Goldman Sachs and Bridgewater's Ray Dalio Both Bearish

Both Goldman Sachs and Ray Dalio, the founder of the world's largest hedge fund, have been saying the stock market is likely to encounter low returns at best in the years ahead due to quantitative easing and ultra-low rates which has put the world into record levels of debt, even beyond that of the 1930s. Goldman's gauge of bullish and bearish momentum in the US stock market, what they refer to as the bull-bear indicator, suggests the likelihood of a bear market occurring is at its highest point since the 1970s. But Goldman emphasizes that they are not suggesting a crash but rather a period of lower returns. CME FedFutures puts the odds of a rate hike at near certainty when the Fed meets later this month, and a 58% chance of a hike when they meet in December. Since inflation remains relatively tame, the Fed will likely err on the side of caution to avoid derailing the fragile global economic recovery, thus the rate hike later this month may very well be this year's last.

That said, part of the challenge in making such predictions is the highly unusual nature of this QE-driven bull market, such that Goldman suggests making historical comparisons is difficult at best.

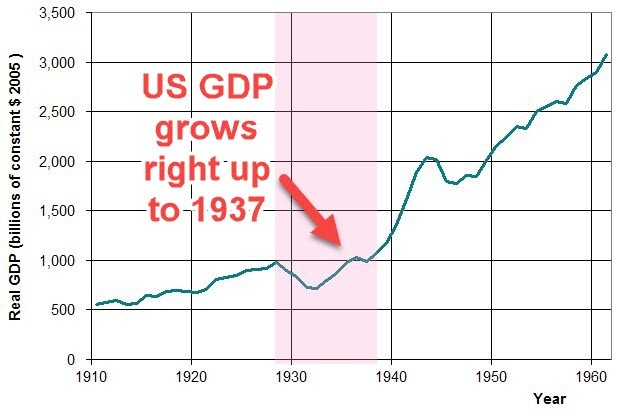

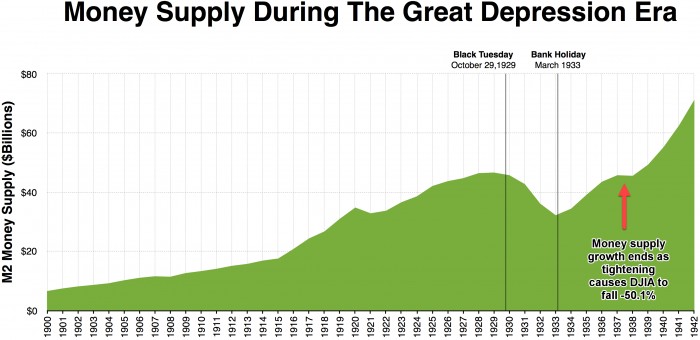

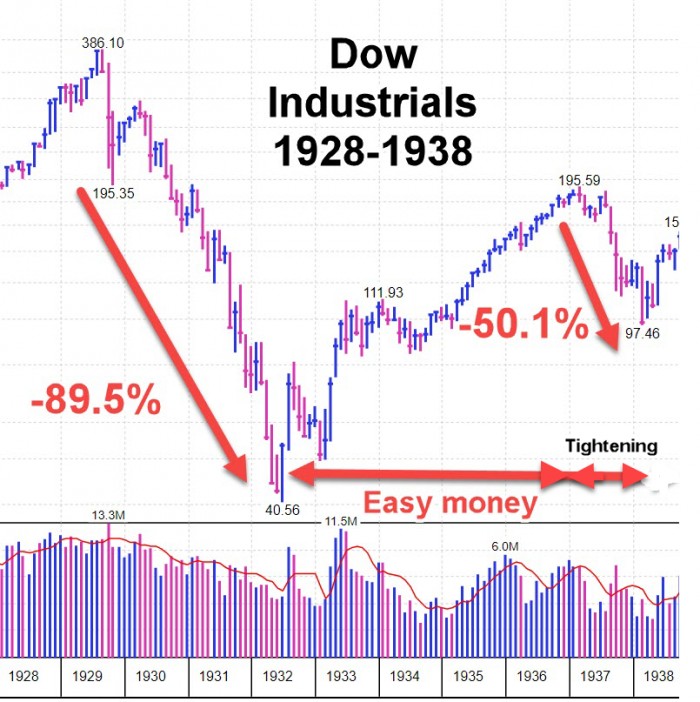

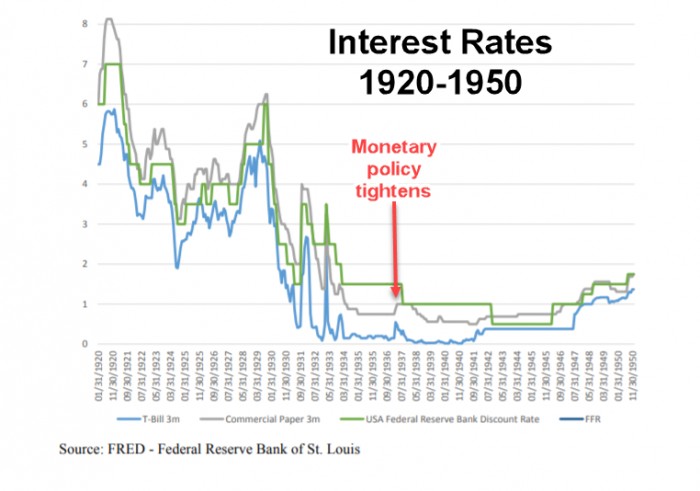

Nevertheless, Dalio suggests being more defensive than aggressive as he thinks the benefits of President Donald Trump's corporate tax cuts signed into law late last year have already been factored in. But maybe Mr. Dalio should consider the deep impact former President Ronald Reagan's pro-business policies had on markets for a number of years as reflected by the prolonged bullish reactions across various markets. Dalio goes on to say, “The ability to ease monetary policy by lowering interest rates is limited in the United States and nonexistent in Europe and Japan, and quantitative easing will be a lot less effective in the future than it was in the past.” This is indeed a concern given the record levels of debt. Dalio also adds that the current economic cycle mirrors 1937 as back in the 1930s, years of money printing and low interest rates along with low unemployment and rising GDP led to the Fed tightening rates, though the discount rate continued to fall starting in 1933. Notice in the figure below how US GDP grows up to 1937 due to easy money policies which resulted in low interest rates and low unemployment.  