by Dr. Chris Kacher

Rising yields bullish for bitcoin

When bond prices fall making yields rise, it signals weak demand for government debt and growing concerns about fiscal stability, inflation, and the sustainability of national deficits. US government bonds were recently downgraded for a third time by a major credit rating agency. This erodes the traditional perception of government bonds—especially US Treasuries—as the ultimate “safe haven” asset. The US’s ballooning debt and persistent deficits are making Treasuries less attractive and less reliable as a store of value.

As confidence in sovereign bonds wanes, investors seek alternative stores of value that are less dependent on government policy or fiat currency stability. Bitcoin, with its fixed supply and decentralised nature, is increasingly seen as a “politically neutral” safe haven. It has been called digital gold. Bitcoin is benefiting from institutional inflows and even state-level reserves are forming as it matures into a macro-hedging instrument.

Further, rising bond yields make borrowing more expensive and reduce the present value of future cash flows, hurting long-duration assets like tech stocks and private equity. However, this environment can paradoxically benefit bitcoin, as investors rotate out of both bonds and equities and into assets that are less correlated with the traditional financial system. Bitcoin is hearing the bond market’s distress signals and attracting capital as a result.

Foreign holders such as Asian central banks are unwinding their US dollar reserves, reducing artificial demand for Treasuries and pushing rates higher. Foreign bonds are also becoming more attractive. The unexpected rise of Japanese inflation pushes their yields higher which reduces the attractiveness of US Treasuries. Japan alone holds ~$1.1 trillion in US debt. Over in Germany, plans to issue €1 trillion+ in new debt over the next decade to fund infrastructure, defense, and climate initiatives are at hand. German 10-year yields spiked 43 basis points in one week, the largest jump since 1990, narrowing the gap with US Treasuries. This makes German bonds increasingly attractive over US Treasuries. These structural changes further undermines the dollar’s “privilege” and strengthens the case for investing into non-sovereign assets like bitcoin.

Institutional investors are increasingly viewing bitcoin as a hedge against systemic risks in the fiat-based financial system, especially as the traditional correlation between bonds, stocks, and commodities breaks down. Bitcoin’s recent all-time highs have coincided with some of the worst bond auctions and credit downgrades in US history.

Falling bond prices are bullish for bitcoin because they reflect a structural loss of confidence in government debt and fiat monetary systems. As yields rise and traditional safe havens falter, bitcoin’s role as a decentralised, scarce, and politically neutral asset becomes more attractive to both institutional and retail investors. This dynamic is helping drive capital flows into bitcoin, supporting its price even as traditional markets face turbulence.

Deadly musical chairs?

