Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

The Metaversal Evolution Will Not Be Centralized™

On rate hikes...

At the most recent press conference, Powell wants a slower pace of tightening but at a higher terminal rate. Yet the terminal rate of 500-525 bps is where more "stuff" starts to break. Powell also said we dont need inflation to come down to slow pace of increases, but the historical record warns against premature loosening.

The Fed wants to avoid a repeat of the 1970s at all costs when the Fed did not raise rates sufficiently to break the back of inflation. Powell has said, "We cannot do what we did in the 1970s because we would just have to have a bigger downturn at the end of this to get inflation out of the economy."

This underscores what Fed member Esther George said: Household savings buffers "may allow them to continue to spend in a way that keeps demand strong. That suggests to me we may have to keep at this for a while. You may see the terminal fed-funds rate higher and have to stay there longer."

Further, employment costs rose at a firm pace in the third quarter. Such occurred in the 1970s where the price of services increased due to higher wages which resulted in a wage price spiral as higher wages forced higher prices. The concern back in the 1970s was that they would repeat the 1930s, a period of the worst recession on record, so instead, the Fed didn't hike rates sufficiently in the 1970s which resulted in persistent inflation with low growth or stagflation.

What could make the Fed less hawkish is housing and used cars which both soared in price have been coming down, and supply chain bottlenecks are improving; it takes time for these factors to show up in the reported inflation data. We also currently have a rising rate of delinquencies which will continue to increase as rates go higher. Part of this is due to soaring monthly payments of home mortgages as the 30-year rate has more than doubled in 2022. In addition, personal saving rates are at all-time lows of 3% while consumer loans including credit card debt are almost at $1 trillion. Meanwhile, median real wages fell -7.7% over the last two years.

Nevertheless, watch for wage inflation in upcoming nonfarm payroll reports. The one reported today puts the current estimate at 0.3% MoM. Also watch for the expected number of jobs being added to exceed the estimates of 205k and the unemployment rate to come in around estimates of 3.5%. This would cue the Fed into staying the course as concerns the higher terminal rate.

When asked what the Fed will do if they overtighten, Powell said they have tools to support economic activity, ie, they will just have to print more which would launch QE5.

CME Fed Futures

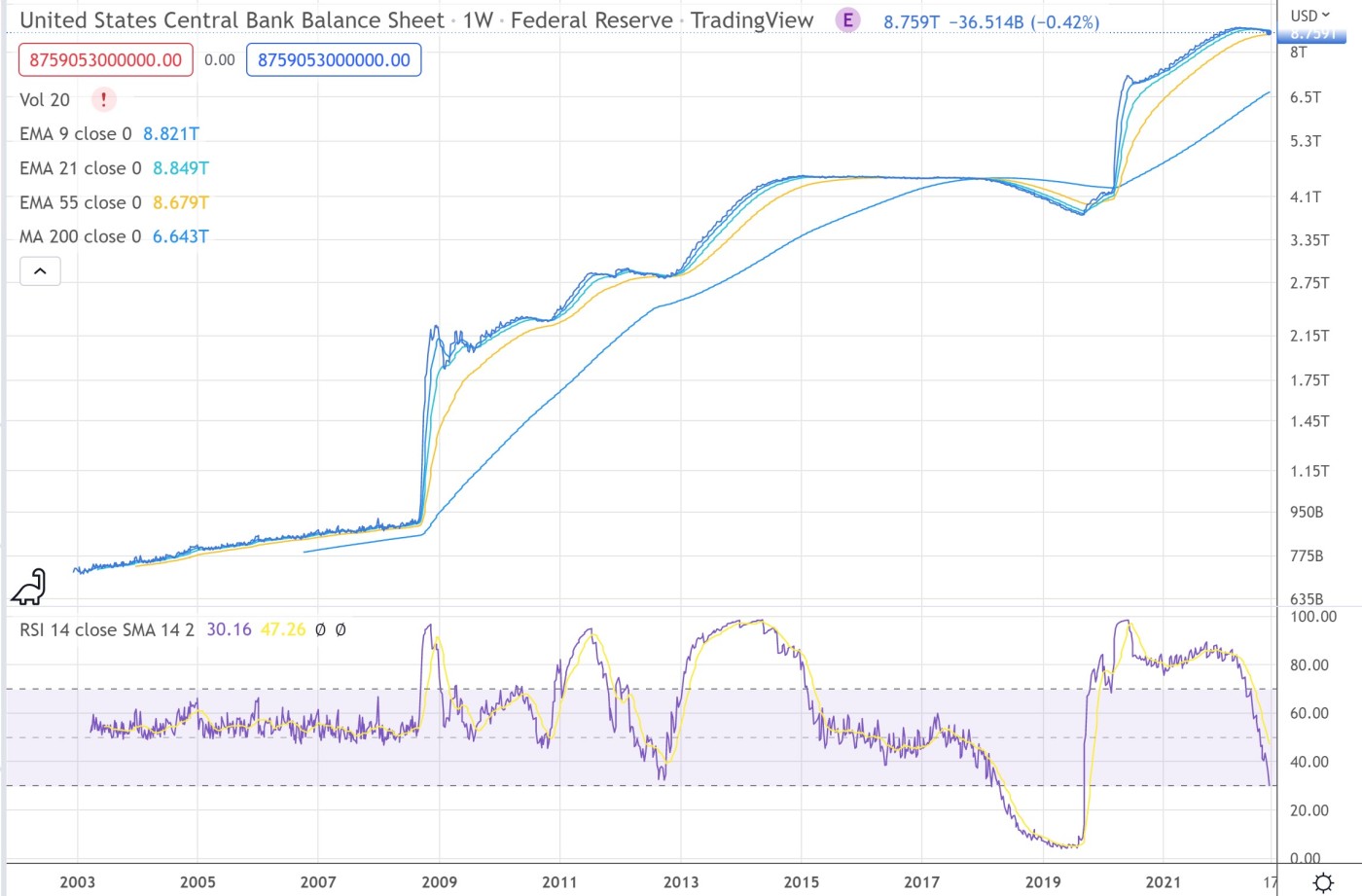

CME Fed Futures is projecting another 75 bps hike in Dec, then two 25 bps hikes in early 2023. This would put the FFR at 500-525. No bueno given record levels of debt. COVID more than doubled the Fed's balance sheet, so the Fed has to tighten to at least 475-500 bps if it even hopes to reverse the amount printed due to COVID by 1/3 to 1/2. Instead, it is far more likely a next crisis will spur a raft of quantitative easing before they even get close to these levels. Notice in the image below how the Fed's balance sheet never materially decreases. The Fed tried their best in 2018 but that brought on the first Christmas crash on record to where the Fed had to step in and promise that it would stop tightening its balance sheet; that marked major lows in both stock and crypto markets.

The Fed has no choice to continue to hike aggressively if they hope to combat supply-side inflation which is far more vicious than demand-side inflation. Supply-side inflation is brought on by supply chain disruptions due to political sanctions and COVID among other second order effects.