by Dr. Chris Kacher

QE Broken Record

Some investors are tired of hearing about quantitative easing and its numerous affects on the markets. Nevertheless, part of investing is staying in step with changing markets as the only constant when it comes to trading is to be ready for change when it happens. Thus black box trading strategies are a myth since markets are ever-changing.

Birth of the Pocket Pivot and Buyable Gap Up

For example, starting in 2004, base breakouts no longer were nearly as profitable as they had once been in the 1980s and 1990s. Markets had changed in a substantive manner. This spurred my research to find patterns that pre-empted base breakouts. I called these Pocket Pivots. In conjunction with this, I also found that certain stocks that gap higher also can be quite profitable. I called these Buyable Gap Ups.

Furthermore, fundamental strength in a stock relative to where it was trading was also a key factor. Thus the technofundamental approach I used to buy base breakouts with success in the 1990s could be used with success in the era of quantitative easing.

By staying aware of changing markets, prior to QE, pocket pivots could be bought on strength with success, even with a 4-6% stop loss which was typical of the higher octane, more volatile stocks often with relative strengths above 95, as the risk/reward was sufficiently favorable. But after QE, markets changed such that buying on constructive weakness after a pocket pivot was the better approach. This kept risk/reward in check as it allowed for maximum losses typically within 3% from the buy point.

And in this QE environment, upside was more limited with stocks often trading in wider bands, thus taking profits when you have them in context with a stock’s chart became a more profitable strategy. One in the hand vs. two in the bush was never more true.

QE and The Fed

QE has pushed many countries into onerous levels of debt. Countries with negative interest rate policies continue to falter. For example, by the time the Bank of Japan announced its plan to push rates into negative territory, its debt-to-GDP was already above 200%. Japan currently holds the record at a whopping 237%. Conditions have deteriorated to the point where Japan’s largest private bank, the Bank of Tokyo-Mitsubishi, announced it wanted to leave the Japanese bond markets because BOJ QE interventions made them unstable.

Indeed, gone are the heady days of the Nikkei achieving new high after new high as it did in the 1980s. In fact, the Nikkei is still way off its peak achieved in 1990 of nearly 40,000, as it trades currently just above 20,000. That said, it has managed to go from around 8300 in late 2012 to where it stands today due to the effects of QE which has helped some businesses. But at what price?

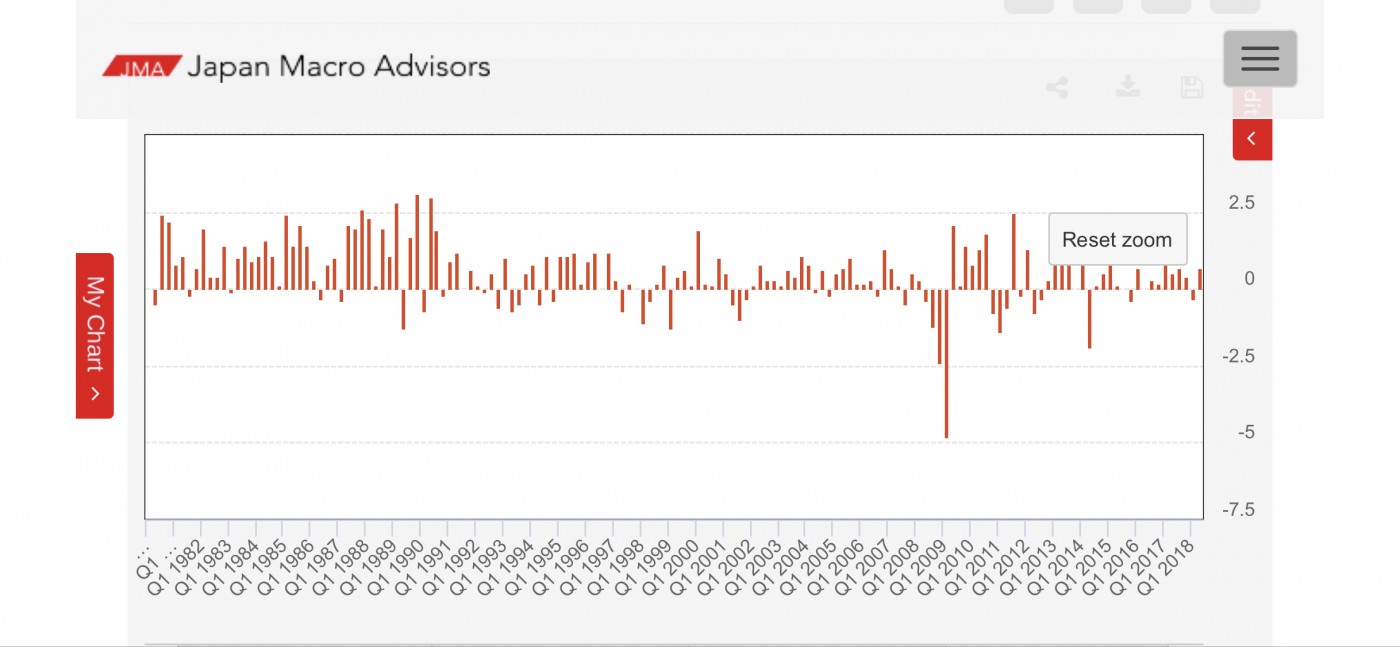

Here is a chart of Japanese GDP since 1980. As one will see, the heady days of big growth ended in 1991, which kicked off QE by the Japanese government in all its forms in addition to legislation which hamstrung many Japanese businesses such as making it far more difficult to fire an employee. Growth has been anemic since then. In recent years, even with QE and negative interest rates, GDP was 0.4% in 2014, 1.4% in 2015, 1.0% in 2016, and 1.7% in 2017.

That said, to play devil’s advocate, I have mentioned that debt levels in the U.S. were at higher levels in the 1940s due to World War II, but the U.S. was able to grow out of that situation. Keep in mind, however, that Interest rates were also at higher levels than they are today. So while it could be argued that low interest rates have been and are the “new norm”, it is instructive to know why. And QE is the culprit.

In today’s climate, I have mentioned Trump’s pro-business policies together with exponential growth technologies could possibly help the U.S. continue its economic lead. But the rest of the world is struggling. For example, the Bank of England reported on Thursday that its growth is at its weakest since 2009. So will the U.S. still be able to sidestep pronounced levels of weakness across the globe? Some say yes as the U.S. has become increasingly insular and protectionist. But if the U.S. has to lower rates again to help spur its economy, the amount of fuel in its interest rate gas tank is historically at low range. This could cause a big problem in terms of jump starting the economy as negative rates have not worked in Japan nor in Germany.

It’s no surprise the Fed has made some critical mistakes in the past. And I’m not targeting any particular Fed Chair, but the concept as a whole is damaged. A small group of people who try to control a dynamic market will always fail, no matter how smart they are. That said, they are often under political pressure which further can color the situation. One could also argue that those from Ivory Tower academic environments are less suited to such positions since reality often wins over theory. This is why legendary investors such as Peter Lynch used to say he would never hire those with MBAs or business degrees, but preferred those untainted by academics.

Nevertheless, it is more important to always keep a close eye on price/volume action in stocks and major averages as these metrics will keep one on the right side of the market so one can portfolio position accordingly. The increasing number of stocks on which we have issued reports is a potentially positive sign of an uptrend which may be more than just a dead cat bounce, especially given the current stance of global central banks wrt QE. Knowing that past, present, and future have been, are, and always will be riddled with change helps to keep things in perspective, rather than trying to ever wish things were as they were or will be a certain way in the future, which is a waste of energy.