by Dr. Chris Kacher

Powell's bullish testimony

The Bank of England and the Fed lowered rates by 0.25% and Fed Chair Jerome Powell gave markets plenty of reason for optimism:

Rate hikes are not anyone’s “base case”, policymakers maintain an easing bias, GDP expected to ramp up, and unemployment seen holding steady.

This underscores how AI is boosting GDP, and unemployment has risen gently due to big tech companies doing more with fewer employees, but not due to a weak economy. Markets rallied on the news.

The last 22 times the Fed has lowered rates with the S&P 500 within 2% of record highs, stocks have been higher 12 months later 100% of the time. So the fears that rate cuts lead to recession is only based on two data points (2008 and 2020) but both years were caused by exogenous one-off events which tanked the economy. Cycles in 1984, 1995, and 1998 eased policy without a subsequent recession.

New highs ahead?

Productivity from AI, rising earnings growth, and fiscal stimulus from the Big Beautiful Bill underscore higher highs ahead for markets, black swans notwithstanding.

Stocks: all-time high

Home Prices: all-time high

Gold: all-time high

Money Supply: all-time high

National Debt: all-time high

CPI Inflation: 4% per year since Jan 2020, 2x the Fed’s “target” though today's core CPI puts inflation at its lowest level since March 2021 (2.6% vs 3.0% est) underscoring supply-side deflation due to AI

Fed: cut rates again & restarted QE in its various forms with QT having ended Dec 1.

We also have supply-side deflation due in part to tariffs and a surge in deportations.

GDP should remain strong due to easy monetary policy, QE in all its forms, technological innovation like AI, and deregulation. The explosion of innovation and investment from Silicon Valley contributes to more than 60% of GDP growth.

The Fed quietly flipped from QT back toward balance‑sheet expansion. Its December 10 directive authorizes new “reserve management purchases” of Treasuries, starting with about $40B a month in T‑bills and possibly notes out to three years to “maintain an ample level of reserves.” In plain English: QT is effectively over, and QE will start grinding higher again.

This is fiscal dominance in action. With structural deficits and heavy Treasury issuance, the system can’t tolerate a true reserve squeeze, so every time stress appears as it did during the 2019 repo, 2020 COVID liquidity panic, and 2023 bank backstops, the Fed is forced to step in as buyer of last resort, even when it says it wants tighter conditions.

The destination is clear: a permanently larger Fed balance sheet and a central bank that is once again a structural buyer of government debt. Call it QE, “reserve management,” or something else, the label matters less than the reality that the central bank is returning as a structural buyer of Treasuries, allowing the government to spend into the system without drawing from the system.

In the meantime, AI fears of overcapacity are real but the data suggest the bubble will likely continue to grow. Stay tuned for the report on arguments from both the bullish and bearish camps.Benign inflation for both Truflation PCE and Truflation US Inflation Index

Truflation PCE:

