by Dr. Chris Kacher

A Legend Passes

Our former mentor, the legendary investor Bill O'Neil, has passed. When Gil and I wrote our first book, the title intentionally included "Trade like an O'Neil Disciple". I read Bill's investment classic "How to Make Money in Stocks" in 1990, a year after it was published. It set me on course for years of success in the markets. In graduate school at Berkeley when I was working on my Ph.D. in the nuclear sciences, despite our successes in creating the first atom of element 110 and confirming element 106 which we had the privilege of naming Seaborgium, I knew my heart was in the science and art of investing. So a year before graduating, I literally started having dreams about working for Bill. I used to say I would sweep his floors just to get my foot in the door to work for him. Instead, he said he would start me at the bottom so I could learn how the company's products were put together. He said if I proved myself, I would be quickly promoted. He was true to his word. I still remember the first day I started at his company, January 22, 1996. I am fond of saying it was the last day I ever worked in my life. It is a true gift when one can do what one loves. Work then becomes play as creativity flows naturally while emotions remain in control. The investment world has certainly lost an icon that will be missed.

Failure to raise the debt ceiling has never happened

All this worry about the US defaulting on its debt is a broken record. The US has never defaulted on it's debt from a failure to raise the debt ceiling. Congress has already authorized the governments budget. The circus tends to get resolved at the last minute with both sides claiming victory as the mainstream media whips up worst case scenarios that have never happened. One other issue is also guaranteed. The US will continue to print money in the coming years. The question is when, not if, a black swan hits, how much will the Fed be forced to print?

In principle, it looks as if a deal to raise the debt ceiling has been reached. In consequence, the Treasury will be able to increase their General Account balance, or TGA which will reduce liquidity substantially. Those banks with sufficient reserves to buy newly issued Treasuries will do so, thus drawing monetary liquidity from the banking system.

Fed balance sheet - TGA (treasury general account) - RR (reverse repo) = LiquidityOn top of this, after Friday's PCE report, Fed Futures now places odds on another 25 bps rate hike when they next meet in June and one 25 bps rate cut in Nov-2023 to bring the final target rate to 500-525 by the end of the year. Of course, this is data dependent so should inflation remain elevated due to supply chain and other issues, the Fed may be forced to hike more than once this year.

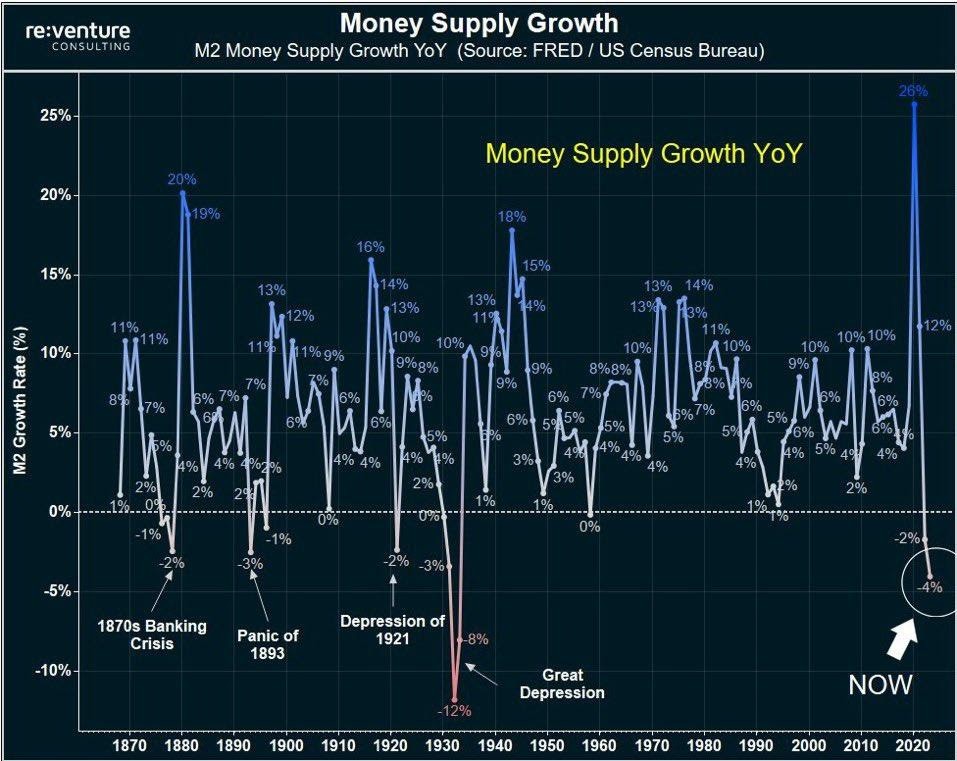

As of Q1 2023, M2 growth is down to -2.6% YoY, its largest decline since the Great Depression which coincided with the Dow Jones Industrial Average down -90%. But then, the Fed never printed so much money in such a short period of time due to the pandemic.