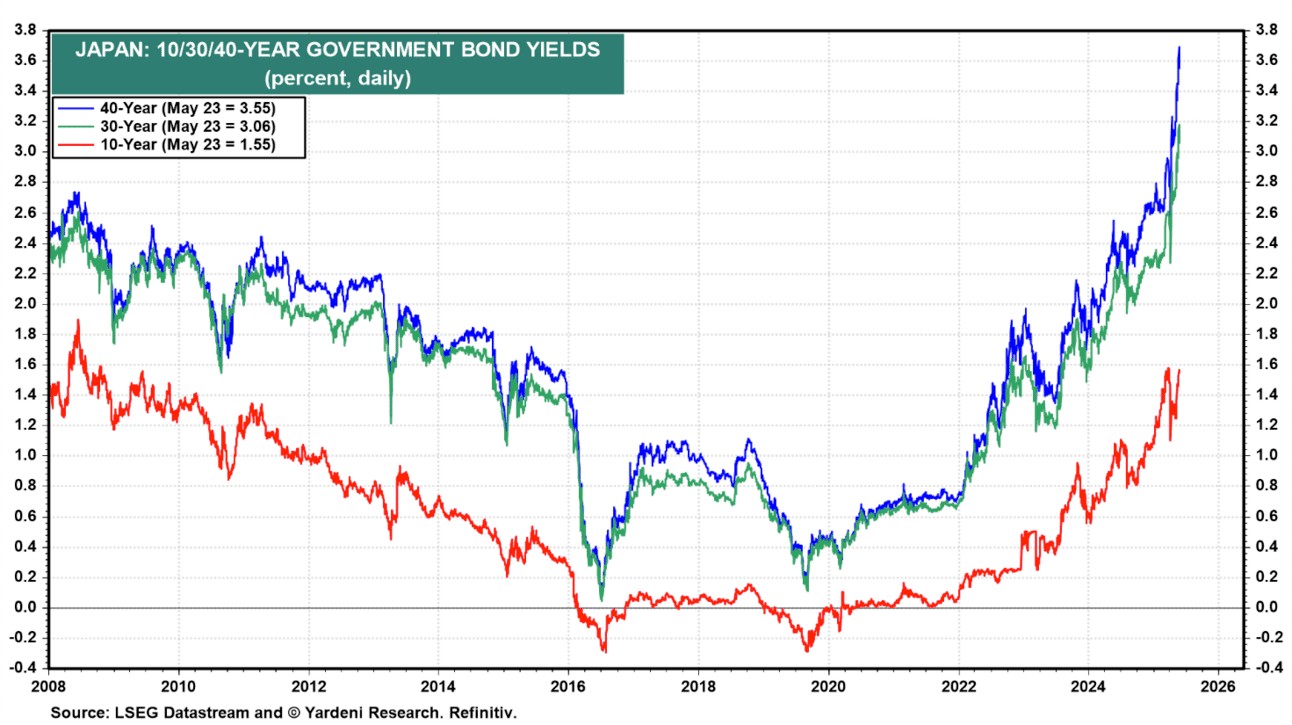

US bond prices may continue to fall due to Japan monetizing its $7.8 trillion debt at record levels. Japan has a dilemma. If it keeps buying its bonds via QE, its currency weakens and inflation rises. If it stops buying via QE, then yields spike, debt becomes expensive, and its banks suffer. At present, we are seeing its bond prices stage a minicrash. Japan’s 30-year bond yields rose above 3% to the highest since 1999 while Japan’s 40-year bond yields hit 3.6%, a record high. There is also the issue of overall falling demand for its debt due to worsening fears over fiscal stability. Such is higher risk in a nation like Japan, where domestic investors and the central bank own over 80% of the bonds. Rising yields in Japan mean global investors could soon demand higher yields everywhere else.The US — with a sizable portion of its debt held by foreign entities — could be even more vulnerable to market tumult. Today, Japan is the largest foreign holder of US debt, with more than $1.13 trillion in Treasurys. But if Japanese yields keep rising, that capital may flow out of US bonds and back to Tokyo. If sharply higher Japanese bond yields entice Japanese investors to return home, the unwinding of the carry trade could send stock markets lower. We are monitoring surging Japanese bond yields on the long end closely.

If global investors (or central banks like China’s) slow their buying of US Treasuries or increases its selling, the US must raise rates to attract buyers. Higher rates = higher interest payments = bigger deficits. Or the US must buy its own bonds to keep yields down. $10 trillion in debt must be rolled over by July so it is essential to keep yields down, but the recent US credit downgrade is another headwind. But China's hands are also tied so its buying and selling should remain in balance. On the other hand, if overall foreign demand for US Treasuries dries up, the Fed has to step in with QE which means more inflation.

The system is tightly connected. We are living through a slow-motion sovereign debt crisis.

Global interest rates thus global liquidity are largely tied to the US and Japanese bond markets. They must grow their way out of this fiasco via cutting edge technologies such as AI which quantum jump productivity across individuals, corporations, and governments. QE funds the torrential growth of AI compute as capital finds its way into the Magnificent 7. The acceleration of QE thus global liquidity will remain an unstoppable force so expect more inflation as well as higher stock, bitcoin, and real estate prices. The balancing act between countries is delicate, like walking a tightrope, but increased productivity via cutting edge technologies may help the world get to the other side.

