by

Dr. Chris Kacher

We hear Trump crowing about his economic accomplishments while he has been in office, so I thought I'd go through the actual record of Trump's impact on the economy.

First, the positive:

- 1) The 327,000 new manufacturing jobs over the last year represent the best 12-month stretch in 23 years.

- 2) The GDP rate (4.2%) is higher than the Unemployment Rate (3.9 %) for the first time in 12 years, since 1Q 2006.

- 3) Small-business optimism is near the highest level in 35 years. Small businesses felt Obama was not small-business friendly.

- 4) There has been a revitalization of business spending due to Trump's tax cuts from 35% to 21%. By contrast, such spending was poor during the last 2 years of Obama's administration.

The positives above are certainly of note and begs the question whether such is too little too late given the onerous levels of debt, or whether Trump's tax cuts and deregulatory policies will help the U.S. maintain a strong economy. So while global central banks continue to print money near record levels driving up debt and making fiat that much more fragile, the bull market in the U.S. may continue for another year or two or longer.

And now the negative:

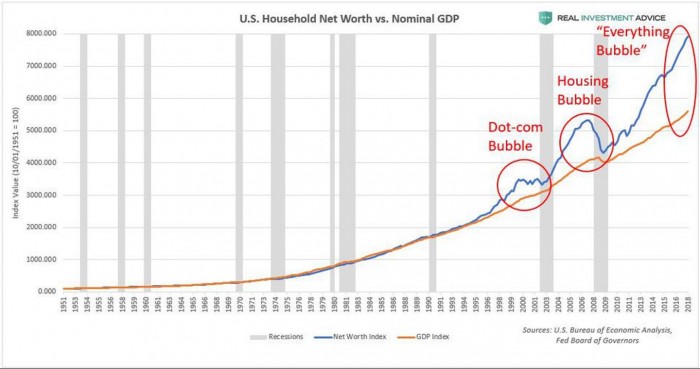

- The ballooning federal deficit under Trump's tax cuts and trade policies pushes it up above $1 trillion a year. His policies are not helping to reduce the debt bubble. The question remains when this and other bubbles start to blow apart. Here's one bubble: Since 1951, the distance between US household net worth vs. US GDP currently stands at record levels. Household net worth far exceeds GDP at present. It far exceeded GDP at the peak of two prior bubbles, namely the housing bubble which led to the 2008 financial collapse and the dot-com bubble which led to a 78% drop in the NASDAQ Composite.

Another way to look at is by plotting U.S. household wealth as a percentage of GDP. Since 1951, household wealth has averaged 379% of the GDP, while the Dot-com bubble peaked at 429%, the housing bubble peaked at 473%, and the current bubble stands at a record 505% of GDP.

The underlying drivers of the current bubble is the U.S. Federal Reserve-driven bubbles in stocks, bonds, and housing prices, thus some have called the current bubble the 'everything' bubble. Back in 2008 during the housing crash and Great Recession, the Fed was so desperate to create an economic recovery and bull market that it decided to do so via the brute force of monetary policy. It cut interest rates to record low levels by pumping trillions of dollars worth of liquidity into the financial system which is known as QE. The S&P 500 consequently soared by over 300%.

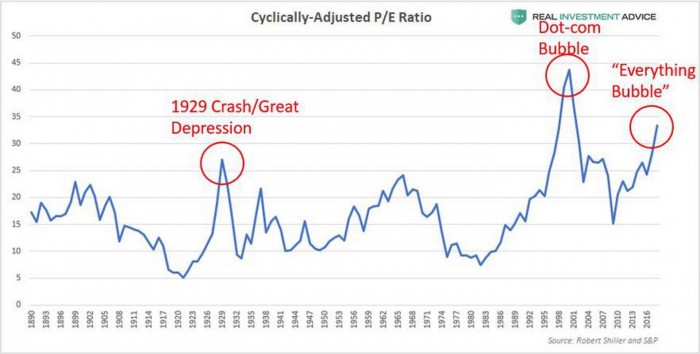

Here's another bubble: After nearly a decade of QE, the U.S. stock market is as overpriced relative to its fundamentals as it was at major historic peaks such as in 1929 and during the dot-com bubble. According to the CAPE ratio which is the cyclically adjusted PE ratio, the U.S. Stock market is more overvalued than it was in 1929 though still remains below the spike it achieved during the dot-com bubble.

The current U.S. household wealth bubble will end the way that the last several asset and wealth bubbles did. The Fed ended loose monetary conditions that caused the bubble in the first place. The higher the Fed hikes rates, the closer we get to the end of the road. Ray Dalio who founded Bridgewater Associates, the world's largest hedge fund, recently said the rate hikes are now hurting asset prices. When bonds break, bonds could take stocks with it much as happened when subprime mortgage bonds broke leading to the financial collapse of 2008. Adding fuel to the fire is the quantitative tightening policy which shrinks the balance sheet by $40 billion a month.