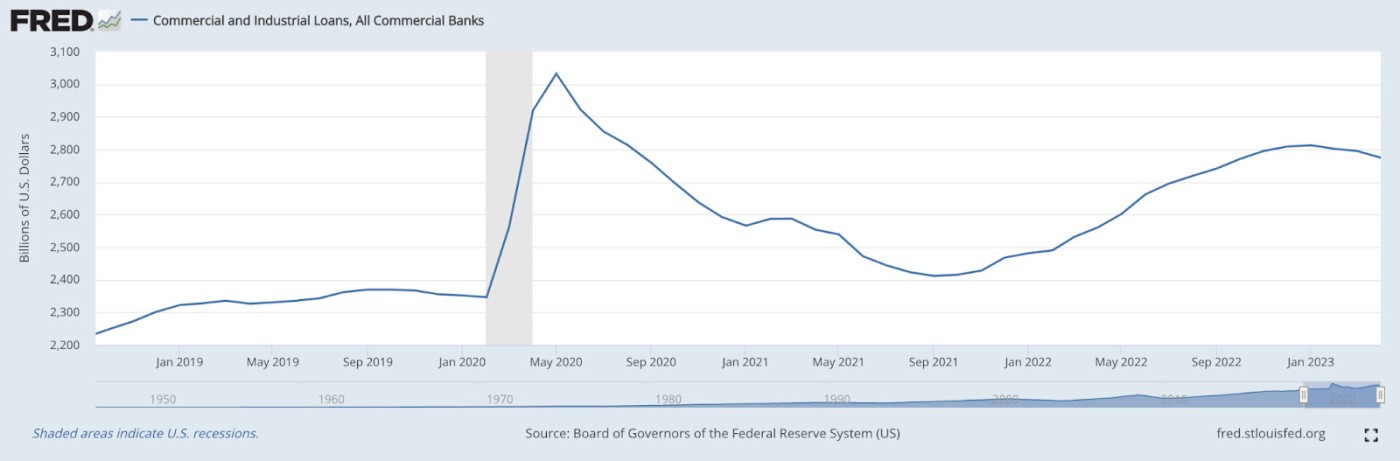

Bankers have clearly foreseen the serious reduction in monetary liquidity so have tightened credit conditions in recent weeks as the amount of commercial and industrial loans outstanding from US banks has been declining since the start of this year. Credit worthiness has steeply declined since rates have been hiked over the last 14 months. In consequence, banks have now begun to offer less credit to businesses and consumers.

All of these factors boost the odds of a recession sometime later this year or early next though the counterbalance is the exponential growth of cutting edge technologies such as AI and Web3. We also saw a recent upside adjustment to GDP, and the Purchasing Managers Index has shown signs of economic conditions improving in the US, coming in at 54.5, well above estimates of 50.0. Growth was driven primarily by the services sector, though this adds fuel to some Fed members' arguments that services inflation remains problematic thus more rate hikes are necessary.

