by Dr. Chris Kacher

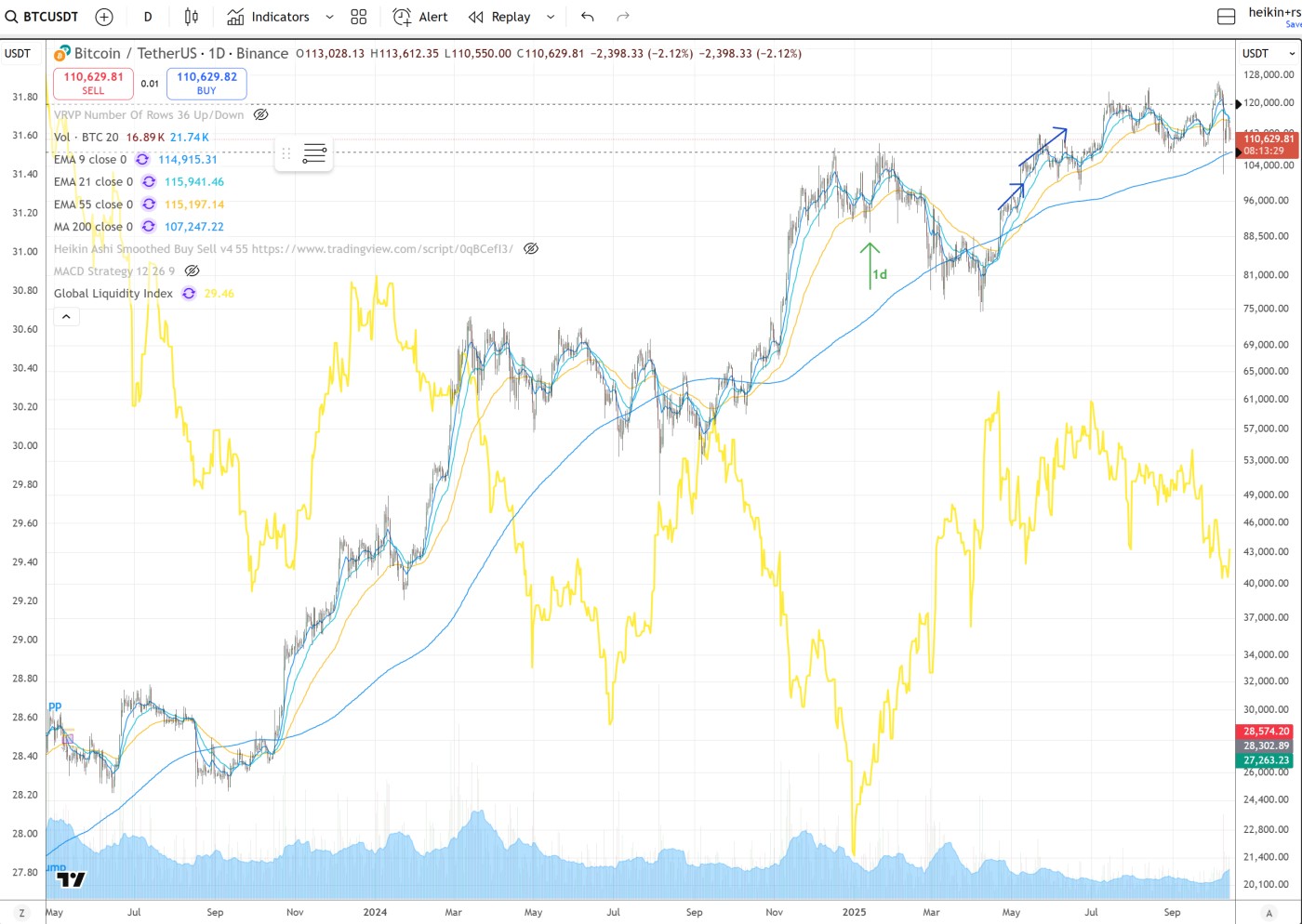

Gold, Bitcoin, and stocks all outperforming

We mentioned in a prior report on how the administration is shifting QE to Main Street from Wall Street by expanding ‘Treasury QE’ (i.e. heavy Treasury bill issuance) and reducing Fed QE (i.e. banks’ reserves and money market liquidity). This bodes well for hard assets, stocks, precious metals, and bitcoin.

Historically, when gold outperforms stocks, it has only happened during moments of stress such as the 2008 great financial collapse, the 2011 euro-zone debt panic, and the 2020 pandemic.

But right now both are outperforming. Gold is surging while the S&P 500 enters its third year of a bull run. With risk-assets booming and Big Tech ruling the market, gold and stocks are making record highs simultaneously.

There are a few reasons for this.

For gold, global central banks have ramped up gold purchases, retail investors are piling into gold, and demand for gold ETFs is booming.

For stocks, AI is materially lopsiding the market with Big Tech and related AI names outperforming.

So both leading stocks and gold can outperform which is a historical anomaly.

Bitcoin is the only denominator that exposes the post-2020 economy as a slow-motion Zimbabwe. Gold is the state's ancestral memory for multiple millennia of default insurance. Bitcoin is the emerging consciousness, holistic with the ability to step outside the denominator entirely. Gold remembers value; Bitcoin redefines it.

