by Dr. Chris Kacher

AI and decentralization

AI has been a topic of discussion and research since the advent of computers in the mid-20th century. However, it's only in recent years, nearly seven decades later, that AI applications have become genuinely useful to hundreds of millions of people. AI is currently in the midst of a rapid adoption phase, similar to the steep curve of a hockey stick.

For AI to function effectively, it requires access to data. If this data becomes compromised due to a single-point vulnerability, or if the central entity storing the data changes access rules or pricing, an AI system relying on this storage entity becomes vulnerable to failure. This presents a significant existential risk, which is why I advocate for the use of decentralized storage solutions by AI systems.

Large cloud data service providers like Amazon are vulnerable. As a massive centralized company operating under human jurisdiction, it does not align with the requirements of an AI for its data hosting. Amazon could, under government pressure, cut off access to data unilaterally. This situation is infeasible in a censorship-resistant decentralized network. I'm aware that blockchain technology, with its consensus mechanisms and economic incentives, can facilitate coordinated data sharing. That's why I see the decentralized data storage network powered by Filecoin (FIL) as a necessity for the growing AI industry. Crypto companies such as Golem (GLM) offer decentralized computing power but are relatively smaller and may face challenges in a bear market. That said, we remain in a bear market so such coins remain highly vulnerable.

Bond yieldsBonds are selling off and yields are rising on a future expectation of the expanded US expenditures on peripheral wars. The US will spend whatever is necessary on arms to support Israel’s war effort. Ray Dalio pointed out the world is at the same timeframe as it was two years before WW 1 and two years before WW 2. Indeed, America’s military budget is set to explode especially since the current geopolitical conflicts may spread. This will increase future government borrowing, and the sky's the limit when it comes to the sums of capital a war can waste.

Bitcoin and gold are rallying as long-end US Treasuries fall. While a spot Bitcoin ETF being approved started the run higher in price, this is Bitcoin discounting a very inflationary global world war situation. The question remains as to how much additional money printing will be required. This will depend on the geopolitical situation. If war spreads, then more money will be needed. There is going to be an orgy of money printing in the near future as part of an attempt to inflate away the massive amount of unproductive sovereign debt. This is where stealth QE/liquidity arises.

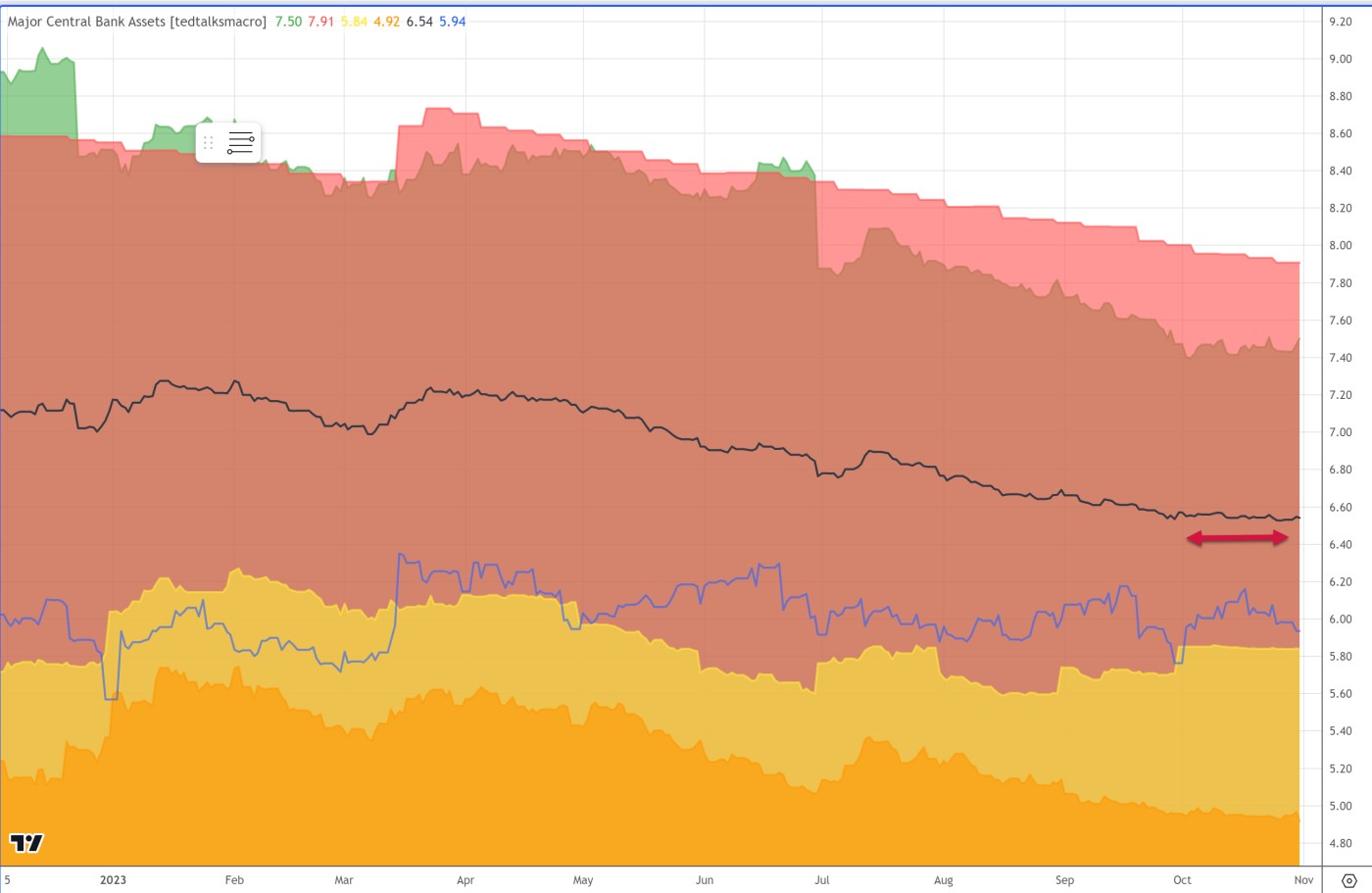

We will keep track of US and global liquidity to monitor any material increases which would be bullish for markets. For now, global liquidity which had been on an overall downtrend has been flatlining over the last month. The national debt stands at over $33.5 trillion. When you throw in future entitlements that have been promised, we are looking at over $100 trillion. To prevent a collapse in pensions and IRAs, the Fed will have to print even greater sums than we saw during COVID.