The figure below shows how money supply growth ends in 1937 due to monetary tightening causing the DJIA to fall -50.1%: The figure below shows how money supply growth ends in 1937 due to monetary tightening causing the DJIA to fall -50.1%: After the October 1929 stock-market crash, the Fed slashed interest rates and began printing money, engineering what Dalio calls a “beautiful deleveraging” — the perfect balance of inflationary and deflationary forces that reins in a big debt crisis. The same happened in the U.S. after 2008. The mid-1930s then saw the Fed-built recovery ignite a rally in stocks, just as the Fed’s moves after 2008 have made today’s stock investors a lot wealthier. Back then, like today, a wealth gap erupted to where the top one-10th of 1% of the population was worth as much as the bottom 90% combined. Dalio says about the same level of income inequality exists in the U.S. currently. Such extremes where the middle class has eroded is an unsustainable socioeconomic disparity. And back in 1937, this tipping point to the debt cycle led to a -50% drop in the Dow Industrials. |

The Federal Reserve has tightened a number of times without pricking the QE debt bubble because global QE remains substantial, thus it can be argued the bull market may continue for longer yet, which will give Trump's policies more time to further prolong this ageing bull market even as global QE slowly winds down.

Inept Japanese governmental policies as well as Brexit over in the UK keep both central banks hamstrung thus near record levels of QE continue to flow from both countries. But over in the EU, beginning in October, the ECB will once again reduce the monthly buying of bonds from €30 to €15 billion. The reduced pace is set to run until the end of the year and starting in 2019, the ECB will not buy any more bonds. The Quantitative Easing program that started in 2015 is reaching its end. Stronger GDP numbers with subdued inflation is giving the ECB more room to slow QE but the ECB has said they will not look to raise rates until the end of summer 2019 as things are still fragile.

So despite current debt levels brought from a massive QE flow, if a soft landing can be achieved via Trump's pro-growth policies as well as with the help of numerous cutting edge technologies that are growing exponentially, the historical significance will not go unnoticed. But keep in mind that monetary policy has often erred at critical junctures thus has at times caused great upset to the economy and to markets. Perhaps at best, a slowing economy over the next few years could be the best possible scenario, if not something more serious of the black swan variety.

Actionable Stocks

The mushy market remains thematic though there have been a few names on which we have reported that can be monitored for potential entry points in addition to reports sent on stocks already trading in low risk zones.