Rip tides

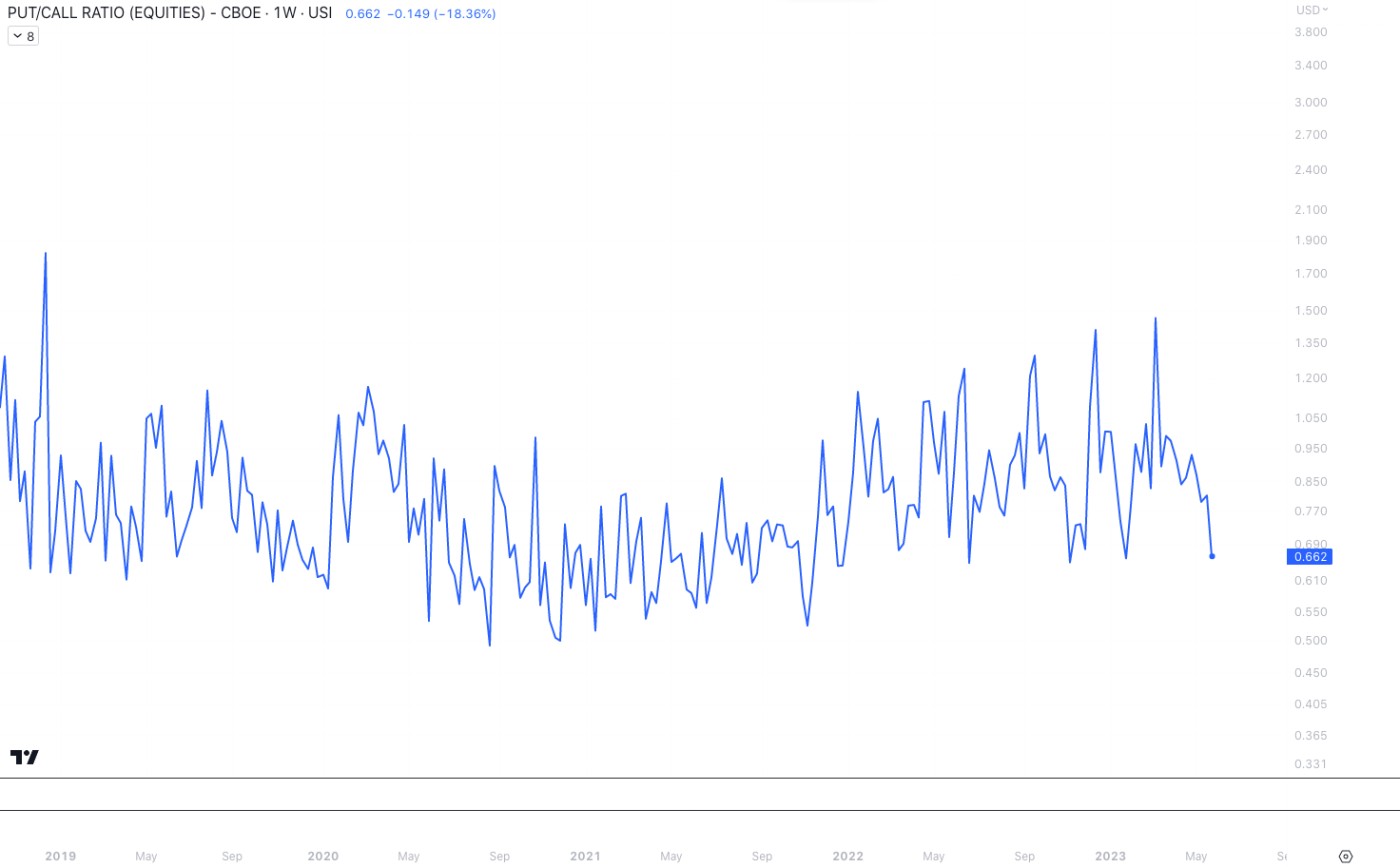

So with liquidity likely to drop once the debt ceiling is raised due to soaring TGA, markets are likely to follow to the downside. But we also have big tech beating earnings such as NVDA and AMD due to the AI craze. This has created a bifurcated market where most names are lagging except for big tech. But the equity-only put/call ratio has dipped down to 0.66, its lowest level since the market began its rally in January, so a pullback in tech-centric indices is likely sooner than later after the FOMO dies down.

In relation to FOMO, the former CEO of Sun Microsystems Scott McNealy made a statement to Bloomberg just after the dot-com collapse:

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate.

Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

Indeed, stocks trading at more than 10x sales have well underperformed the S&P 500 over time. NVIDIA ($NVDA) is now trading at 38 times its revenue (P/S = market cap/last 4 qtr sales).

Lack of liquidity in crypto

Stablecoin liquidity has fallen as their onramps are affected due to lack of banking partners in the US. The two largest stablecoins correlate loosely with the direction of the crypto markets. Both have been in overall downtrends since May 2022 with more or less sideways but insubstantial upside moves this year.

In addition, market makers Jane Street and Jump Trading having largely retreated from crypto trading in the US as a regulatory crackdown on the industry has intensified. Jane Street is scaling back its global crypto expansion plans, while Jump Crypto is pulling back from US markets, although it's still planning to expand internationally.