As bitcoin and gold reach new highs, fiat is entropy trending toward zero. But across the whole financial spectrum, entropy always increases. Gold and bitcoin rising together is the world beginning to price truth again.While the shorter term perspective shows bitcoin will underperform at times and can even be shorted, the overall correlation on a quarterly to annual basis shows bitcoin continues to outperform most markets. Remember, the mainstream press has announced the death of bitcoin almost 500 times.

Global liquidity fuels bitcoin/crypto. When the Fed and/or other major central banks slow QE, bitcoin has deep corrections of as much as 94% prior to 2013 but since then, 75-85% is more typical from peak-to-trough during tightening phases.

The simultaneous rise of gold, leading stocks (especially AI tech), and bitcoin suggests a unique market state where traditional safe havens and disruptive digital assets all exist in strength. Markets are increasingly pricing in a new reality where value is simultaneously “remembered” (gold) and “redefined” (Bitcoin), while AI-driven growth propels equities forward. This multifaceted environment departs from historical norms and signals transformative shifts in global finance.

Covid crash: $1.2B in liquidationsFTX crash: $1.6B in liquidations

Friday 10/11/25: $19.14B in liquidations

The crashes from the first two were literally the best days of the last decade to buy. Binance BNB just hit new highs after its massive correction.

Boosting the bounce, late on Sunday afternoon, Donald Trump seemed to backtrack on his threat to impose a further 100% tariff rate on China when he posted on his Truth Social account, saying ‘Don’t worry about China, it will all be fine!’ He said that President Xi ‘had a bad moment’ and that the US wants to ‘help China, not hurt it !!!’

