by

Dr. Chris Kacher

In a speech on Wednesday, Powell said interest rates were "just below" the neutral level at which they neither stimulate nor hinder economic growth. This was in stark contrast to when just 2 months ago, he said rates were probably "a long way" from the neutral point. Further, the Fed meeting minutes showed the central bank is expecting to hike interest rates in December but emphasized the importance of incoming data for upcoming decisions, making future moves less predictable. This suggests fewer interest rate hikes in 2019. While a fourth rate hike for 2018 is expected in December, the market is now only anticipating 1 rate hike for 2019, down from 3.

The Fed has always been able to reduce rates during recessions to spur the economy. Without sufficiently high interest rate levels, it would lack the 'fuel' to do so. Since interest rates are still below historical norms, the interest rate fuel in its tank is still subpar, thus the Fed would like to continue to hike rates while GDP remains strong. Nevertheless, it seems Powell believes the economy could encounter some slowing or rather that he does not want to slow the robust levels of GDP, thus feels more dovish in terms of slowing the pace of rate hikes.

That said, onerous levels of debt and low interest rates still prevail. The question is whether the U.S. can keep growing in light of what is discussed below. Despite Trump's tax and deregulatory policies, it begs the question whether capital will eventually flow into hard assets such as gold and real estate should bubbles burst, the US stock market crater, and the US dollar devalue.

Ray Dalio who runs the world's largest hedge fund thinks this will happen, and feels stocks boosted by lower interest rates and QE have largely run their course. He says the world by and large is leveraged long, explaining that low interest rates have fueled stock buybacks and M&A, boosting stock prices, which also were pushed higher from Trump's tax reductions.

Dalio's new book “Principles for Navigating Big Debt Crises,” compares the current era of investing to that of the 1930s when the U.S. was also in the late stages of a business cycle with populist politics and huge levels of debt, though today's debt stands at even greater levels than in the 1930s. Interest rates in many first world economies remain near record lows as central banks have already purchased trillions of dollars worth of assets. But total debt in the U.S. is still far lower than it was during World War II. The US then grew its way out of its massive debt after the war.

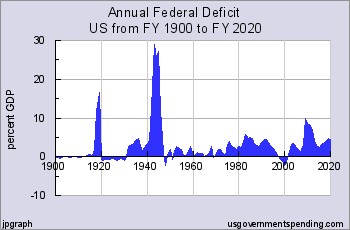

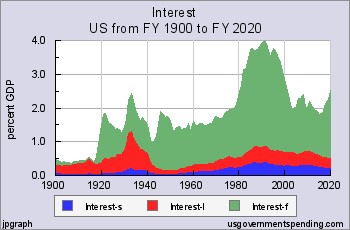

At present, debt interest as a % of GDP is still contained (well under the 12% red flag level) and the total annual deficit is still well below what it was in WW II:

Despite this, Jim Rogers, Ed Seykota, and Alan Greenspan all agree more or less with Dalio's views. Dalio described America’s worst nightmare of the dollar losing its place as the world’s reserve currency. His concern is that swelling U.S. budget deficits will eventually be problematic for big buyers overseas such as China. Dalio said, “You easily could have a 30 percent depreciation in the dollar within the next 2 years” as the Fed has little choice but to monetize the national debt. “The role of the U.S. dollar will diminish, and the returns on U.S. dollar-denominated debt will suffer. Then I think you will see the emergence of other currencies.”

Ray Dalio compares 1929-1937 period vs 2008-2018:

· In both cases, the financial crisis caused interest rates to go to zero, forcing central banks to print money to buy financial assets. The resulting asset market rallies drastically increased wealth disparity between rich and poor. [My comment: The reaction by politicians triggered rate hikes, plus the wealth disparity is not an issue because a rising tide lifts all boats, thus people across the board are better off. Technology has made a massive impact over the last 50 years and continues to accelerate in terms of quality of life in the U.S. and now more globally.]

· Political polarization between left and right occurred globally, and populist/progressive movements popped up everywhere. In the 1930s, populism led to nationalist dictatorships in Italy, Spain and Germany. [My comment: Populism by itself is not the issue but the leftist, progressive thinking which sounds great in theory but often leads to socialism, fascism, and a lower tide for all.]

· Japan was the China of the 1930s, a rising global economic power. The global response were trade restrictions and eventually an oil embargo. [My comment: Trump is a businessman so does not want to create waves that cause a steep drop in the stock market. Of course, this situation remains in flux.]

· In 1937, the Fed began tightening monetary policy – U.S. unemployment jumped 19 percent and manufacturing fell by 37 percent from peak. The Dow Jones Industrial Average cratered -50.2% per cent. [My comment: The situation today is different from 1937. 1937 did not have strong pro-business policies in place as we have today. Instead, we had a socialist government in place (New Deal, etc) which hamstrung many businesses.]

The US devalued the dollar by 41% in 1934 in the throes of the Great Depression. But today's situation is not the same. While Trump’s policies have greatly helped, they have also increased the deficit to more than $1 trillion this year but a material part of this is Obamacare which has yet to be repealed. That said, are the existing bubbles broad enough to affect the stock market should any or all of these bubbles blow apart? It is claimed the current U.S. household wealth bubble will end the way the last several asset and wealth bubbles did- by The Fed ending loose monetary conditions that caused the bubble in the first place. But this is wrong. Utopian affirmative action with ninja type loans and the equivalent where most anyone would qualify for a home loan created a monstrous real estate bubble which blew apart in 2008. There is arguably no such bubble today, though there are many smaller bubbles, some which I will discuss in a future report, but none sufficiently endemic to cause a replay of 2008.

Nevertheless, the perception is that the higher the Fed hikes rates, the closer we get to the end of the road. Dalio recently said the rate hikes are now hurting asset prices. Adding fuel to the fire is the quantitative tightening policy which shrinks the balance sheet by $40 billion a month. But the question remains how fast GDP can continue to grow to offset rising rates. If GDP can continue to grow, then this ageing bull market will head higher once again, especially given the still near-record levels of global QE still in place as global economies remain weak thus have no choice but to continue to print. And futures are up around 2% at the time of this writing as Trump and China reached common ground.