Inflation

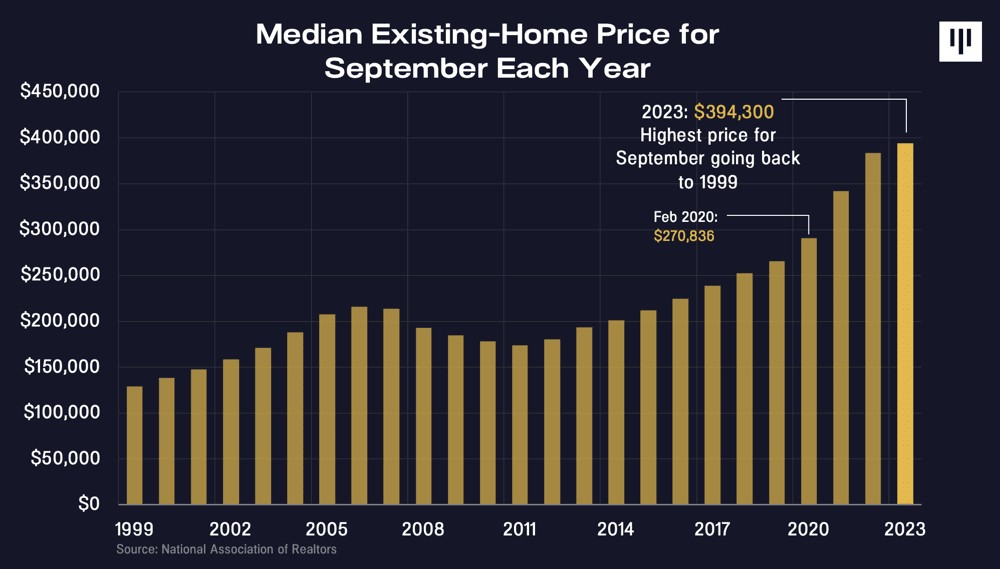

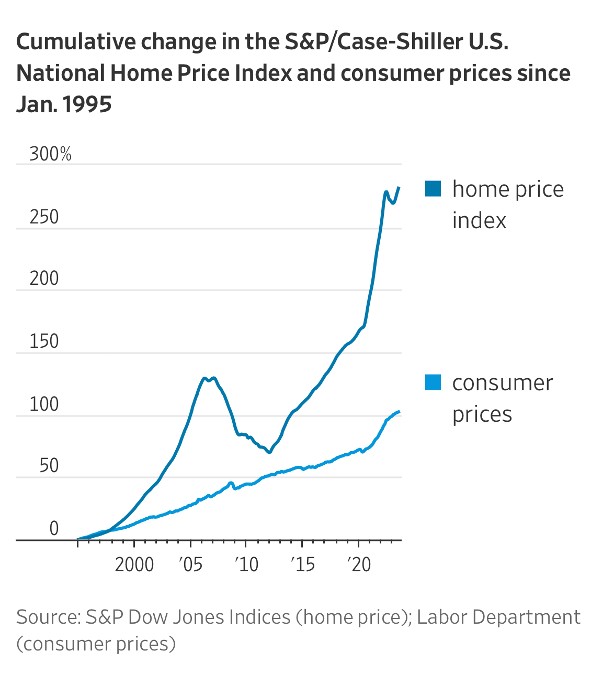

In the meantime, inflation remains an issue with all the items that people require to live- food, energy, housing, and transportation. For housing, the Owner’s Equivalent Rent measure takes two years to fully pass through, so even if houses stayed stable for the next two years, the CPI would still rise 1.1% just because of previous housing increases over the last two years in the pipeline, according to the Atlanta Fed. Thus, the S&P/Case-Shiller US National Home Price Index is still hitting new record highs.

Home prices also hit new highs in 2023 when everyone expected they would cool.

Housing is the single largest expense. The Fed manipulated the mortgage market such that the price of shelter rose 2.5-times as much as the general inflation index of which 32% is housing.

Core inflation is 4.4%, more than double the Fed's target 2%. Wage inflation is at 4.5% and increasing as PCE services component came in above expectations. Rates could stay elevated for much longer than people think. When rates were falling, the average P/E in stocks was roughly at the same level compared to today when rates have been rising. This suggests stocks are at a valuation extreme. Stocks dont have sustainable bull markets when tight money policies are prevalent.

Over the last decade, stocks were relatively cheap. There were many times in the past decade that equity earnings yield was more than 4% above bonds because bonds were overvalued as rates plummeted. Today, the earnings yield on equities is below that of treasuries. Bonds are no longer overvalued while stocks are hugely overvalued.

Fed Chair Powell was dovish in his testimony, saying the September "dot plot" that suggested one more rate hike this year is less relevant as its efficacy decays with time. Powell did reiterate rates would stay "higher for longer" as their 2% mandate remains in effect.The duration of market chop will be determined by persistent inflation across key goods which will keep rates at elevated levels vs. liquidity from extended wars, debt interest payoffs, and future entitlements.