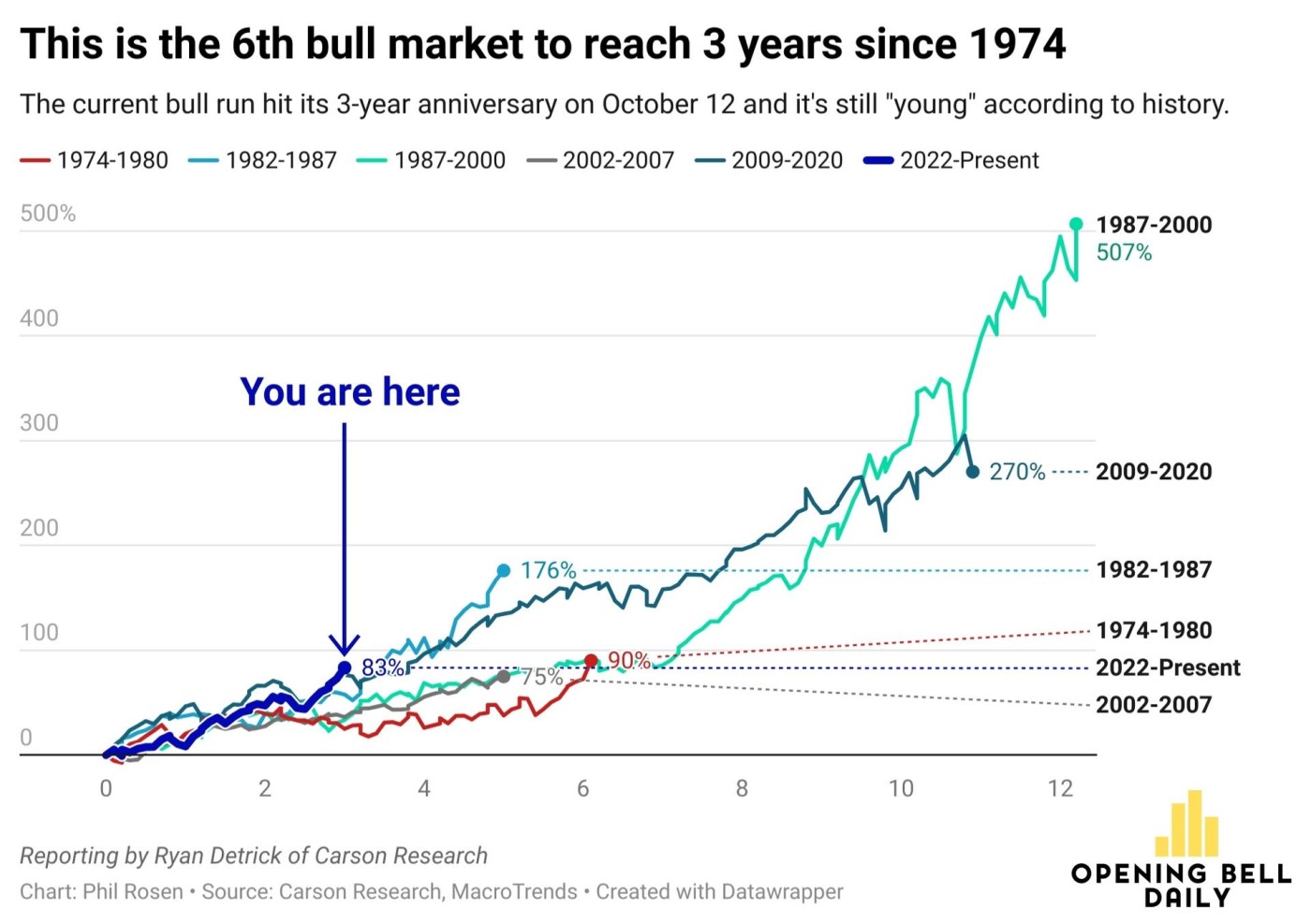

Further, from a historical perspective, since 1974, this is the sixth bull market to reach 3 years. History suggests three years is still “young” compared to the other bull runs given that there have been 11 other bull markets since World War II, and all reached their fourth anniversary except for one.S&P 500 is up 83% this bull market, far less than the average 191% of the last 11 bull markets. Most bull markets go longer than three years with an average of 5 years, but the 2009 bull lasted twice that long due to various forms of quantitative easing. With QE alive and well across major central banks, expect this bull to run.

AI boosting GDP but with caveats

Also helping markets, a large portion of real GDP growth came from investments tied to data centers and information-processing tech. In the first half of 2025, AI-driven “information processing equipment” totaled about 1.11 percentage points to real GDP growth, while “software” added about 0.99 points. Together they explain a large share of the 3.8 percent annualized growth print, even as other components were mixed.

Recent deals between tech giants like xAI, NVIDIA (NVDA), AMD, and OpenAI show that building massive AI computing power isn't just about buying hardware. It's become a big part of how companies handle their money and investments. Instead of just spending cash outright (“capital expenditure” or capex), these companies use clever financial setups, like letting partners own part of their company, using special financing vehicles (called SPVs), and even leasing chips as if they're assets. Massive capex in data centers and AI infrastructure appears to be genuinely stimulating the real economy, not just market values, but construction, hardware, energy, and supply chains as well.

Studies indicate that AI investments drive potent productivity gains, sales growth, market valuations, and innovation, providing long-term tangible economic benefits. The McKinsey Global Institute and others estimate trillions in new economic value will emerge from this capex wave, and these effects may not be fully captured in traditional economic statistics.

This helps AI labs expand quickly by giving them access to the latest chips before paying full price, while the chip vendors (like AMD and NVIDIA) lock in guaranteed big orders that help plan their business over several years. Because these deals set specific milestones for delivering chips, the entire schedule of building new AI capacity links tightly to the chip makers’ supply timelines. Since both sides are betting enormous amounts of money and shares, these arrangements now play a major role in U.S. economic growth.

In essence, Big Tech and AI companies aren’t just buying computer chips anymore. They’re teaming up with chip companies, trading shares, and creating new financial plans that help them grow fast while making sure everyone stays on track with technology goals. These “financialized” deals not only build more AI labs but also drive much of America’s future economic growth.

Unlike 2008, where mortgage debt and opaque derivatives built up systemic risk tethered to failing consumer assets, most AI capex is linked to major public corporations with diversified business models and substantial liquidity. These deals are also tied to real, productive assets (chips, data centers), and the tech giants driving this boom generally have low debt and high cash reserves. Even if AI growth slows, leading companies can revert to their massive cloud or ad businesses.That said, the reliance on SPVs, leasebacks, and share swaps between AI labs and chip vendors can mask true demand through “circular financing,” reminiscent of earlier market bubbles where demand was artificially inflated (egs, Nortel pre-2000). Companies are increasingly using these structures to move risk off their own balance sheets and lock in long-term deals which can unravel quickly if real end-user demand or revenue growth disappoints.

Further, over 75% of recent S&P 500 gains and capital expenditures are traced to this AI sector, raising concerns about market breadth and systemic contagion if the sector falters. Top analysts caution that this “one-note narrative” creates interwoven financial risks, as complicated deal structures make companies mutually exposed (OpenAI with NVIDIA, AMD, Microsoft, Oracle) and debt-funded expansion increases fragility if underlying AI profitability falls short.

The AI hardware bottleneck which could occur in 1-2 years may be the biggest issue to slowing the growth of AI. But in the meantime, with global liquidity as a major tailwind, the AI buildout continues at a feverish pace.

Quantitative easing (QE) vs markets: A historical perspective

Indeed, outside of major global crises such as the Global Financial Collapse of 2008 or COVID of 2020, the top-level view shows that market direction is determined by global liquidity. Bull and bear markets both typically trade beyond what most expect. Outside of major global crises such as the Global Financial Collapse of 2008 or COVID of 2020, slowing QE is typically what ends bull markets (2000, 2022) while accelerating QE is typically what ends bear markets (1974, 2009, 2020), especially since 2008 when the Fed has relied increasingly on various forms of QE to prop markets.

QE is the 'Fed put', a morphine drip into the patient who remains unwell. Bitcoin's value against falling fiat illustrates how $1 in bitcoin in 2010 today is worth over $15 million, or a 15-million fold gain, providing a mirror which reflects fiat's exponential erosion. It highlights the irrationality and the destruction of fiat via "printing presses" which underscores the saying, "The market can remain irrational longer than you can remain solvent."