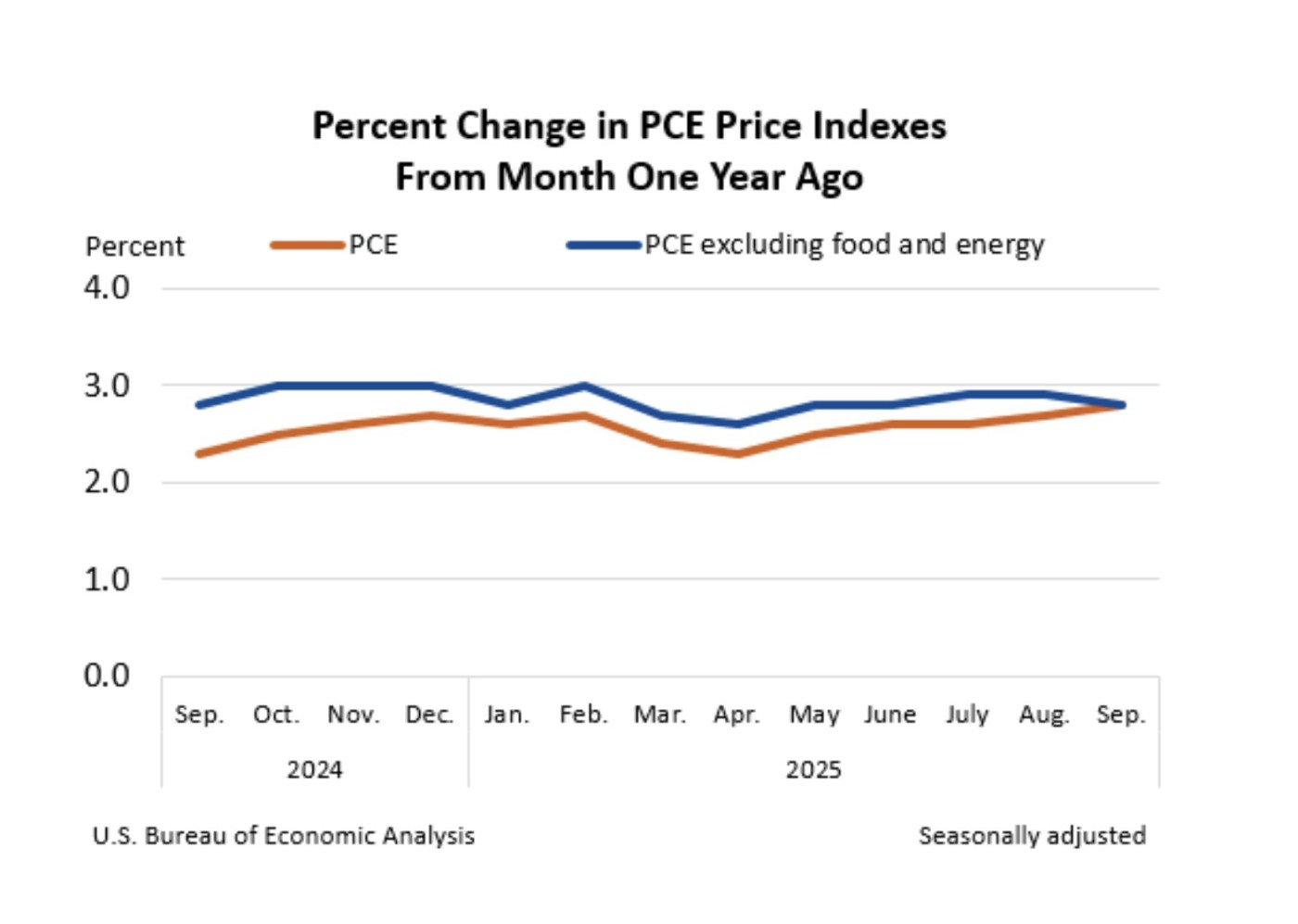

September PCE: 2.8% (previous 2.7%, expected 2.8%)

September Core PCE: 2.8% (previous 2.9%, expected 2.9%)

October inflation data was cancelled. Meanwhile, Truflation has been reporting daily PCE data using independent data sources which shows inflation is falling.

