Over in Europe, the European Central Bank decided to leave interest rates unchanged and announced that it expects to lower its monthly asset purchases to EUR 30 billion from EUR 60 billion in January. That pace of purchases is expected to continue until at least the end of September 2018.

So The Great Unwind which began in the spring of this year will accelerate and begs the question how stock and bond markets will react. Will it be the straw that finally crashes the camel? ETF TLT which tracks the price of the US treasury 20+ year bond index has been trending lower since September. And that's after weakly trending higher in wide bands all year. In fact, TLT is back under its 200dma and at the same price it was in January. Perhaps this is the beginning of a more pronounced downtrend in the price of long bonds?

With centrals banks aware of such a possibility, The Great Unwind may turn into the Endlessly Infinite Unwind. Just as the market has baby-stepped higher, we would most likely see central banks slow their unwinding process should the stock market start into a major correction as we saw in the early years of QE such as in 2010 and 2011. The US Fed was quick to launch QE 2 then QE 3 as well as Operation Twist to counter falling markets. Certainly, they don’t want to undo the artificially created bubble QE has created in the US stock market since 2009. But of course, bubbles are bubbles because they do eventually burst. When global debt has become this massive, there has never been a soft landing.

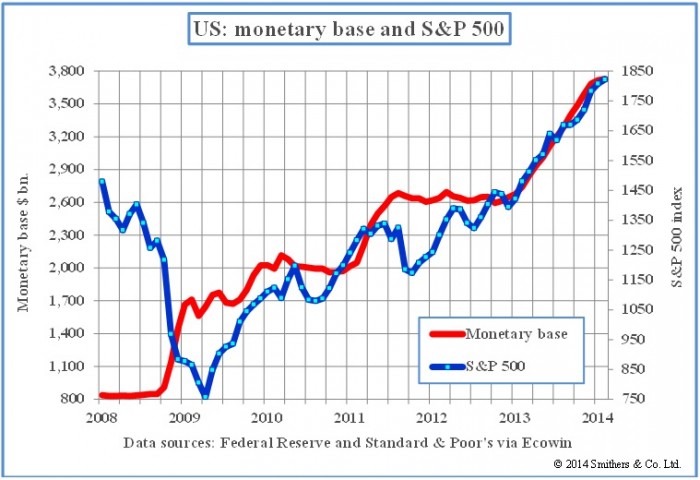

The chart below shows the high correlation between the S&P 500 and monetary base, both which were pushed higher by QE. When central banks unwind their balance sheets, their respective monetary bases will shrink. Should central banks unwind too quickly, the S&P 500 will most likely follow any downtrend in the US monetary base. Thus, the monetary base may end up decreases at an ever-slowing pace, thus the implication of the Endlessly Infinite Unwind.

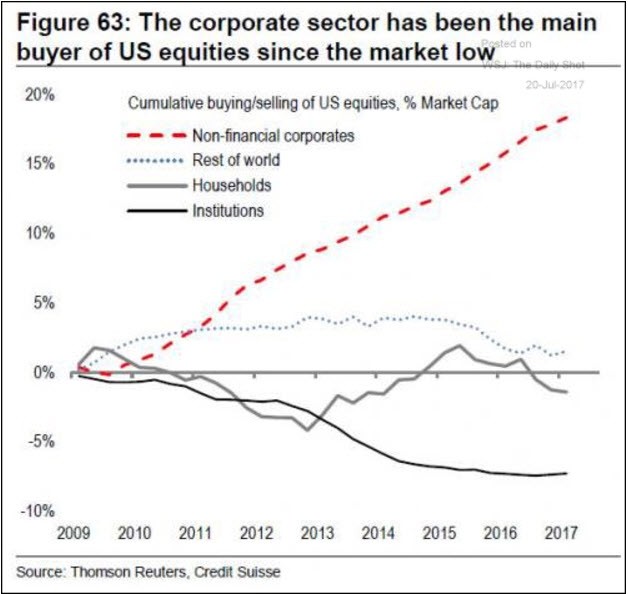

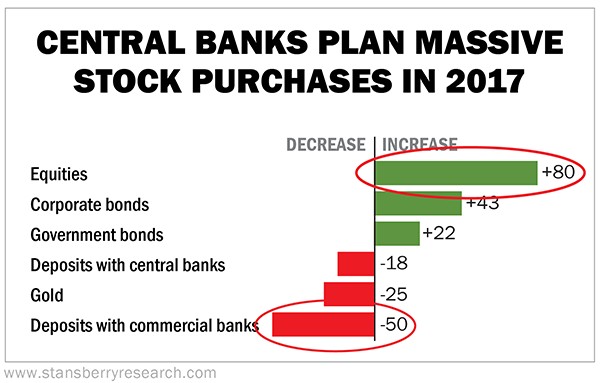

Meanwhile, corporations and central banks have been the main buyers of US equities since the market low as shown in the two charts below:

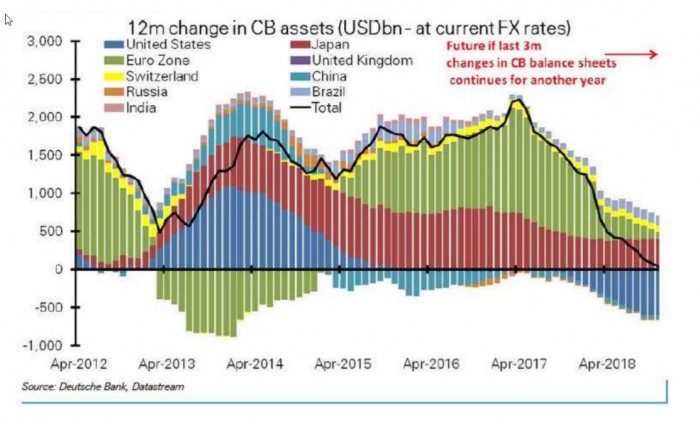

Now what happens as the QE unwinding process steepens thus pushing the monetary base lower? Notice in the figure below how QE-flow peaked in the spring of this year with the European Central Bank, Bank of Japan, and Bank of England continued to print at record levels while the US Federal Reserve continued to taper. Balance sheet reduction will accelerate when the ECB reduces its levels of QE to $30 billion/mo down from $60 billion/mo starting in January 2018. Perhaps that will be the final blow?

Of course, central banks will not continue to reduce QE at this pace should stock markets start to crack as they presented with 20% corrections in 2010 and 2011 which spurred on renewed measures of QE. Singularly, Fed Chair Yellen as well as other major central banks have left open the possibility of lowering interest rates once again, and even going negative (!) should the global economy falter in the face of The Great Unwind. But that in and of itself could spur a crash of some magnitude as markets know central banks have little to no fuel in their respective tanks as interest rates remain at or near historically low levels. Such actions could destroy any remaining faith markets have in the Federal Reserve.