker month for Bitcoin as noted in the table above.