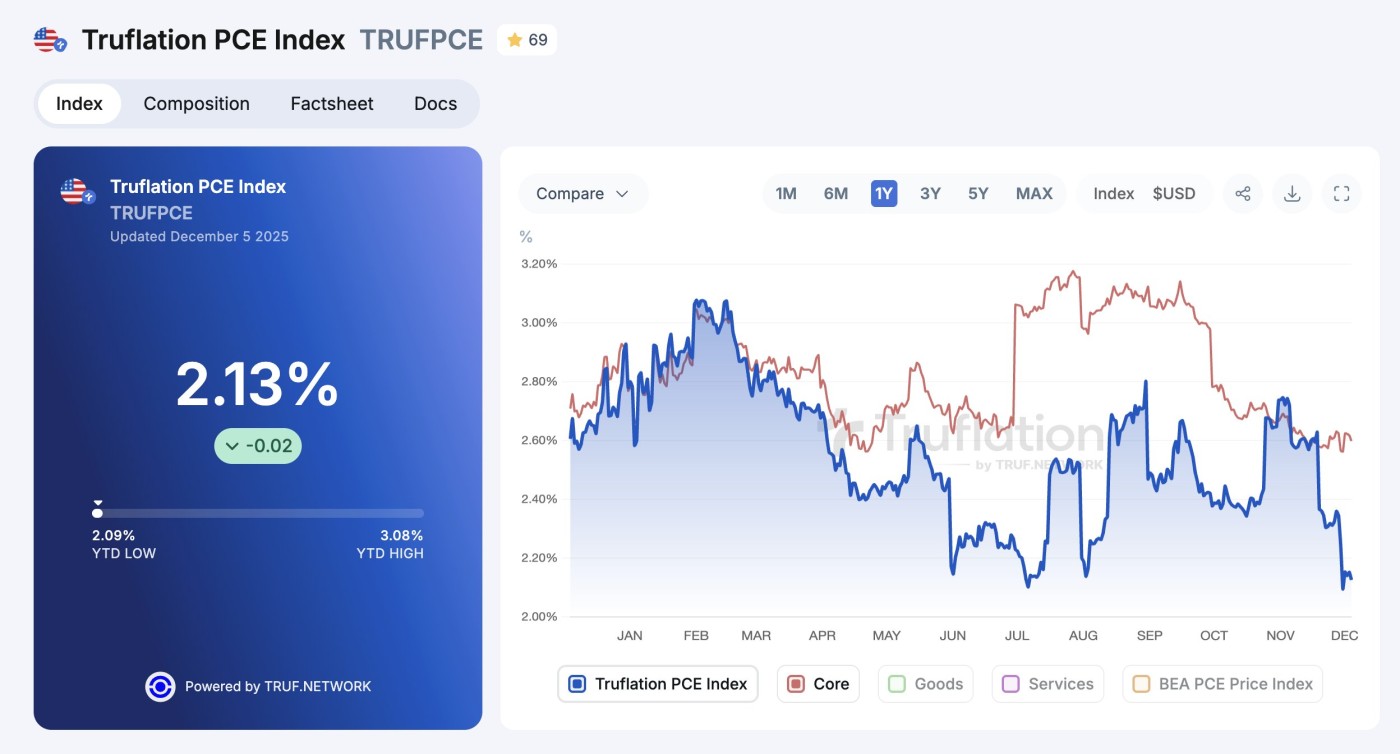

Truflation PCE: 2.13%

Truflation Core PCE: 2.6%

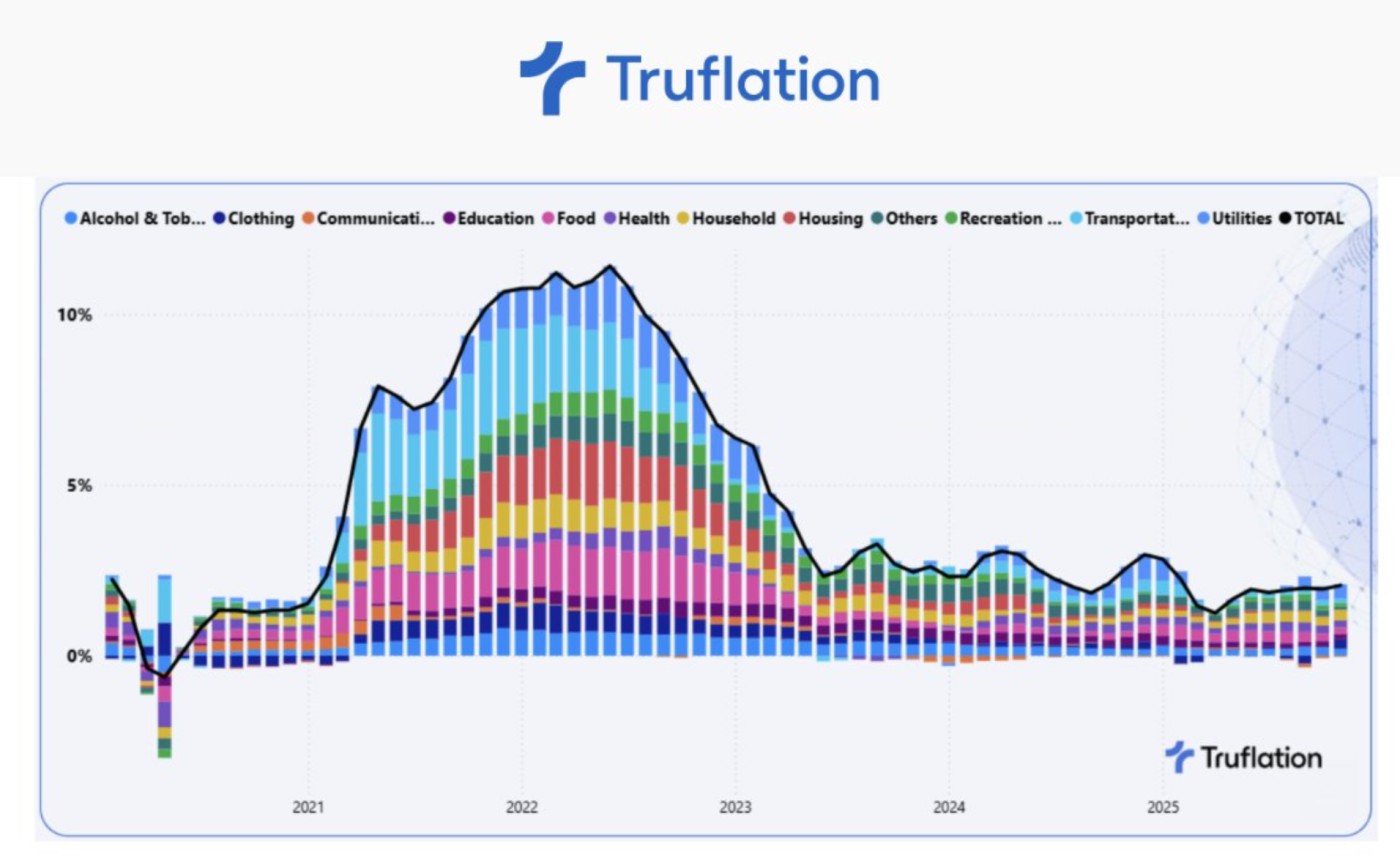

The latest data show a cooling trend towards the low end signalling tame prices that pave a smooth runway for growth with core holding steady:

Truflation PCE: 2.33%

Truflation Core PCE: 2.6%

Truflation gets their PCE index by taking millions of price data and assigning them to BEA's categories and subcategories and their BEA's weighting to make their index directly comparable but using more current and real prices from real purchases, as opposed to surveyed prices. It leads BLS CPI by ~45 days; historically correlates 0.97-0.99 with official data.

Truflation US Inflation Index:

Meanwhile, Truflation US Inflation Index (composed with more than 30 data partners which are grouped in 12 household expenditure categories) shows inflation is **stable, contained, and off the peak**, a backdrop that keeps the door open for growth without the shadow of runaway prices. With today's CPI report, the graph below will show 2.36%.

The long term Truflation US Inflation Index emphasizes how inflation this year remains benign, especially given today's CPI numbers. When the graph below is updated, it will low a lower bar:

FAQs

Q: Do you think the upcoming bank of japan interest rate decision will have an impact on US markets?