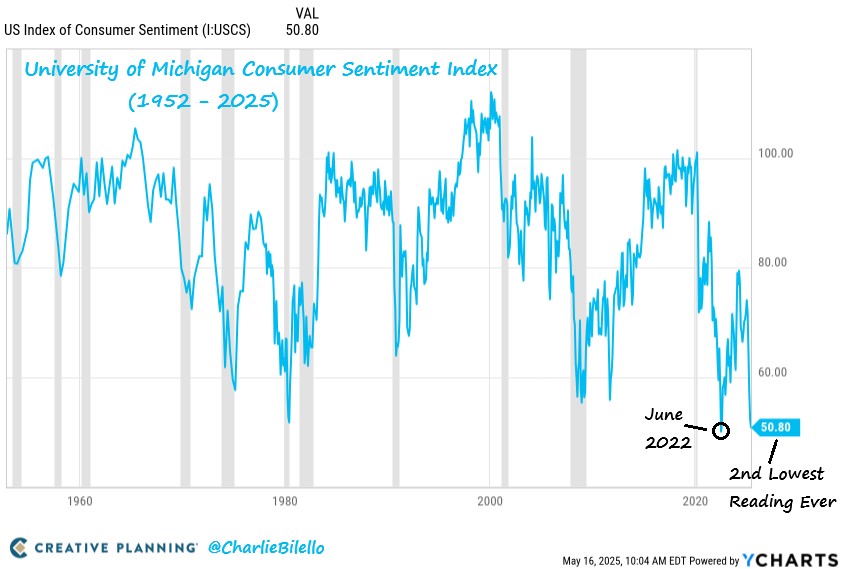

Consumer sentiment near all-time lows

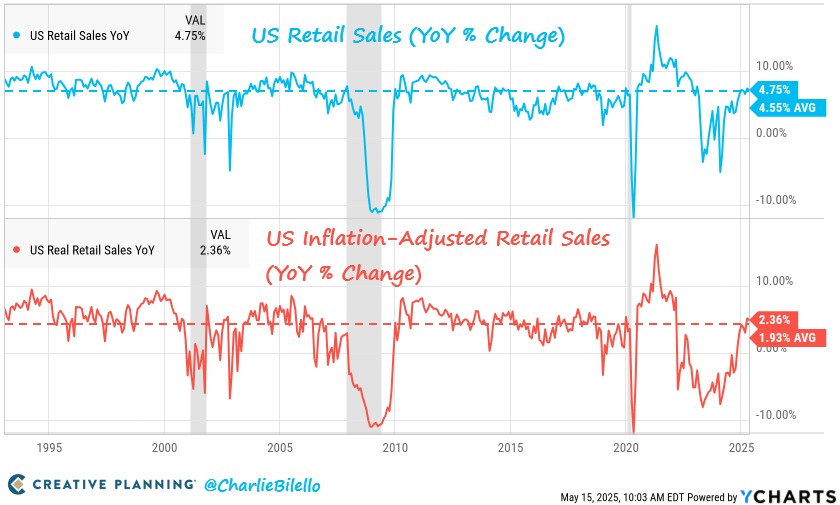

Meanwhile, retail sales are up 4.8% while consumer sentiment crashes? Classic disconnect. The inflation disaster in 2022 forced families to spend more just to keep up—gas, groceries, utilities. Adjusted for inflation, real sales growth is a pathetic 2.4%. The University of Michigan’s sentiment index stands at 50.8, the lowest since 2022. Real wages are stagnant, savings drained, and every trip to the store feels like a robbery for many.

NVDA earnings

While some analysts warned that Wall Street may underestimate the impact of US export restrictions on Nvidia’s China sales, and CEO Jensen Huang recently called the ban “deeply painful” with up to $15 billion in lost sales, Nvidia’s earnings soared in after-hours trading Wednesday after it reported blockbuster numbers that surpassed expectations and, crucially, an upbeat forecast that brushed off US-China tensions. This was a departure from the company’s recent string of post-earnings slumps. Wall Sreet believes the AI trade can still outrun geopolitics.

Adjusted EPS: $0.96, versus $0.93 expected

Revenue: $44.06 billion, up 69% year-over-year, versus $43.31 billion expected

Data center revenue: $39.1 billion, up 73% year-over-year, just under estimates

Even when accounting for $8 billion in lost China sales, Nvidia projects $45 billion in revenue for the next quarter. The street nonetheless is acting like Nvidia’s $45 billion revenue forecast is a lowball estimate.

“Global demand for NVIDIA’s AI infrastructure is incredibly strong,” CEO Jensen Huang said in a statement. “AI inference token generation has surged tenfold in just one year, and as AI agents become mainstream, the demand for AI computing will accelerate.”

Indeed, US hyperscalers like Microsoft, Amazon and Meta are spending billions on Nvidia products to fuel their AI ambitions. The latest numbers don’t point to anything like a slowdown.

“Countries around the world are recognizing AI as essential infrastructure — just like electricity and the internet — and NVIDIA stands at the center of this profound transformation,” Huang said.”