- A second negative for Trump is the continuation of higher interest rates which could impact housing, automotive, and business investments. On the other hand, the E.U., the U.K., and other parts of the world are all struggling economically. This may prevent the US Federal Reserve from hiking rates as many times as they wish. Fed officials remain committed to a gradual hike in rates but are concerned that the global economy is slowing. Germany who leads the E.U. economically reported the worst growth in nearly 6 years at a recessionary -0.2%, adding to worries over global growth. As mentioned in the weekend's Focus List report, the Bank of England may have to increase its QE program at some point as a necessary trump card the U.K. must play due to the E.U.'s attempts to prevent Brexit. Given the weakness in the E.U. as noted by Germany's latest GDP figure among others, the ECB may also have to postpone its planned reduction in QE.

Here is what hasn't changed:

1) The uptrend in GDP growth continues to move higher from Obama to Trump.

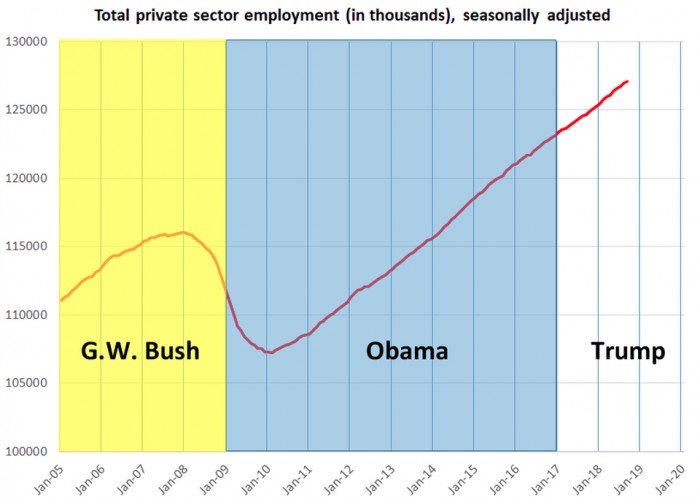

2) Total private sector employment continues to move higher from Obama to Trump in a steady linear uptrend suggesting things have remained at the same pace whether the country was being led by Obama or Trump:

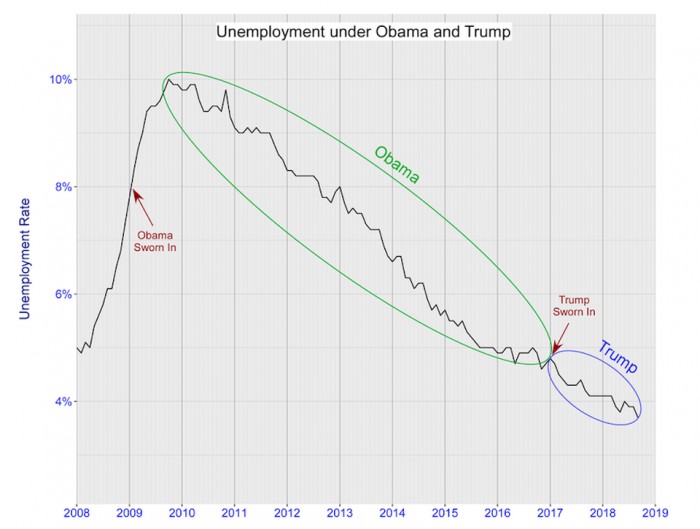

3) The downtrend in unemployment continues to move lower from Obama to Trump in also a fairly steady linear downtrend:

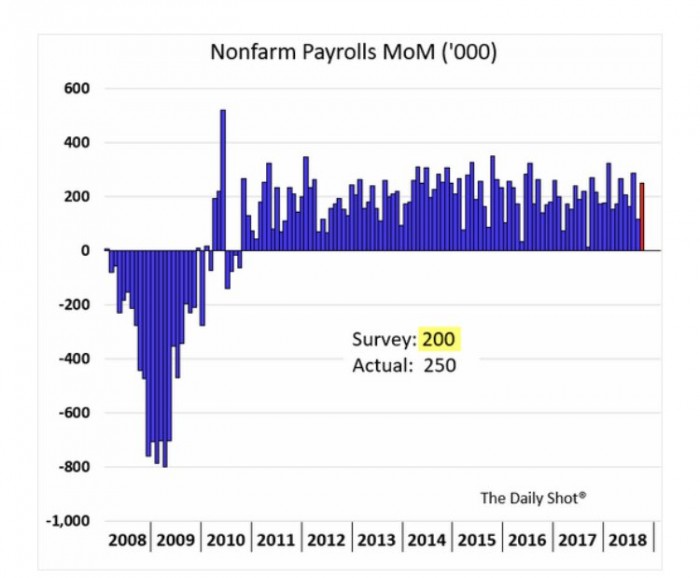

4) Nonfarm payrolls remain equivalent from Obama to Trump:

So Trump is being misleading when he suggests he is responsible for any of these four metrics. Nevertheless, we will have to see if U.S. GDP can continue at its current pace with Trump's tax cuts and deregulatory policies in place. The ECB's plans to roll QE back further may have to be postponed, but even if it is reduced according to schedule, QE will still be a formidable force even at reduced levels. Such may continue to push the U.S. market higher, albeit in choppier fashion, though with further rate hikes, the current correction may become more serious with rising bond yields sucking money from the stock market. That said, despite the elevated levels of volatility due to the QE vs GDP vs rate hike tug-o-war, this ageing bull may yet have another year or two left in its lifespan.