A: A Japanese rate hike could cause markets to fall, primarily through potential unwinding of the yen carry trade and shifts in Japanese capital flows. Markets are pricing in about 90% odds for a rate hike when the Bank of Japan meets on Dec 19. Past BOJ hikes triggered volatility: the 2024 increase caused a Nikkei plunge and S&P 500 drop of 6% in days, with tech stocks hit hardest amid forced deleveraging.

Q: Please cover trade management on the GLXY trade.

A: GLXY Galaxy Digital correlates well with the price of bitcoin since much of Galaxy’s revenue comes from trading, OTC block deals, lending, asset management products, and banking services that see volumes and fees surge when bitcoin is in a bull phase and contract when BTC is weak. It also holds a large proprietary BTC position (over 17,000 BTC as of mid‑2025). Since bitcoin looks weak and could head lower in part due to the MSCI decision on January 15 as to whether MSTR will stay in the index or not, GLXY is likely to also head lower. On the other hand, global liquidity is reaccelerating so could counter the selling due to the upcoming MSCI decision. Sidebar: If MSTR is forced to exit the index, JPMorgan and others estimate forced passive outflows from MSTR could run from roughly $2.8 to 8.8 billion if MSCI proceeds and other index providers follow, which is material selling pressure on a key leveraged BTC proxy.